A slide down

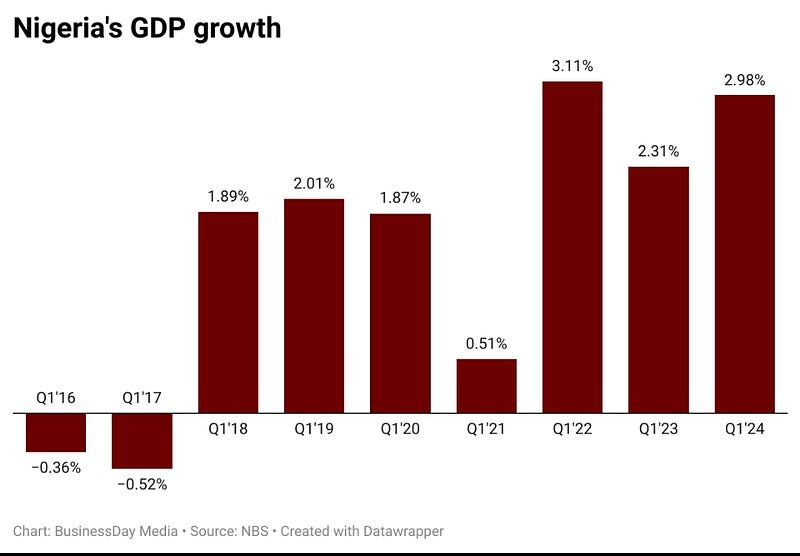

Nigeria’s GDP growth declined to 2.98% in Q1 2024, down from 3.46% in Q4 2023 but higher than the 2.31% recorded in Q1 2023. The services…

Nigeria’s GDP growth declined to 2.98% in Q1 2024, down from 3.46% in Q4 2023 but higher than the 2.31% recorded in Q1 2023. The services sector grew by 4.32%, contributing 58.04% to GDP. Agriculture and industry grew by 0.18% and 2.19%, respectively. Also, the oil sector’s real growth was 5.70%, and the non-oil sector grew by 2.80%. The money supply reached ₦96.96 trillion in April, up 74.26% from ₦55.64 trillion in April 2023, and increased 5.01% month-on-month from ₦92.33 trillion in March 2024. Currency in circulation rose by 65.40% to ₦3.92 trillion in April 2024.

This decline in the GDP growth rate should not be surprising given that GDP is simply the total amount of goods and services produced in an economy within a certain period. The GDP growth rate is slower than the IMF’s projected rate of 3.3%. largely driven by low growth in the non-oil sector, which is far larger than the oil sector. High inflation, the naira’s depreciation, increased electricity costs, and petrol scarcity — which resulted in higher prices — are some of the recent economic hiccups Nigerians have had to endure. Agriculture and industry are experiencing such tepid growth. These two sectors should be the engine of growth of the Nigerian economy, especially coming from the low-yield, low-industrialised base. However, they require the type of focused work the Nigerian state seems incapable of driving any longer. On the surface, a 2.98% GDP performance appears poor, but considering the monetary tightening by the Central Bank of Nigeria (CBN), akin to having the handbrakes on, growth below 3% is not unexpected. Perhaps the most important data is that the oil sector, which suffered negative growth for years, maintained positive momentum for the second straight quarter. If Nigeria can get inflation, exchange rates, and insecurity under control, then strong economic growth should follow. The problem is that these issues have been bedevilling the country for the past decade and are now entrenched. While Nigeria faces substantial economic challenges, there is still room for improvement and potential for growth. The remedy is carefully thought-out policies with short-, medium and long-term targets that are implemented systematically and coordinatedly. For starters, it is crucial to address pressing concerns hindering business growth and development, such as the draining burden of multiple taxation and arbitrary imposition of levies. The government must also be careful not to burden new businesses that are springing up and also ease the processes involved in exporting made-in-Nigeria goods. Only then can businesses grow and create jobs, translating into prosperity for the government and citizens. The Nigerian government must also learn to leverage some of its comparative advantage. If the services sector is the highest contributor to GDP, then archaic laws currently impeding players in the sector must be repealed. Opening up the sector will certainly have a multiplier effect on the economy.