Cocoa prices take a tumble

President Alassane Ouattara has won re-election in Ivory Coast. The opposition conceded, and the news triggered a fall in global cocoa prices.

President Alassane Ouattara won the Ivorian presidential election, with early results showing that the 83-year-old leader is leading comfortably nationwide. Opposition candidate and former commerce minister Jean-Louis Billon conceded defeat, congratulating Ouattara and acknowledging that preliminary figures place the incumbent ahead. Partial results from the Independent Electoral Commission indicate a strong turnout in northern regions loyal to Ouattara, while participation remained low in southern opposition areas. The vote, held on October 25, was marked by a fragmented opposition after former President Laurent Gbagbo and ex-Credit Suisse chief Tidjane Thiam were barred from contesting. Security forces remain deployed as isolated clashes left two people dead, though Abidjan has remained largely calm. Meanwhile, global cocoa futures fell by more than 3% to around $6,100 per tonne on October 27, amid optimism over strong West African harvests. Analysts say the expected supply rebound from the Ivory Coast, the world’s top cocoa producer, has eased market concerns after months of price volatility.

President Alassane Ouattara’s securing of a fourth term in Côte d’Ivoire’s most recent election was, externally, a relatively peaceful affair, particularly when contrasted with the tumultuous political scenes in countries such as Cameroon and Tanzania. Internally, however, the contest was widely perceived as a coronation rather than a genuine democratic exercise, largely due to the disqualification of key opposition candidates. The resulting fear of violence and mass arrests actively discouraged many citizens from voting, while others chose to boycott the election altogether.

President Ouattara shrewdly capitalised on the Ivorian population’s profound desire for stability and peace, a sentiment rooted in the fresh memory of past civil wars and their devastating consequences. His administration’s formidable economic performance since 2012 reinforced this preference for non-confrontation.

