Cash capped

The Central Bank of Nigeria (CBN) has set new limits for Point of Sales (PoS) agents, capping daily transactions at ₦1.2 million ($725) and cash withdrawals per customer at ₦100,000 ($60). Weekly cash withdrawals are restricted to ₦500,000 per customer. PoS agents must use the approved Agent Code 6010 and connect terminals to a Payment Terminal Service Aggregator. Separately, the CBN announced strict penalties for banks involved in mint Naira hawking, including a ₦150 million fine for violations. The CBN plans periodic checks, mystery shopping, and intensified monitoring of banking halls and ATMs around the country to curb this illicit trade.

Regulatory intervention in the cash access space has become increasingly imperative as banks impose severe limitations on customers’ ability to withdraw cash over the counter and neglect the maintenance of their Automated Teller Machines. These actions have left customers with few options, making Point-of-Sale (PoS) agents the primary and often sole reliable avenue for cash access. However, this convenience comes at a premium, further straining consumers who must bear additional costs for what should be a basic banking service. We advocate for a more robust and inclusive system where customers have diverse channels to access their cash seamlessly. These channels should include well-functioning bank halls, properly serviced ATMs, and widespread PoS agent networks. Such an ecosystem ensures flexibility, convenience and affordability. For this to work, the Central Bank of Nigeria (CBN) must balance regulation and market dynamics. Allowing market forces to dictate service fees can drive innovation and competition, but only if financial service providers are held accountable for ensuring availability and operational efficiency across all platforms. Without this balance, Nigerians, driven by necessity, may resort to alternative and potentially disruptive means to access cash.

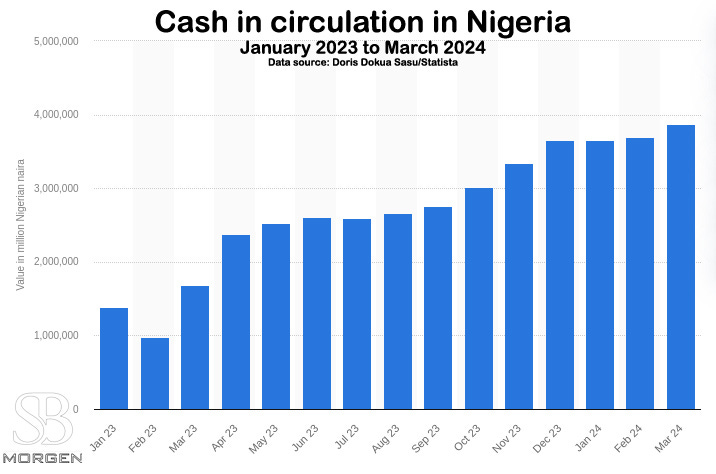

A visit to any bank ATM highlights the severity of the current limited cash availability, with many machines either out of service or dispensing limited amounts. Across the counter, customers face withdrawal limits as low as ₦20,000 ($12) per day—a restriction that has sparked widespread frustration. Yet, paradoxically, the CBN’s data reveals a 93.3% surge in currency circulation, reaching an astonishing ₦4.1 trillion. Despite this, only 6.6% of this figure remains within the banking system, with the vast majority—93%—circulating outside formal financial channels. This apparent disconnect may, in part, reflect the unintended consequences of the Shared Agent Network Expansion Facilities (SANEF) initiative, launched by the CBN in 2019 to promote financial inclusion. While SANEF has successfully empowered hundreds of thousands of Nigerians to become PoS operators and bring financial services closer to underserved areas, it has also created a new dynamic. Many merchants now circumvent traditional banking channels by withholding daily cash deposits, leaving bank vaults and bulk rooms unusually empty. This trend has exacerbated banks' liquidity issues, raising questions about whether the CBN’s recently proposed guidelines will effectively address these challenges.

Meanwhile, the gradual rise of digital payment platforms and mobile banking has reduced consumers’ reliance on physical cash compared to previous years. Yet, Nigeria remains a predominantly cash-based economy, particularly in rural and informal sectors. This underscores the need for a comprehensive and adaptable approach to cash management. The CBN must address the operational inefficiencies within banks and the broader systemic issues contributing to the currency’s circulation imbalance. Regulatory enforcement must not only penalise non-compliance but also incentivise banks to prioritise customer needs, maintain their ATM networks, and improve cash accessibility across the board. Ultimately, a thriving financial system depends on trust, accessibility and efficiency. The CBN’s efforts to regulate the cash economy should be complemented by strategies encouraging collaboration among banks, fintech companies and other stakeholders. By addressing the root causes of the cash access crisis, Nigeria can transition towards a more inclusive and resilient financial ecosystem.