Fast and loose

Nigeria’s House of Representatives raised the Ways and Means advances from 5% to 10% at an emergency plenary session led by Speaker Abbas…

Nigeria’s House of Representatives raised the Ways and Means advances from 5% to 10% at an emergency plenary session led by Speaker Abbas Tajudeen. This increase follows CBN Governor Cardoso’s halt on lending until previous debts were repaid, citing economic challenges. Although initially proposed to be 15%, the limit was reduced to 10% after debate. Minority Leader Kingsley Chinda argued for 2% to ensure accountability, while Finance Committee Chairman James Falake supported the increase for economic survival. Despite opposition, the Deputy Speaker approved the 10% increase, leading some lawmakers to stage a walkout in protest.

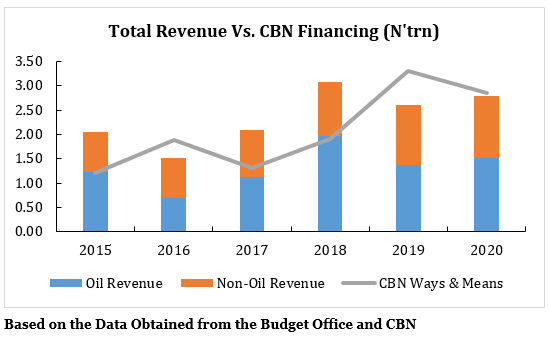

The ways and means advances constitute a short-term loan from the central bank to the government to bridge revenue shortfalls. It is a tool that should be used sparingly and as a last resort, not as a routine mechanism to finance recurrent expenditure. Yet, Nigeria has become increasingly reliant on this financial crutch, a practice that undermines monetary policy, fuels inflation and raises debt sustainability concerns. The Nigerian House of Representatives’ decision to double the limit on ways and means advances to the central bank from 5% to 10% of the previous year’s revenue is a move that would have been less alarming if this were a government with a proven track record of fiscal prudence. However, Nigeria’s history of lavish spending and mounting debt makes this decision a red flag. It is counterproductive that the current government has struggled to address the huge fiscal mess left by the previous administration, which heavily relied on ways and means financing. By securitising this debt, the current government has only created long-term liabilities while borrowing further through the same means after recently coming to power. Despite this, it has gone ahead to loosen the fiscal responsibility limits — limits the previous government ignored — contributing significantly to the current runaway inflation and near fiscal collapse. The central bank’s independence is crucial for maintaining price stability and economic growth. When it is forced to become a de facto financier of government deficits, its ability to effectively manage monetary policy is compromised. This can lead to a vicious inflation cycle, currency depreciation and economic stagnation. Moreover, the lack of public outcry over this decision is disheartening. If Nigerians were more attuned to the dangers of excessive government borrowing and the importance of fiscal discipline, there would likely be a far greater uproar. Unfortunately, a sad — but understandable — collective ignorance has allowed a culture of impunity that lets politicians make reckless decisions without facing significant consequences to fester. We believe this indicates that the Tinubu government will heavily rely on ways and means financing and will likely continue to raise the limit when it suits them, undermining the very intent of fiscal responsibility.