Divide and reform

Nigeria's Governors' Forum endorsed a revised VAT sharing formula, allocating 50% equally, 30% by derivation, and 20% by population.

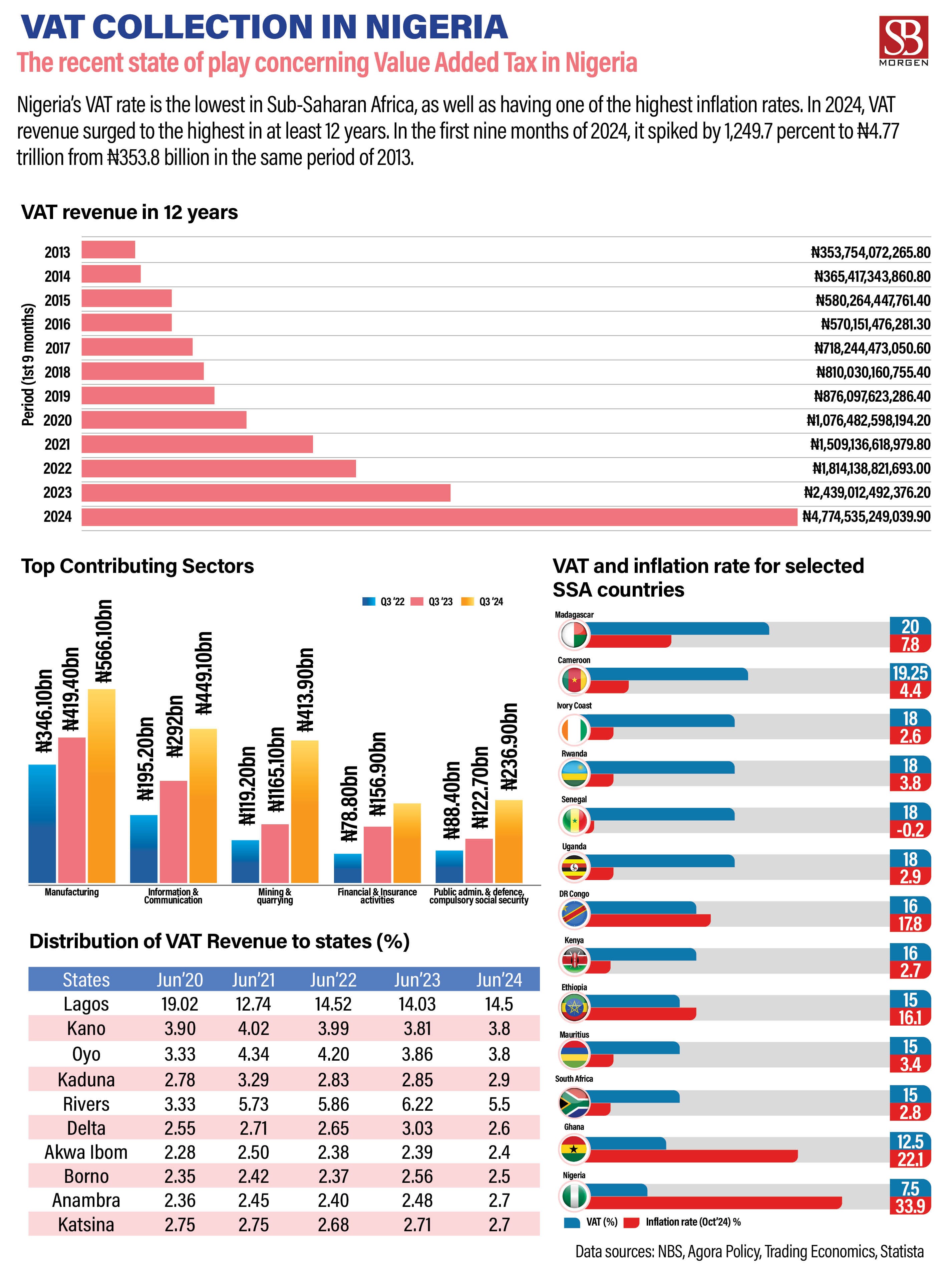

The Nigeria Governors’ Forum (NGF) has endorsed a revised Value Added Tax (VAT) sharing formula, allocating 50% based on equality, 30% on derivation, and 20% on population. NGF Chairman AbdulRahman AbdulRazaq announced that the decision followed consultations with the Presidential Tax Reform Committee and Federal Inland Revenue Service. Governors opposed increasing the VAT rate or reducing Corporate Income Tax (CIT) and advocated continued VAT exemptions for essential goods and agricultural produce to protect citizens’ welfare and boost agricultural productivity. The formula aims to ensure equitable resource distribution among states while addressing economic and social priorities.

For decades, tax reform in Nigeria has been a topic of intense discussion, yet successive administrations lacked the political will to tackle the issue. The current administration under President Bola Tinubu deserves commendation for advancing the conversation with its tax reform initiatives. These reforms, encapsulated in four bills—the Nigeria Tax Bill 2024, the Nigeria Tax Administration Bill, the Nigeria Revenue Service Establishment Bill, and the Joint Revenue Board Establishment Bill—aim to address long-standing issues in Nigeria’s fiscal framework. Their overarching goal is to improve the country’s Tax-to-GDP ratio, currently at 8%, compared to the Sub-Saharan average of 16%, and incentivise state governments to boost internally generated revenue rather than relying predominantly on allocations from the Federation Account Allocation Committee.

The contentious issue of Value Added Tax allocation is central to these reforms. Presently, VAT is remitted based on the location of company headquarters, which disproportionately benefits southern states where most corporate headquarters are located. The Nigerian Governors Forum (NGF) recently proposed formula differs from the Federal Government’s proposed formula of 20% for equality, 20% for population, and 60% for derivation, as well as the current structure of 10% for the federal government, 55% for states, and 35% for local governments. The FG’s proposed model shifts VAT attribution to the place of consumption, which has raised concerns among northern governors. They fear it could reduce their revenue due to lower consumption levels and economic activity in the north, exacerbating existing economic disparities.

