Billion-dollar debt

The Nigeria Extractive Industries Transparency Initiative (NEITI) reports that as of June 2024, the federal government is owed $6.071…

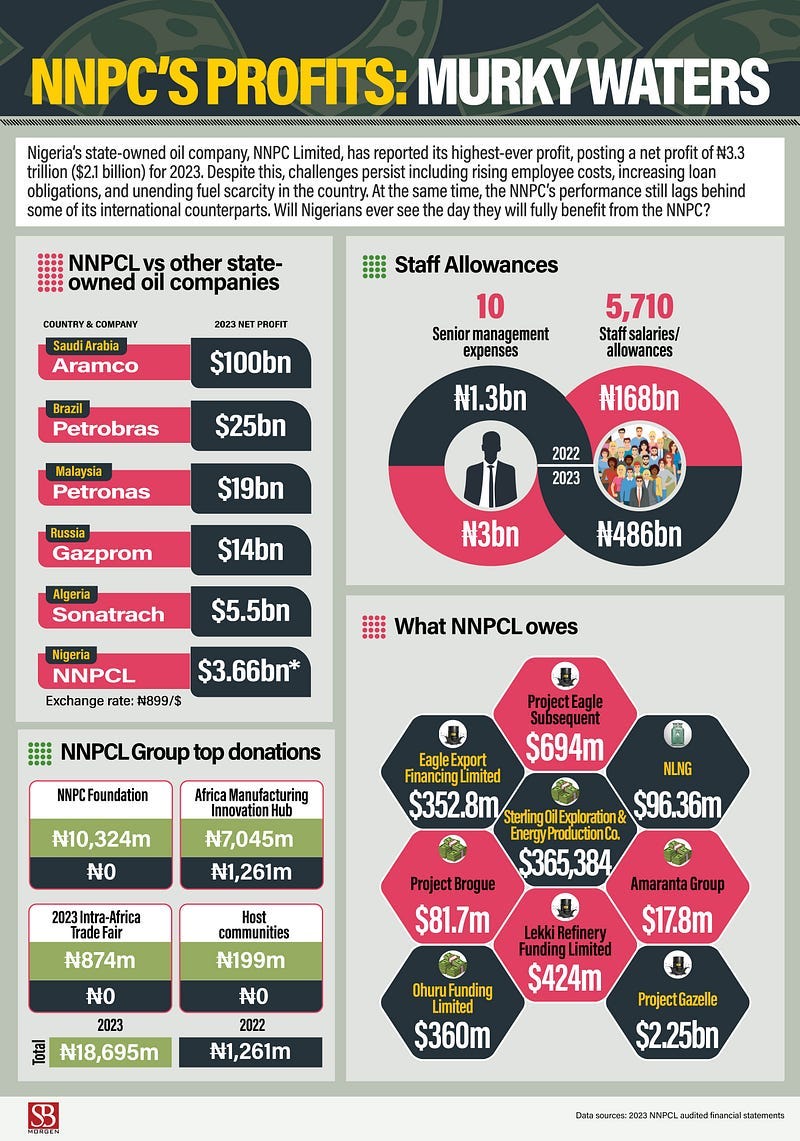

The Nigeria Extractive Industries Transparency Initiative (NEITI) reports that as of June 2024, the federal government is owed $6.071 billion and ₦66.4 billion in unpaid oil and gas revenues. This includes $6.049 billion and ₦65.9 billion in unpaid royalties and gas flare penalties owed to the Nigerian Upstream Petroleum Regulatory Commission (NUPRC), and $21.9 million and ₦492.8 million in taxes owed to the Federal Inland Revenue Service (FIRS). Additionally, Nigeria lost 7.68 million barrels of crude to theft or loss in 2023, a 79% decline from the 36.69 million barrels lost in 2022.

Over the last few months, substantial information has emerged regarding the mismanagement of the Nigerian economy during the Buhari administration. The government engaged in extensive borrowing by leveraging future oil sales to finance unproductive pursuits that failed to stimulate sustainable growth. According to the World Bank, Nigeria’s debt service-to-revenue ratio reached a staggering 96% in 2023, highlighting the severe financial strain on the country’s economy. Members of the current economic team contend that the removal of subsidies and the naira devaluation were necessary measures to address this crisis. However, it is evident that the Nigerian economy requires fundamental restructuring, but unfortunately, the necessary funds to facilitate this transformation are not readily available. The existing debt burden will hinder the government’s ability to increase revenue inflows to adequately fund its budget. Despite efforts to diversify into non-oil sectors, crude oil sales remain a critical source of government revenue, accounting for approximately 60% of total earnings. The ongoing volatility in global oil prices and domestic production challenges further complicate this reliance. Additionally, there is a pervasive lack of trust in the government among the populace and investors, which exacerbates the situation. When the government is unable to fund its budget adequately, its capacity to invest in vital infrastructure projects — essential for creating jobs and fostering economic growth — is severely restricted. Furthermore, insufficient funds compel the government to continue borrowing, resulting in an escalating debt stock that could jeopardise future economic stability. The combination of high debt levels, overreliance on oil revenues, and a lack of public trust creates a precarious situation for Nigeria’s economic future, necessitating urgent and strategic reforms.