A fragile stability

Nigeria’s June oil revenue dropped 23.9% to $2.98 billion amid volatile oil prices. Meanwhile, the CBN held rates at 27.5%, and reserves rose to $40.11 billion.

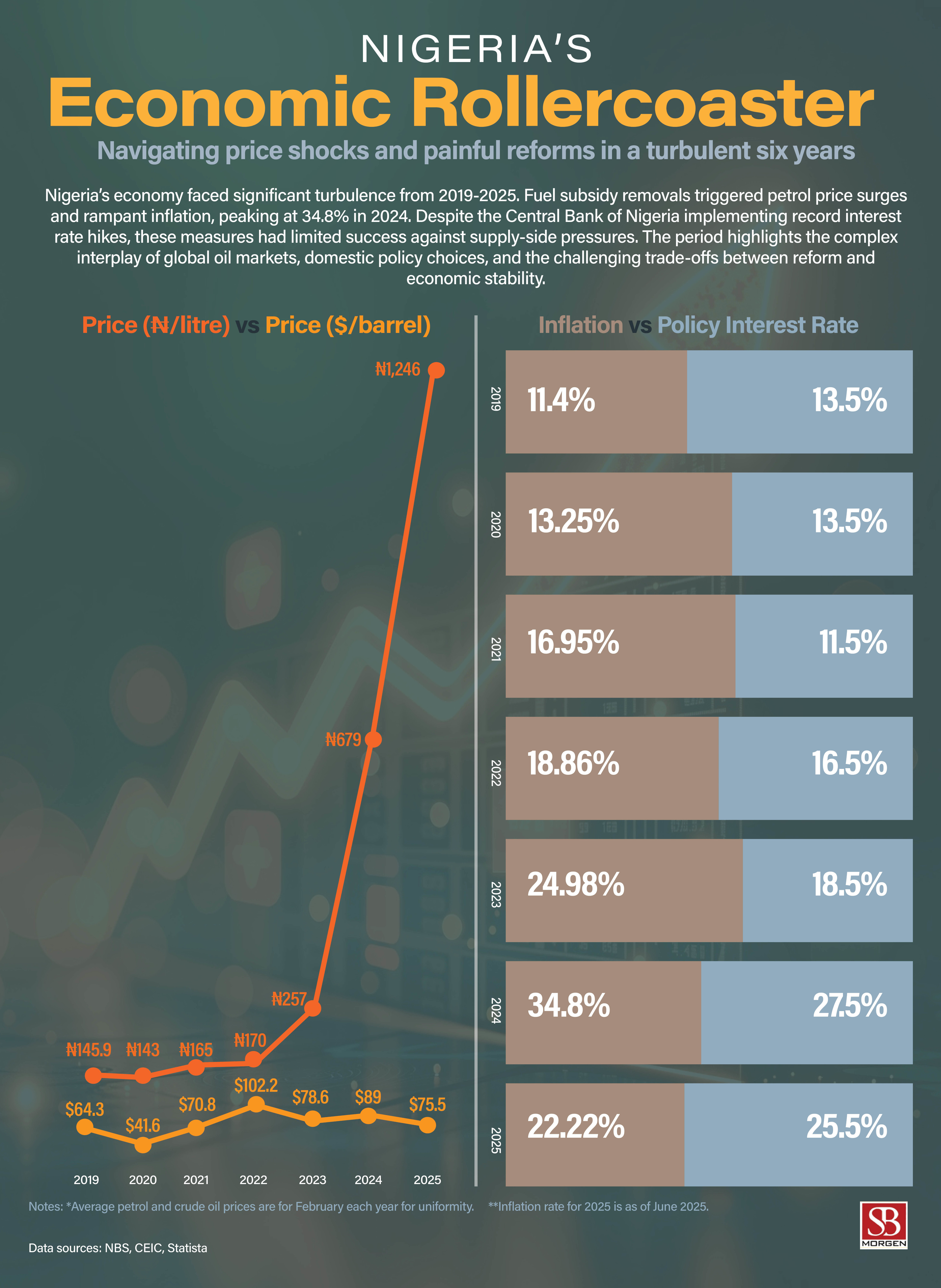

In June 2025, Nigeria’s oil revenue fell to ₦4.57 trillion—a 23.9% decline from May—due to volatile global oil prices driven by geopolitical tensions and uncertain OPEC+ production strategies, according to NNPC data. Despite this, Nigeria's economic landscape saw key developments: the Central Bank retained the Monetary Policy Rate at 27.5% to manage persistent core inflation, while the Senate approved President Tinubu’s borrowing plan, including $21.5 billion in external loans and a ₦757.98 billion bond to address pension liabilities. The naira remained stable officially but weakened slightly in NFEM. Nigeria’s external reserves rose to $40.11 billion, supporting foreign exchange stability.

Nigeria’s economic stability remains closely tethered to the global price and domestic production of crude oil, with the commodity accounting for approximately 65% of federal government revenue and over 85% of total exports. It is therefore unsurprising that the Nigerian National Petroleum Company (NNPC) Limited reported a month-on-month revenue decline in June 2025. However, the company’s improved timeliness in publishing financial statements is more notable—though several allegations, including those raised by the National Assembly, remain unaddressed.

The June 2025 revenue dip is a stark reminder of Nigeria’s acute exposure to global oil market volatility. External factors—geopolitical tensions, fluctuating Asian demand, and uncertainty within OPEC+—exerted downward pressure on prices, highlighting the structural fragility of a commodity-dependent fiscal framework. Indeed, revenue from crude oil and gas exports saw a significant drop from ₦6,013.98 billion in May 2025 to ₦4,577.85 billion in June 2025. This marks a clear downward trend from the peak of ₦6,163.78 billion recorded in April 2025. This sustained decline underscores the immediate impact of global market dynamics on Nigeria's primary income stream.

The broader macroeconomic context compounds the situation. The Central Bank of Nigeria’s decision to maintain the Monetary Policy Rate (MPR) at 27.5% reflects an attempt to temper persistent core inflation without derailing fragile economic activity. While headline inflation has slightly eased, core inflation remains stubbornly high, fuelled by energy costs, exchange rate pass-through, and logistics constraints. On the fiscal front, reliance on debt continues unabated. The Senate’s approval of President Tinubu’s borrowing plan—which includes over $24 billion in external loans and a ₦757.98 billion domestic bond specifically earmarked to clear pension arrears—underscores persistent structural funding gaps. Whilst the bond issuance may offer some reprieve by easing liquidity pressures and settling outstanding pension obligations, the sheer scale and direction of this borrowing raise serious questions over Nigeria's long-term debt sustainability, particularly in the context of recurring revenue shocks.

A modest improvement in external reserves—to $40.11 billion as of mid-July—provides a temporary cushion for exchange rate management and import cover. However, the Naira’s largely flat performance in official markets and its continued depreciation in the Nigerian Foreign Exchange Market (NFEM) suggest that underlying currency fragility remains unresolved.

Taken together, the interplay of declining oil revenue, elevated borrowing, and a cautious monetary policy underscores the economy’s constrained policy space. The imperative is clear: Nigeria must drastically reduce its dependence on oil, anchor inflation through comprehensive structural reforms, and channel debt into productivity-enhancing investments. Without this fundamental recalibration, Nigeria risks remaining perpetually reactive—merely managing crises rather than proactively shaping its economic outcomes. While the June oil revenue shortfall may prove transient, the structural vulnerabilities it exposes are far more enduring and demand urgent, decisive action.