Failed on arrival

The Nigerian National Petroleum Corporation Limited (NNPCL) revealed that a $3 billion crude repayment loan agreement with Afrexim Bank has…

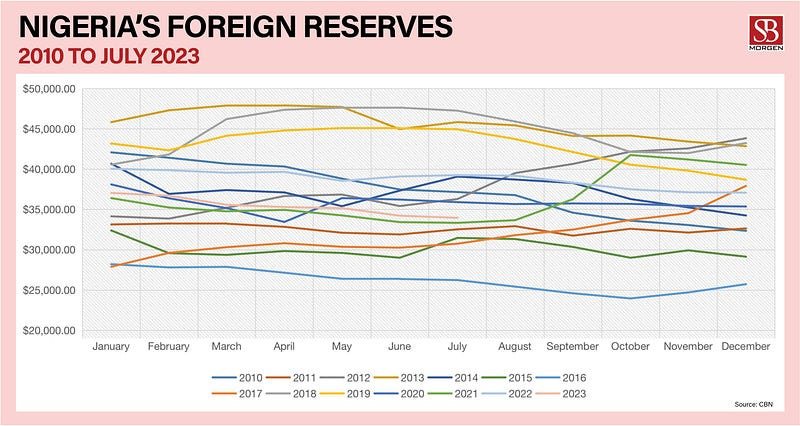

The Nigerian National Petroleum Corporation Limited (NNPCL) revealed that a $3 billion crude repayment loan agreement with Afrexim Bank has stalled as other lenders intended to participate backed out. Afrexim was to contribute $250 million to attract additional lenders, but concerns about exposure to Nigeria and the NNPC MD’s announcement that the money would be used to shore up the Naira made other lenders hesitant. Meanwhile, the Central Bank of Nigeria’s gross reserves have not increased since the announcement, remaining at $33.68 billion. The West African region already accounted for 45% of Afrexim Bank’s loans in Q1 2023, and doubts surround the rushed announcement amid Nigeria’s financial challenges and oil theft issues.

Several aspects of this development are concerning. First, the NNPC MD rushed to make an announcement before the loan agreements were fully executed and everyone irrevocably committed. This is not circumspect behaviour from Mr Kyari. The NNPC’s announcement that it would use a loan to prop up the Naira has made the company look like an unstable partner to potential investors in the petroleum sector. This could have contributed to the difficulties the company has had in securing the loan. This is why the NNPC must focus primarily on its core role of oil production and sales. The NNPC does not have experience in managing monetary policy. Engaging in monetary policy, which falls under the CBN’s jurisdiction, should not extend to the point where its Managing Director publicly expresses intentions to assist the President in bolstering the local currency through a loan facility. If anything, the impact of such an incident on monetary policy should be indirect, and loans must primarily serve the specific purposes outlined by the lenders. Using a loan for monetary policy would be a misuse of funds and could lead to financial problems for the company. A thorough privatisation of the NNPC would address these concerns and subject the company to market forces, which would force the company to compete for customers and investors, leading to better performance and more accountability. In addition, it is clear that the loan’s purpose was not properly disclosed in the discussions before this public announcement, and except for AFREXIM, which has politico-economic reasons, lenders who are primarily assessing the loan as a viable transaction can see what we have said since its announcement: borrowing to shore up a currency will only plunge the country into more crisis. Nigeria’s foreign reserves and the CBN’s ability to defend the Naira are in challenging situations. Revenues from oil sales have been below expectations despite high crude prices. Last week, JP Morgan estimated that Nigeria’s net foreign reserves could be as low as $3.7 billion after considering the CBN’s obligations and commitments. Thus, the news that the $3 billion crude repayment loan deal with Afrixim Bank has fallen through is another punch in the gut of Nigeria’s economy. Any thoughts that a quick fix is possible should be discarded, and sleeves should be rolled up for the work ahead. Further devaluation of the Naira is likely; more investors might take out their remaining funds from Nigeria as the announcement will make potential partners get cold feet. The way forward is for the Nigerian government to realise that the country cannot strengthen its currency, leading to the consideration of opportunities that a depreciated currency presents: fostering export discipline and boosting productivity.