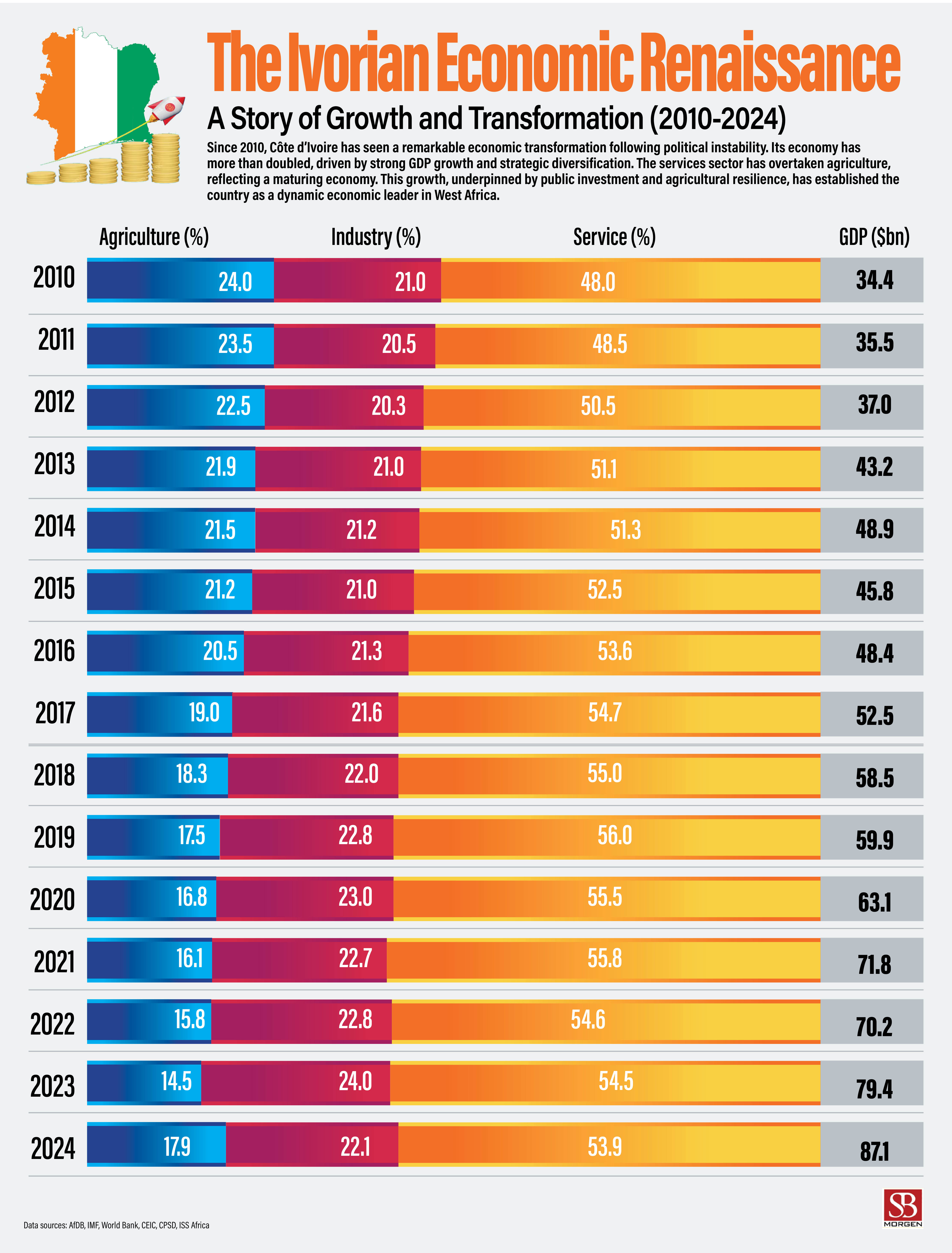

The Ivorian economy has experienced a significant post-crisis recovery, averaging around 7% annual GDP growth between 2012 and 2024. This growth successfully drove down the national poverty rate from 44.4% in 2015 to 31.94% in 2024, marking substantial progress. Crucially, this economic renaissance has been achieved through effective diversification. A look at the economy between 2010 and 2024 reveals a strategic shift: the Service sector has emerged as the dominant economic engine, expanding its share from 48.0% to 53.9%. Conversely, Agriculture, traditionally reliant on cocoa, saw its economic share decrease significantly from 24.0% in 2010 to 17.9% in 2024. While the cocoa industry’s contribution to GDP now sits at a more sustainable level (around 7% to 8%), the initial rapid focus on expansion in earlier years slowed poverty reduction efforts between 2012 and 2015. Despite the overall success, challenges persist, including growth that relies on external factors, an uneven distribution of wealth, and a vulnerability to global market fluctuations, all of which underscore the continuing need for deeper industrialisation and truly inclusive development.

While Mr Ouattara’s economic achievements provide a strong foundation for his popular mandate, his decision to seek a fourth term by altering the constitution introduced significant political instability. The core conflict stemmed from this attempt to secure another term, which led directly to the exclusion of opposition leader Tidjane Thiam and other key political figures from the race.

Political tension escalated throughout the summer of 2025, starting with peaceful demonstrations in June before moving to a mass protest in August demanding a revision of the electoral roll. By early October, the government had significantly hardened its stance, forcefully banning nationwide demonstrations and cracking down on dissent. This culminated in the violent dispersal of a protest on 11 October, with security forces deploying tear gas and roadblocks, resulting in the arrest of at least 237 people, including journalists and political activists.

In the short term, the low voter turnout, a trend mirroring the declining participation and growing disillusionment with democracy seen across other West African countries, suggests a temporary return to stability, easing immediate fears of disruptions to the crucial cocoa supply chain. However, the political risks remain high. With the election outcome widely viewed as illegitimate by the opposition, lingering divisions and discontent could keep the commercial capital, Abidjan, on edge. The immediate challenge for Côte d’Ivoire is to reconcile its impressive economic renaissance with its deepening political fragility, as the perceived lack of a genuine democratic contest risks alienating key segments of the population and potentially jeopardising the very stability that allowed the nation’s economic success to flourish.