Chocolate therapy ends

Cocoa prices plummet as strong port deliveries suggest improved supplies, despite forecasts of significantly weaker harvests due to disease and dry weather.

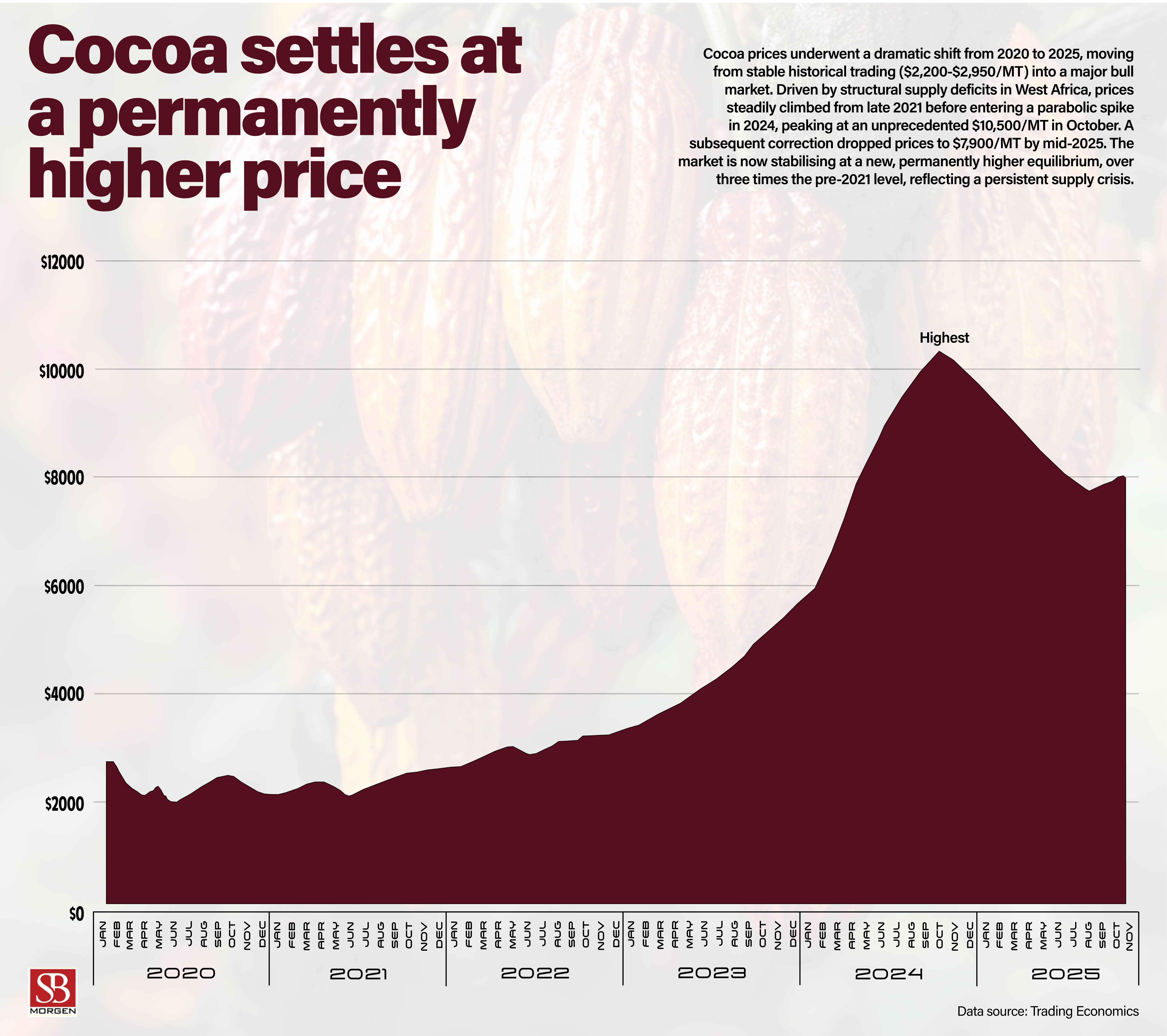

Cocoa futures continued to fall this week as strong arrivals at Côte d’Ivoire’s ports deepened expectations of improved supplies despite warnings of weaker harvests ahead. Prices hit their lowest point since February 2024 in New York, now about 60% below last December’s record, after port deliveries topped 100,000 tons for a third straight week — a sign of recovering stocks and shifting production patterns. Industry analysts say current volumes reflect carryover beans from last season and favourable early-season flows, though surveys still point to a slightly weaker main crop due to earlier dry weather. Reuters reports that Côte d’Ivoire has already sold 1.3 million tons of 2025/26 cocoa contracts, marginally below last year, as ageing farms, disease, and erratic rainfall are expected to cut arrivals by about 30% between January and March 2026. The Coffee and Cocoa Council says no contract defaults are expected but warns the intermediate crop may fall by as much as 30%, prompting tighter stock checks and restrictions on exporter purchases.

The recent slide in cocoa prices to an eight-month low highlights the rapid shifts in sentiment within West Africa’s soft commodity chain. This decline, driven by strong Ivorian port arrivals, shows traders are prioritising short-term supply relief over the persistent structural pressures that caused record highs just a year ago. It is a significant, yet likely temporary, correction.

Contextualising this supply is crucial. The strong arrivals in Côte d’Ivoire are believed to be carryover stock and favourable early-season flows, not a fundamental farm-level turnaround. The core agronomic constraints remain: ageing tree stock, disease escalation, such as Swollen Shoot Virus, and increasingly erratic rainfall. Industry surveys still point to a softer main crop ahead, a severe concern for a commodity vital to regional exports and incomes.

Regulatory-wise, the Ivorian Coffee and Cocoa Council insists contract defaults are unlikely, but its warnings of a weaker intermediate crop signal a period of heightened control ahead. This will include tighter stock verification, stricter rules for exporter purchases, and a more interventionist posture, leading to higher compliance costs and thinner margins across the industry.

For smaller producers like Nigeria, these dynamics are highly significant. While Nigeria’s cocoa belt is undergoing revival, its lack of coordinated sector reforms limits its ability to capitalise on any supply gaps left by Côte d’Ivoire. More broadly, this situation reinforces that price volatility is becoming a structural feature of the market. The sector’s long-term supply risks, driven by climate change and regulatory interventions, are colliding with rising global demand, keeping the market hypersensitive to West African port arrivals. In summary, the current price dip is a reprieve, not a reset of the cocoa market’s deep-seated challenges.