Climbing

Ghana’s year-on-year inflation rate at ex-factory prices for goods and services rose to 33.2% in August 2024, up from 29.1% in July, with…

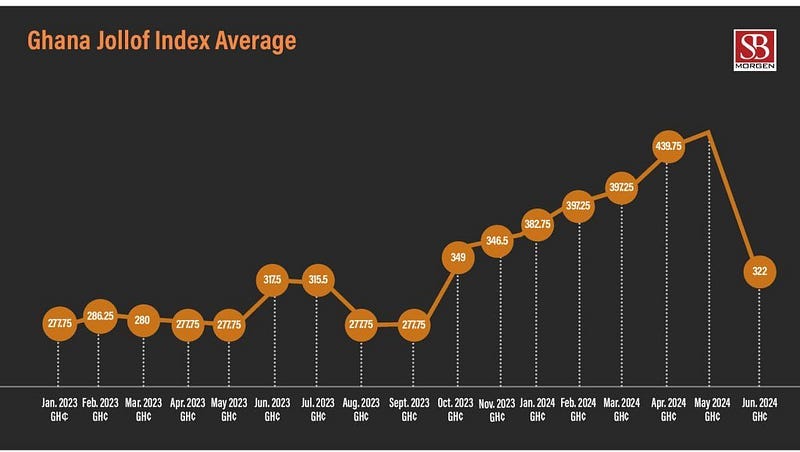

Ghana’s year-on-year inflation rate at ex-factory prices for goods and services rose to 33.2% in August 2024, up from 29.1% in July, with month-on-month producer inflation at 2.7%. The Producer Price Inflation (PPI) in the Industry sector increased to 44.2%, while the Construction sector’s rate dropped to 27.7%. Ghana’s economy grew by 6.9% year-on-year in Q2 2024, the fastest in five years, driven by a 9.3% rise in the Industry sector, particularly mining and quarrying. The services sector grew 5.8%, and agriculture rose 5.4%, though the cocoa sector contracted for the fourth consecutive quarter by 26.2%.

Ghana’s economic crisis continues to unfold, with key indicators still signalling distress. Despite over a year of the IMF-supported economic recovery programme, which has successfully undergone two reviews and disbursed more than $1.5 billion, the tangible benefits remain elusive for the average Ghanaian. Consumer inflation has declined significantly but remains stubbornly high at over 20%, and producer inflation, which is a predictor of future consumer inflation, continues to rise at year-on-year and month-on-month levels, indicating further price pressures ahead. This disconnect between the first macroeconomic stabilisation goals and the lived experience of Ghanaians highlights the country’s deep-seated challenges. One of the biggest concerns is the continued depreciation of the cedi against major currencies, compounding inflationary pressures. The country’s GDP growth rate of 6.9% may seem impressive at face value — marking the fastest quarterly growth in five years — but this growth is largely driven by inflation. The sharp rise in prices has inflated the GDP figures when calculated using both the constant and current market price (purchasing approach), making the growth appear more robust on paper than it is in real terms. For the average consumer and businesses, high prices are eroding purchasing power, and the cost of borrowing remains excessively high, further dampening economic activity. The nominal growth is not translating into real economic relief, as productivity is not growing at the same rate as prices. Ghana’s agricultural sector, particularly cocoa — a key export commodity — continues to decline, with no signs of recovery in the near term. Persistent challenges, including low yields, high input costs, and global price fluctuations, are compounding the sector’s struggles. This lack of momentum in such critical subsectors poses a significant risk to overall economic growth, as agriculture plays a vital role in Ghana’s economy. The IMF programme’s focus on macroeconomic stability, such as reducing fiscal deficits and stabilising the currency, has yet to translate into broad-based economic improvements. The real sector — agriculture, manufacturing, and services — is struggling with high production costs, expensive credit, and weak consumer demand. Cocoa, which is supposed to be the backbone of the Ghanaian economy, has lost its power as illegal mining activities and bad weather conditions continue to affect yield and revenue.