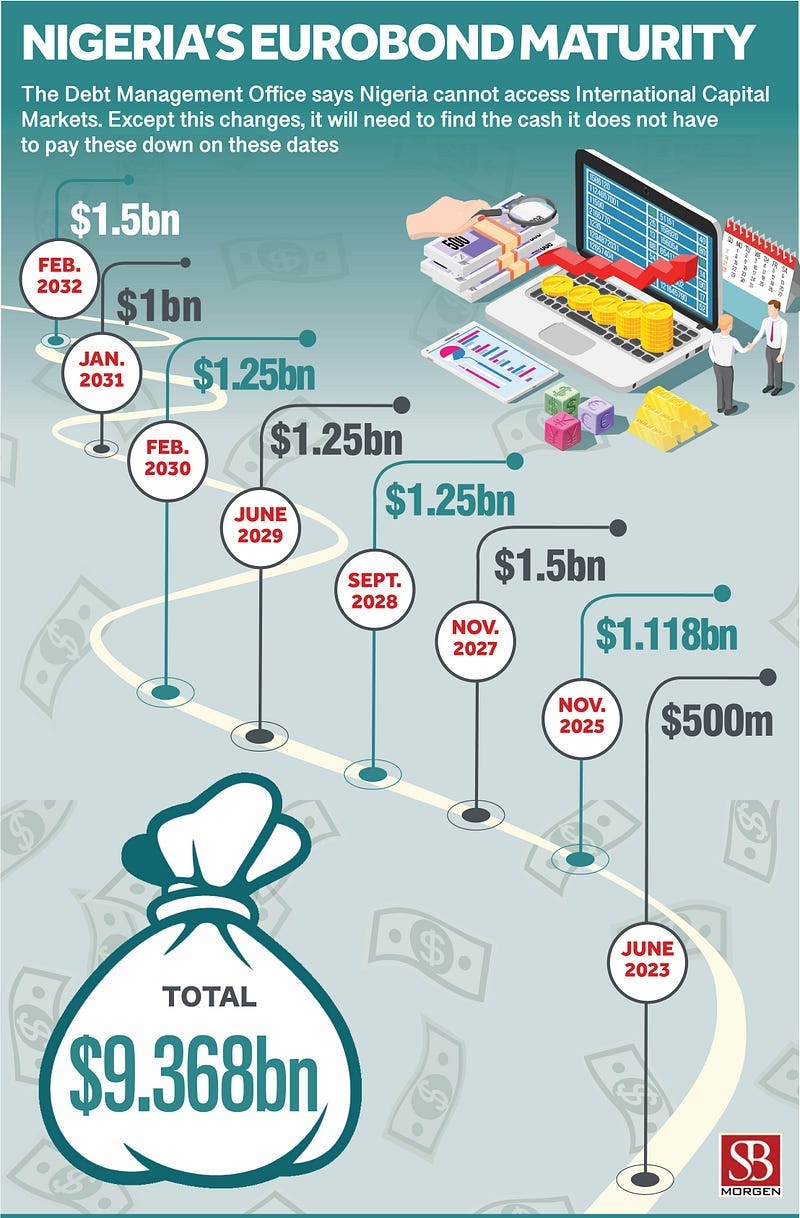

A few things about debt

The Nigerian government deducted more than ₦78 billion from state allocations for external debt servicing. This was according to the…

The Nigerian government deducted more than ₦78 billion from state allocations for external debt servicing. This was according to the National Bureau of Statistics’ Federation Account Allocation Committee Disbursement reports. The deductions were made in 2022 from the allocations given to state governments from the Federation Account. The state with the most deductions was Lagos, with about ₦23.61 billion deducted in 2022 for external debt servicing, followed by Kaduna (₦10.25 billion) and Cross River (₦7.56 billion). The least affected states were Borno (₦309.79 million), Delta (₦417.54 million) and Zamfara (₦417.96 million).

