Beware the pensioners

Ghanaian labour unions have asked for time to assess a proposal to restructure pension funds worth around 30 billion Ghanaian cedis ($2.7…

Ghanaian labour unions have asked for time to assess a proposal to restructure pension funds worth around 30 billion Ghanaian cedis ($2.7 billion). The nation is looking to extend the maturity periods of cedi currency bonds that the pension funds hold in exchange for higher interest payments as part of efforts to save billions in near-term debt payments under a loan deal from the International Monetary Fund. Abraham Koomson, leader of the labour federation, said there was a certain amount of “mistrust of government promises,” and they would need time to engage their constituents.

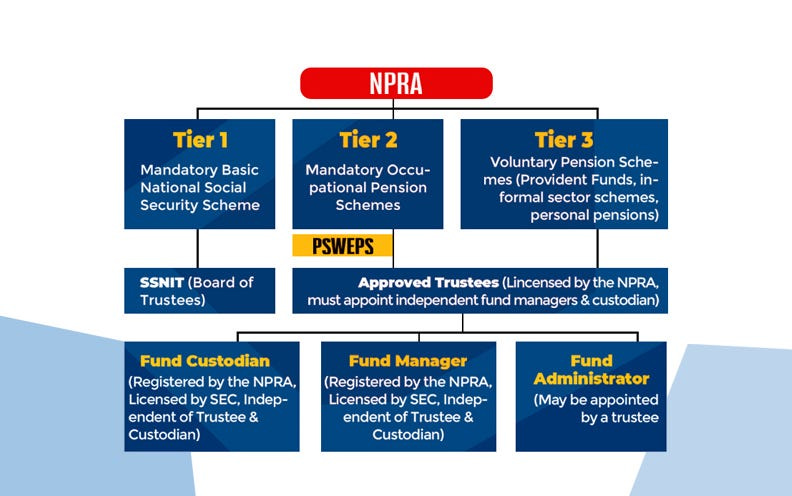

When the government revealed plans to carry out a Domestic Debt Exchange Programme (DDEP), the first group to request exemption was the Organised Labour — they told the Finance Minister, Ken Ofori-Atta, to stay away from pension funds. After several weeks of protests and threats of strikes, the government finally surprised Labour with a “Christmas present” by agreeing to go ahead with the DDEP without touching pension funds. “Government has decided to grant exemption to all pension funds in the DDE programme,” Organised Labour disclosed at a press conference on 22 December last year. More than five months after this assurance, Labour has been asked to return to the negotiation table for fresh talks on the wheels of improved restructuring terms. Abraham Koomson, the labour federation’s general secretary, who was present to sign the exclusion agreement, said that all strike plans had been dropped following the agreement in December 2022. Koomson said that the finance ministry agreed to drop pensions from the programme only if labour groups could arrange an alternative plan with the central bank. He disclosed that Labour unions had begun engaging the central bank. According to data from the Central Securities Depository Pension, funds held 6% of Ghanaian domestic public debt — 181 billion cedis or $20.1 billion — as of September ending 2022. The finance ministry hopes to shave off around 30 billion cedis ($2.7 billion) of pension funds in rounds of debt treatment talks with Labour. In February 2023, the government successfully prunes about 83 billion cedis of its domestic debt with a participation rate of 85% — excluding T-bills and bonds held by pension funds — and a combined average maturity of 8.2 years. It is clear the restructuring of more than 80 billion cedis of domestic debt isn’t enough to secure debt sustainability in the medium term. The government is trying hard to rope in pension funds and Independent Power Producers (IPPs), who have a combined weight of more than $4 billion on the West African country’s debt portfolio worth $40.4 billion. IPPs have refused at least two restructuring calls from the Ghanaian authorities and are threatening to cut power generation should the government insist on including them in the debt talks. Downgrades have started popping due to the government’s inability to pay coupons and maturing principals. Another group, pensioner bondholders, have been picketing at the finance ministry for days demanding payment of coupons and principals due them. The calling-back of groups initially exempted from the DDEP sends shock waves across the investor community and creates uncertainty. Assurances have simply become disappointments. First, President Akufo-Addo assured all investors that “there will be no haircuts.” Twenty-four days later, Deputy Finance Minister, John Kumah, disclosed that “for foreign bondholders, the government is proposing a 30% haircut on both principal and interests.” The second was Ken Ofori-Atta’s assurance that the current “Domestic Debt Exchange Programme will not affect individual bondholders.” This lifeline could not stay long on the exemption list as the government reversed this decision barely eighteen days after. Without any condition, the government also indicated that “treasury bills are completely exempted, and all holders will be paid the full value of their investments on maturity.” However, page 13 of the Amended and Restated Exchange Memorandum states that treasury bills issued by the Republic and certain non-marketable securities issued by the Republic are not subject to this Invitation to Exchange. However, such treasury bills and non-marketable securities may be the subject of other exchanges and purchases by the Government of Ghana from time to time.” With this condition in full swing, experts say the government may make a U-turn to include treasury bills to slash domestic debt to a sustainable level. For domestic creditors, the information on the DDEP continues to swing like a pendulum, and investors have been left at the mercy of flip-flops at such a crucial moment. External creditors, whose assurances helped Ghana obtain the $3 billion bailout package, are watching keenly and will take cues from the events in the domestic arena.