Beyond the surplus

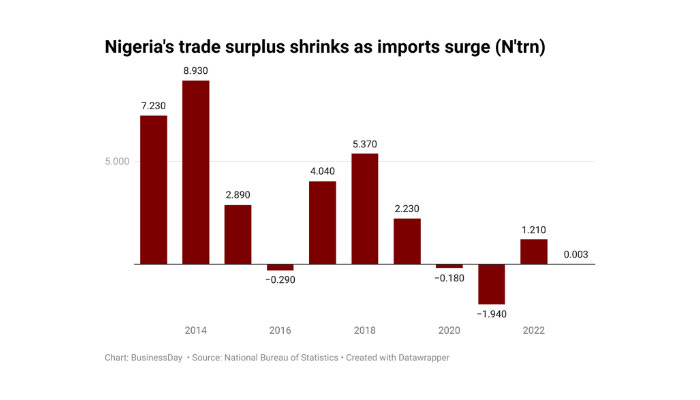

Nigeria recorded a trade surplus of ₦5.81 trillion ($3.36 billion) in Q3 2024, marking its eighth consecutive quarter of positive trade…

Nigeria recorded a trade surplus of ₦5.81 trillion ($3.36 billion) in Q3 2024, marking its eighth consecutive quarter of positive trade balance, though lower than the ₦6.9 trillion in Q2 and ₦6.52 trillion in Q1. Total merchandise trade reached ₦35.1 trillion, a 13.26% increase from Q2 and 81.35% higher than Q3 2023. Total exports in Q3 2024 were valued at ₦20.4 trillion, a 98% rise compared to ₦10.3 trillion in the corresponding quarter of 2023. Total imports in Q3 amounted to ₦14.6 trillion, an increase of 62.3 % from Q3 2023’s ₦9 trillion.

It is often argued that currency devaluation provides opportunities for exporters, making goods cheaper for international buyers and boosting trade. In Nigeria, the naira devaluation over the past 18 months has indeed made Nigerian products more affordable to neighbouring countries. For instance, eggs and grains from northern Nigeria frequently cross the borders into neighbouring markets, while the southern region’s plastic products, carbonated drinks and snacks hold potential for wider export. However, despite this theoretical advantage, manufacturers in Nigeria have struggled to capitalise on the situation due to poor infrastructure and prohibitively high interest rates, which make credit access expensive. These challenges have turned what could have been an economic opportunity into a missed one. The country’s trade policy, which focused more on import substitution than export promotion, compounds this issue. The Export Expansion Grant (EEG), Nigeria’s primary exporter incentive scheme, has faced allegations of corruption and poor management by the Nigerian Export Promotion Council, leaving many exporters disillusioned and unsupported. Despite these setbacks, Nigeria has maintained a positive trade balance since the fourth quarter of 2022, primarily driven by crude oil exports. In the third quarter of 2024, crude oil accounted for ₦13.4 trillion of the ₦20.4 trillion in total exports, representing 65% of Nigeria’s export profile. Non-oil exports, by comparison, contributed only 12.21%. While crude oil exports have been on a downward trend since late 2023, the recent increase in the trade surplus is attributed mainly to the naira’s devaluation. This has resulted in higher naira earnings per dollar for export proceeds, providing some relief to Nigeria’s current account and reducing external financial pressure. Agricultural exports have also recorded remarkable growth, surging by 301.87% to reach ₦884.07 billion. This marks a potential revival for a country that once relied on agriculture as the backbone of its economy before the 1970s oil boom. Legacy regions that once competed in producing world-class commodities such as cocoa, groundnuts and palm oil now have an opportunity to reclaim their prominence. The Tinubu administration has set an ambitious goal of achieving crude oil production of two million barrels per day by 2025. Encouragingly, the relative peace in the Niger Delta region has already led to slightly higher crude production. To achieve this target, the government must address longstanding issues such as infrastructure deficits, vandalism, theft, corruption and militancy, all of which have contributed to production levels falling below one million barrels per day in recent years. Additionally, Nigeria will need to negotiate a higher production quota with OPEC. While there are glimmers of hope in increased activity from the oil and gas sector and the resurgence of agricultural exports, significant work remains to transform Nigeria into a resilient, export-driven economy. Building robust infrastructure, fostering an enabling business environment, and reforming trade policies will be critical steps in ensuring Nigeria fully capitalises on its economic potential.