The NGF’s formula attempts to balance the need for equity and derivation-based distribution; however, it falls short of addressing the critical issue of incentivising states to enhance their revenue generation capabilities. Northern governors, in particular, argue that the proposed tax reforms could deepen economic inequalities between the North and South. Northern regions already contend with higher poverty rates and lower industrialisation levels, making them more reliant on federal allocations.

Our recent report, ‘Much Ado About Taxes’, highlighted an alternative perspective. Survey respondents from the formal and informal sectors recognised that the tax reform bills could push states, particularly in the North, to improve their revenue generation capabilities, fostering greater industrial competitiveness. Yet, the report also flagged a significant concern: the planned gradual increase of the VAT rate from 7.5% to 15% by 2027, which respondents feared could exacerbate inflationary pressures. The proposed reforms aim to improve revenue sharing by prioritising derivation (60%), followed by equality (20%) and population (20%). This marks a departure from the current structure and reflects an attempt to address consumption patterns.

While this formula has merit, it has ignited debates about its political and economic implications. Tax reform in Nigeria is not merely economic; it is deeply political, with far-reaching consequences for governance and intergovernmental relations. The Taiwo Oyedele-led tax reform committee faces a delicate balancing act: crafting a framework that drives economic efficiency while maintaining political stability. A key critique of the reforms is their limited focus on motivating states to increase IGR. While the reforms’ emphasis on derivation is intended to reward states with higher economic activity, they do not adequately address structural barriers that hinder revenue generation in less industrialised states.

Without complementary policies to foster industrialisation and economic diversification in these regions, the reforms risk perpetuating existing disparities. The tax reform bills represent a significant step forward in Nigeria’s fiscal policy landscape. However, their success will depend on thoughtful implementation and the resolution of contentious issues, such as the VAT-sharing formula. As the reforms progress, it is crucial to prioritise measures that incentivise all states to enhance their economic capacities while ensuring equitable resource distribution. Only then can Nigeria achieve a more balanced and sustainable fiscal system.