Ebbing away

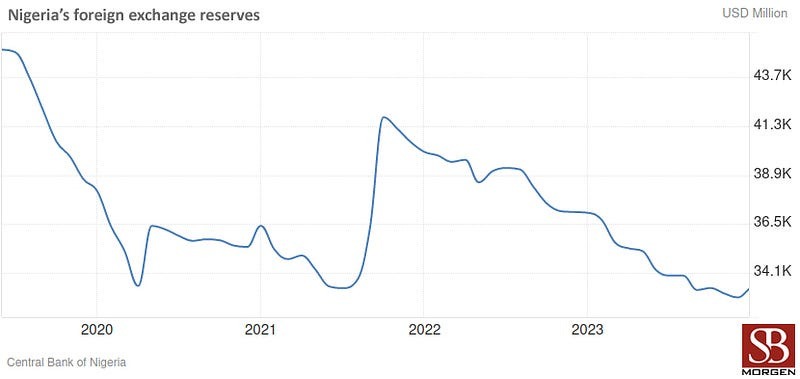

Nigeria’s foreign exchange reserves have decreased by $1.8 billion in 10 weeks, reaching $32.69 billion on 29 May 2024 from $34.44 billion…

Nigeria’s foreign exchange reserves have decreased by $1.8 billion in 10 weeks, reaching $32.69 billion on 29 May 2024 from $34.44 billion on 18 March. The country’s debt repayments ranged from $276.16 million to $560 million in Q1 2024. The International Air Transport Association (IATA) reported that $19 million in blocked funds remain uncleared due to the Central Bank’s ongoing verification. Meanwhile, the federal government surprisingly admitted that Nigeria will spend ₦5.4 trillion on oil subsidies in 2024, contradicting previous repeated denials. The Finance Minister, Wale Edun, revealed this during a presentation on an Accelerated Stabilisation and Advancement Plan (ASAP).

Nigeria’s declining foreign exchange reserves present a significant challenge to its international trade. These reserves are crucial for facilitating global commerce, providing liquidity to pay for imports and support exports. As reserves dwindle, Nigeria’s ability to import essential goods is restricted, adversely affecting manufacturers and consumers. Over the past few years, Nigeria’s foreign reserves have oscillated between $31 billion and $44 billion, and analysts have observed a correlation between the foreign reserves and the strength of the Naira. Simply put, when the foreign reserves exceed $35 billion, the CBN is usually more active in its market interventions. When the level drops to the low 30s, it eases off on spending the reserves. That being said, there is a heightened risk of the naira losing more of its value unless the Federal Government/CBN can attract more dollars to its reserves. Currently, Nigeria’s foreign exchange earnings are predominantly derived from oil exports. This heavy reliance on a single commodity makes the economy highly vulnerable to fluctuations in global oil prices. Nigeria needs to diversify its exports by investing in manufacturing and agriculture to bolster its foreign exchange reserves. The country’s ability to absorb the global shocks during the 2008 global financial crisis and its inability to do so since 2016 falls squarely on how reserves were managed prior to the shocks. By maintaining a balance where the value of exports grows alongside imports, Nigeria can ensure a sustainable inflow of foreign currency. Having said that, it is a positive development that Nigeria has finally honoured its obligations to the airlines to repatriate their trapped funds. The FG appears to have paid over $830 million owed to foreign airlines within the past year, leaving a residual $19 million. While there is no incontestable link between this and the reduction in the foreign reserves, it is safe to assume that this, along with the servicing of due foreign debt repayments and the CBN’s intervention in the FX market, are key drivers of the drop in the reserves. The CBN must expedite the resolution of outstanding claims and streamline the remittance process. A stable and predictable financial environment is critical for maintaining robust international travel and trade. We applaud the efforts of the authorities to clear up the backlog that should not have existed in the first place. Unfortunately, as one great thing happens, a terrible thing happens alongside. The finance minister’s acknowledgement that petrol subsidies are back with a bang and that the government expects to spend up to ₦5.4 trillion (approximately $3.6 billion) is bad news. President Tinubu’s announcement that Nigeria’s fuel subsidy regime would be ended was expected to herald economic rationalisation. Paradoxically, subsidy payments are now projected to be higher than ever. The root of this conundrum lies in the significant depreciation of the naira, which has experienced a devastating loss of value and dramatically increased the cost of importing fuel. Nigeria relies heavily on fuel imports to meet domestic demand, so the Naira devaluation has directly translated into higher subsidy costs. This vicious cycle places immense financial strain on the government, exacerbates inflation, raises costs of goods and services and worsens hardship for Nigerians. The government needs to be bold about sticking to the path of subsidy removal, not just making announcements and backing down when the withdrawal symptoms hit.