Cemented exit

Swiss building giant, Holcim, is selling its 84% stake in Lafarge Africa to China’s Huaxin Cement for $1 billion, marking its exit from…

Swiss building giant, Holcim, is selling its 84% stake in Lafarge Africa to China’s Huaxin Cement for $1 billion, marking its exit from Nigeria as part of a portfolio refocus on high-growth regions. The deal, expected to close in 2025, reflects Huaxin’s growing African acquisitions. Meanwhile, Nigeria faces a sharp $12.8 billion drop in foreign holdings between 2022 and 2023, falling to $73.4 billion due to naira devaluation and corporate exits, as noted in the World Investment Report 2024. Nigeria’s inward and outward foreign direct investments also declined, with FDI inflows reaching historically low levels, further straining the country’s economic outlook.

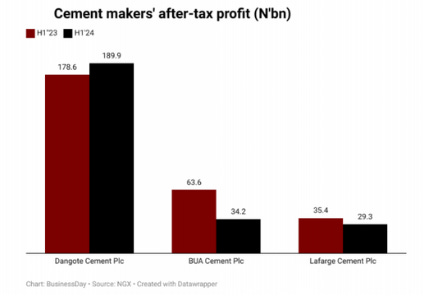

In recent years, the dynamics of the Nigerian economy have changed significantly, forcing investors to reconsider their assumptions about Nigerians’ spending capacity and preferences. Nigeria’s challenging business environment, worsened by the removal of the petrol subsidy and naira devaluation, has led to the exit of more multinationals from Africa’s most populous country. The naira, which has weakened by more than 70% since the FX reform in 2023, coupled with the departure of multinationals, helps explain why foreign direct investment (FDI) inward stock fell by 14.9% last year. This decline is more pronounced when compared to 2021, where FDI inward stock fell only marginally by 1.49%. South Africa, which remains the top FDI recipient in Africa, also saw a drop in its FDI stock, falling from $172.2 billion in 2022 to $124.0 billion in 2023. FDI, a key category of cross-border investment, is crucial for spurring economic growth, technological advancement, and job creation. However, over the past few months, there has been a consistent rise in exit plans or reductions in involvement by multinationals, particularly in the manufacturing sector. In the second half of 2023, at least five multinationals — Procter & Gamble, GlaxoSmithKline Consumer Nigeria, Equinor, Sanofi, and Bolt Food — announced plans to exit Nigeria in 2024. The trend continued in 2024, with companies like Kimberley-Clark, Heineken (exiting Champion Breweries), Diageo (exiting Guinness Nigeria), Eni (exiting Nigerian Agip Oil Company), Mobil (exiting Mobil Producing Nigeria), and Pick n Pay also pulling out of the country. The exit of these multinationals weakens Nigeria’s productivity capacity, making achieving a one-trillion-dollar economy by 2030 an uphill task. As Africa’s fourth-largest economy, Nigeria cannot reach this milestone without a strong and thriving manufacturing sector. Challenges such as lingering foreign exchange scarcity, high energy costs, port congestion, multiple taxation, insecurity, and poor infrastructure continue to stifle the sector’s growth. According to the National Bureau of Statistics, the real growth rate of the manufacturing sector in the third quarter of 2024 was just 0.92%, the lowest since 2022’s third quarter when the sector contracted. The Manufacturers Association of Nigeria also reported a 37% drop in job creation during the first half of 2024. Two recessions over the past eight years have hindered Nigeria’s ability to grow beyond $500 billion. The last time Nigeria exceeded that figure was in 2014, when its GDP stood at $574.2 billion, according to the World Bank. By last year, the economy had fallen to $362.8 billion, down from $477.4 billion in 2022. Multinationals have historically been major contributors to Nigeria’s GDP and earnings. Before the exits of major multinationals this year, many manufacturers, particularly in the fast-moving consumer goods industry, had either left the country or stopped producing certain products due to the difficult operating environment. Earlier this year, President Bola Tinubu claimed that his reforms had attracted $30 billion in FDI into the economy within one year. However, in the second quarter of 2024, the National Bureau of Statistics reported that FDI dropped to $29.8 million — the lowest figure since the agency began compiling data in 2013. This decline highlights a growing trend of joint ventures between Chinese companies and African nations. Companies like Huaxin Cement, which acquired cement firms in Tanzania, Zambia, South Africa, and Mozambique since 2020, and West China Cement, another major player, have expanded into countries such as the Democratic Republic of the Congo and Mozambique. Huaxin’s majority stake in Lafarge Africa, if completed next year, could further boost Lafarge’s market capitalisation and financial performance. In the first nine months of 2024, Lafarge reported a 53% growth in earnings, reaching ₦60.1 billion from ₦39.3 billion in the same period last year, while Dangote Cement saw a slight profit increase of 0.58%, amounting to ₦279.1 billion. However, BUA Cement’s earnings fell by 36% to ₦48.9 billion. Despite Lafarge’s impressive earnings growth, its profit is smaller than Dangote’s. The Nigerian cement market, dominated by three major players — Dangote Cement, BUA Cement, and Lafarge — faces increased competition, especially with the Chinese acquisition. If successful, this acquisition could position Huaxin as a top contender in the market. As the world’s top cement producer, China’s entry into the Nigerian market could intensify competition, with companies vying for customers through lower prices and higher-quality deals. The cement subsector is one of the three largest contributors to Nigeria’s manufacturing sector. While many FDIs from Europe and North America have pulled out, others from Asia are stepping in. The Nigerian building materials and cement industries remain robust, but the growing competition in these sectors is causing margins and growth opportunities to shrink, leading investors like Holcim to reconsider their positions in the market.