Down the ranks

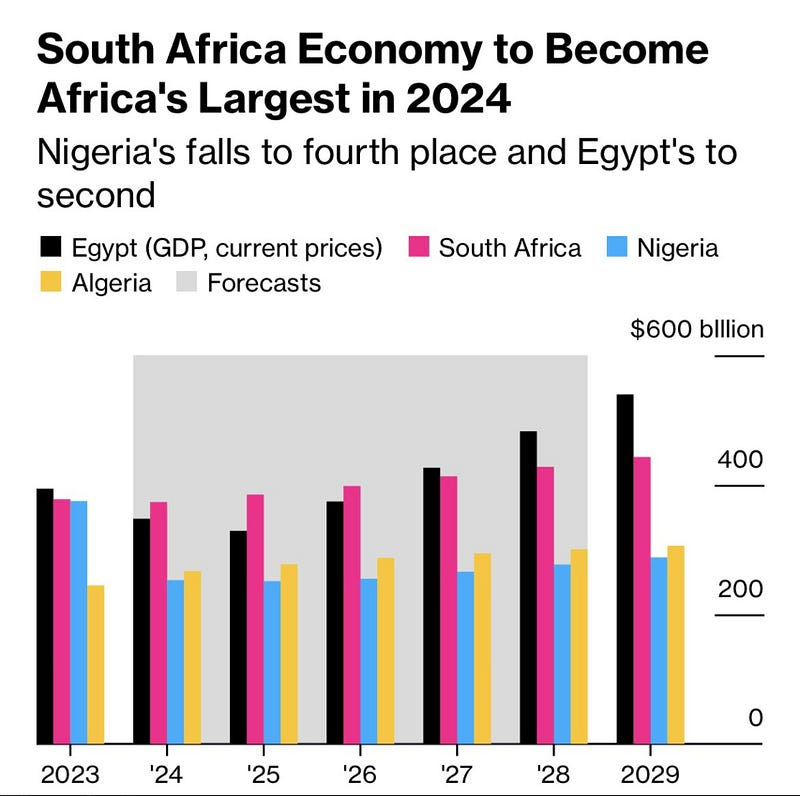

Nigeria’s economy, which ranked as Africa’s largest in 2022, is set to slip to fourth place this year after a series of currency…

Nigeria’s economy, which ranked as Africa’s largest in 2022, is set to slip to fourth place this year after a series of currency devaluations, International Monetary Fund (IMF) forecasts show. As reported by Bloomberg, the IMF’s World Economic Outlook estimated the country’s gross domestic product at $253 billion based on current prices this year, behind North African powerhouses Algeria at $267 billion, Egypt at $348 billion, and South Africa at $373 billion. The report added that South Africa will remain the continent’s largest economy until Egypt reclaims the mantle in 2027.

For decades, economists have argued that the Naira was overvalued, and that had caused Nigeria to become an import-dependent economy, basically because a strong currency makes imports cheaper while a weak currency disincentivises imports. Before the CBN floated the Naira in 2023, economists suggested that the true value of the Naira based on purchasing price parity was around ₦950/$. As of 24 April 2024, the Naira is exchanging at ₦1,240/$, meaning it is slightly undervalued and is a key reason why Nigeria’s economy is estimated at $253 billion, the lowest in decades. Meanwhile, Nigeria’s drop in GDP is a testament to the country’s disastrous economic management over the last decade. A total inability to improve productivity, enhance competitive advantage and drive new landmark growth areas that can open up the economy, like the GSM revolution and banking reforms from the early to mid-2000s, led the country here. Policymakers’ failure to decisively tackle insecurity, resolve bureaucratic bottlenecks, curb corruption and do the hard work required to build a 21st-century economy has led to this decline in economic status. The implications of this will be felt in multiple dimensions: What will be Nigeria’s selling point to foreign investors, and how will we cater to our large population? What’s worse is that the GDP per capita, at $1,100, is now lower than its previous record low — during the civil war in 1968, at $1,268, half of what it was when the All Progressives Congress (APC) came to power. These are the economic numbers that truly matter. The policy choices over the last decade have left Nigeria and Nigerians poorer. Sadly, the leadership keeps repeating those choices. Except Nigeria unlocks another goldmine as it did with telecommunications in the early 2000s, the road to recovery will be long and painful — especially with the unravelling situation in the Middle East and the fast-paced growth of other African economies.