Budget talk

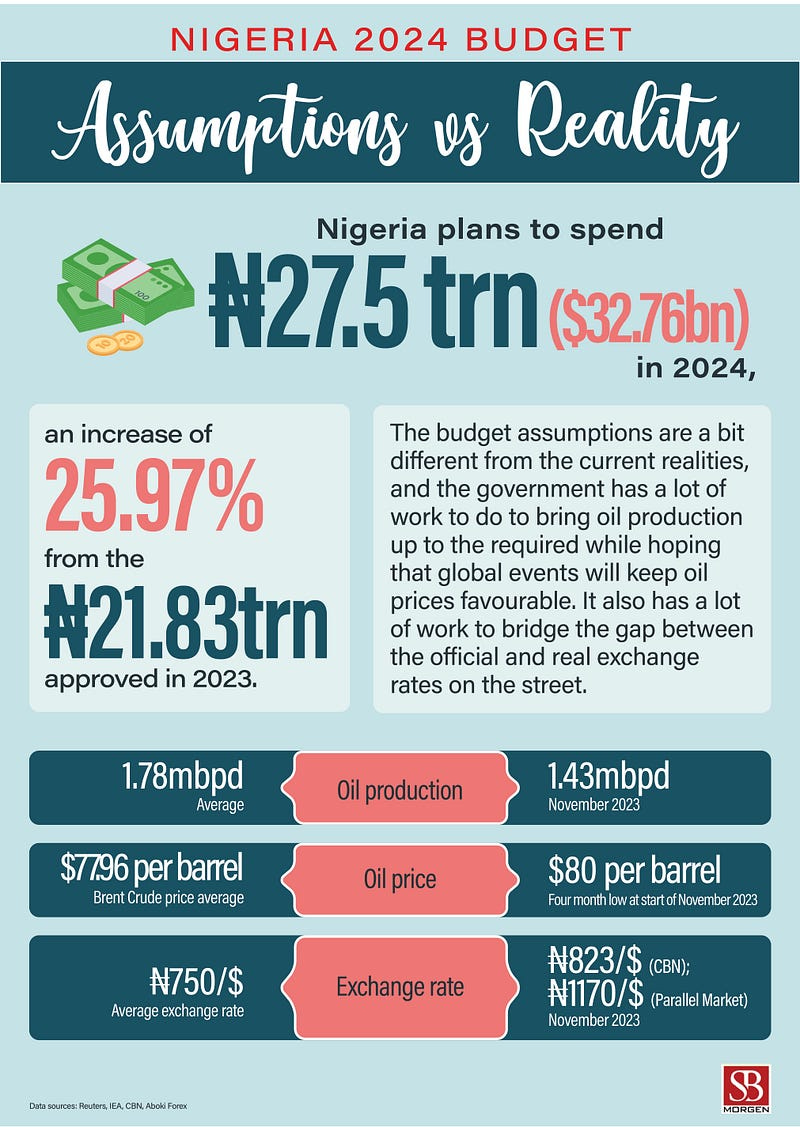

Nigeria has revised its 2024 budget upwards by ₦1.5 trillion to ₦27.5 trillion ($32.76 billion), Budget Minister Atiku Bagudu said, after…

Nigeria has revised its 2024 budget upwards by ₦1.5 trillion to ₦27.5 trillion ($32.76 billion), Budget Minister Atiku Bagudu said, after increasing the oil price benchmark to $77.96 and lowering the naira exchange rate assumption to ₦750 per dollar. Also, the government is seeking to borrow $8.6 billion and €100 million. President Tinubu said the Buhari administration approved the 2022–2024 external borrowing rolling plan on 15 May 2023. Meanwhile, the Socio-Economic Rights and Accountability Project has urged the World Bank to halt loans to Nigeria’s 36 states, citing allegations of mismanagement of public funds.

While we think that the oil assumption revisions are sound and grounded in the current realities of global and domestic outlook, oil production, which is currently at 1.43 million barrels per day and up from 1.23 million barrels per day in the previous month, is still behind the 1.78 million barrels per day target set in the 2024 budget submission. The last time Nigeria’s monthly production averaged 1.7 million per day was in May 2020. However, if the current trajectory continues, the target will be achievable, which can only mean positives for Nigeria’s precarious fiscal position. Meanwhile, it is still largely dependent on oil and gas for FX supply to the government, and the biggest current challenge in the official FX market is the supply of USD. Over the last few weeks, several politicians have said that the Tinubu administration took over a “dead economy” from its predecessor and that aggressive actions are required to give the economy a fighting chance. Like Mr Buhari, President Tinubu believes spending money, regardless of availability, is the best way to awaken the economy. However, while that appears reasonable on the surface, a deeper look shows that much government spending goes to waste in Nigeria due to corruption and lack of political will. Unless these are addressed, the only outcome is more debt burden on the Nigerian people. Additionally, while the Nigerian government’s stated goal of a ₦750 exchange rate may appeal to some, it is unclear how this target will be achieved. Given that the Tinubu administration has said it would converge the multiple exchange rates, we wonder how the exchange rate benchmark is still at variance with the I&E Window or black market rates. Analysing the actual budget, a breakdown shows that security will receive the highest allocation, getting 12% of the total budget. Education will get 7.9%, and health will get 5%, showing how much is unchanged in the country’s budgeting thinking. Nigeria’s budgets are usually grossly inadequate to meet the country’s most pressing needs, and this is no different. Finally, on the SERAP call, Nigerian state governments have a perennial mismanagement problem. They have become the prodigal sons who incur loans, mismanage whatever resources they have — or refuse to develop them — and wait for monthly allowances from the federal government. Some of the problems the federal government contends with are due to the inability of states to cater for their populations. Even if the World Bank withholds loans from them, several parties are willing to give loans to states backed by a sovereign government at a higher interest rate. It is, therefore, uncertain that SERAP’s approach will fix the bad behaviour of Nigeria’s subnational governments.