Over the past demi-decade, many Nigerian states have seen little to no foreign investment. Approximately a month ago, the NBS published a report that noted that foreign investors ignored 24 states as the value of capital importation crashed by 30.78 percent to $6.7 billion in 2021 from $9.68 billion in 2020. Of the 24, ten (Bayelsa, Ebonyi, Gombe, Jigawa, Kebbi, Kogi, Plateau, Taraba, Yobe and Zamfara) have not seen any foreign investments in the last three years. Coincidentally, the FDI decline coincided with the start of the coronavirus pandemic in 2020, as global movement restrictions saw Nigeria plunge into a recession. Additionally, the IMF warning cannot be divorced from a retreat of Chinese infrastructural development and assistance on the continent. Western sanctions on Russia have simply meant that its peers have taken note and are seeking to survive the shocks that the war in Ukraine has brought to the global economy. It has also been almost quiet on the Western front―instability in sub-Saharan Africa has jacked up operating costs for Western finance and sullied investment appetite. In its place has been security diplomacy, which is always gulped by the security industrial complex of many African states. In addition, for most sub-national external borrowings, the FG is required to provide debt guarantees. Hence it is not unusual that deductions for debt servicing are done at source. As the FG and states grapple with an ever-spiralling debt burden, the biggest concern on the minds of observers for the long term is the country and subnationals’ ability to service their commitments in a fiscally sustainable way. The big-ticket decisions to cut down expenditure and grow both federal and state-level government revenue from non-oil sources are still pending, and beyond even reining in the costs, this revenue raising will be the most crucial component of digging the country out of the debt hole its elites have worked it into. Analysts used to say that Nigeria has a revenue, not a debt problem. With recent disclosures by the World Bank that Nigeria spent 96.3 percent of revenue on debt servicing in 2022 from 83.2 percent the previous year, we can now state that Nigeria has significant revenue and debt problems. A big issue is that with hikes in interest rates domestically and internationally, borrowing costs are rising, and the appetite for Nigerian debt is slowing. All these signify a turbulent period ahead: many states with high debt profiles have little funds to address basic issues. The worrying thing about Nigerian debt is not its size but its utility. Lagos paid ₦23.61 billion in 2022 for external debt servicing but is still lumbering with 27% unemployment. The unemployment situation in Kaduna and Cross River is hardly encouraging. This fits a pattern across Nigeria’s states where loans are not channelled to projects that improve productivity and attract investment. Nigerian states are like their parent company, the federal government, stuck in a debt trap they may never get out of without some form of debt forgiveness. The conditions for debt forgiveness arose because the country achieved an annualised growth rate of 6.5% between 2003 and 2007, according to the Debt Management Office. The country was also transiting from the Abacha military era of sanctions into Western-style democracy. During the last decade of the 20th century, the DMO says Nigeria reached a debt overhang, meaning the country’s debt stock was beyond its future capacity to pay. It would be interesting to know what a similar model for the current low oil production and lagging non-oil sector environment would reveal. In the 2020 edition of the guidelines for states to borrow money from external sources, two prudent fiscal rules stand out: the debt servicing cost for the loan or loans to be borrowed must not surpass 40% of the Federal Accounts Allocation derived revenues, and the total loan portfolio of the state must also not exceed 250% of the preceding year’s revenue. While those rules are germane to ensure the country does not waltz into another debt overhang, the loans are also expected to tally with the central government’s agenda. This defeats the idea of a federal state. The 2020 guideline, an offshoot of the first version, published in 2008, gives the federal government absolute power to pick and choose what loans it decides to guarantee. A good illustration can be found with the ports. Two deep port projects with significant economic potential have been floated by All Progressives Congress governors under the current president’s term. Although an argument can be made that having multiple deep ports may mean that cargo demand may be too thin to sustain their long-term viability, the reality is that the outgoing government has demonstrated an unwillingness to diversify transportation. At least 80% of cargo entering Nigeria transits through (and spends an inordinate amount of time) in the Apapa or TinCan Island ports and, when out of port, is transported by road. A new port in Lekki has come online without rail linkage. The Buhari administration is yet to get cargo trains running on the Lagos-Ibadan rail corridor or utilise the country’s semi-extensive network of inland waterways. It is no surprise then that the $1.3 billion Olukola port floated by Ondo’s Rotimi Akeredolu awaits approval, seven months after the federal transport minister promised it would be ready before 29 May. Cross River Governor Ben Ayade said he left the opposition Peoples Democratic Party (PDP) and joined the ruling party to advocate for the Bakassi deep port. He said the state needs at least $350 million just to construct the port and he has been unable to secure Abuja’s backing. The entire project is valued at $2 billion. Away from the grind of fiscal policy, rising government borrowing has one major consequence: crowding out private sector access to much-needed credit. CBN data showed that credit to the private sector reached ₦43 trillion in Q1 2023, a rise of ₦1.3 trillion. Meanwhile, the Senate just okayed the President’s request to restructure ₦22.7 trillion in CBN Ways and Means advances to Aso Rock into 40-year bonds, practically increasing the national debt by a third. Since government bonds are inherently less risky than private credit, the near-term outlook for continued financial sector support for economic value creation will be constrained. The states, facing wilting revenue lines, rising debt deductions and populist pressure, will almost certainly fight back, and the Supreme Court will weigh in on the matter. The country’s fiscal situation will take up most of the next government’s attention and energies. The hope is that it is up to the task. Rather than securing loans to jumpstart the financial independence of states, the central government has secured at least $1.3 billion from the World Bank for a social safety net scheme whose return-on-investment profile is limited at best. In other words, when an item is not on Aso Rock’s agenda, do not expect much policy support.