Fast credit

The International Monetary Fund’s executive board approved a $3 billion, three-year loan programme for Ghana, allowing for an immediate…

The International Monetary Fund’s executive board approved a $3 billion, three-year loan programme for Ghana, allowing for an immediate disbursement of about $600 million. The IMF said securing timely debt restructuring agreements with external creditors would be essential to implement the Extended Credit Facility loan successfully, to help Ghana overcome immediate policy and financing challenges, mobilise additional external financing from development partners and provide a framework for completing its debt restructuring. Also, the Fund’s staff and Kenya have reached an agreement that could unlock more than $1 billion of new financing, which could help relieve pressure on the government’s finances.

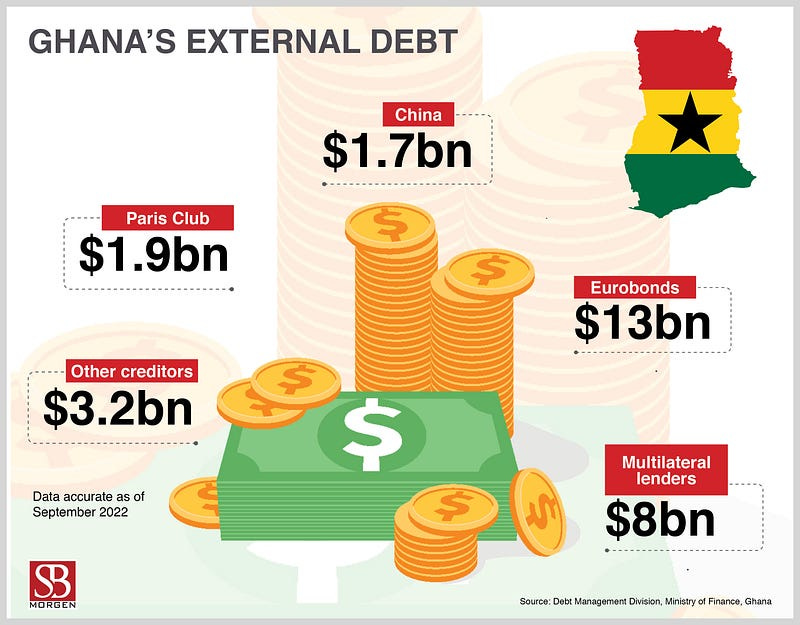

In less than 11 months, Ghana has been able to wade through all necessary conditions to obtain the much-anticipated IMF $3 billion bailout support. The most difficult part in checking all the boxes had to do with debt treatment at both domestic and external levels; for now, domestic debt restructuring is a done deal — participation rate was estimated at 85% with banks, insurance companies and individual bondholders heavily involved. For now, approval from external creditors is enough to grant Accra access to the first tranche of the cake, $600 million. Beyond mere assurances, Ghana’s government must reach an agreement with all external creditors on the nature of debt restructuring. According to the Finance Minister, Ken Ofori-Atta, the magnitude of haircuts international creditors are willing to take is still unclear. Already, the IMF has indicated that Ghana’s entire 3-year programme will demand a Balance of Payment support worth over $15 billion. The Fund revealed Ghana’s payment financing gap for this year is projected to hit more than $4.2 billion. To help finance the gap, the IMF has committed to disburse about $1.2 billion with an additional $530 million from the World Bank. For Ghana to finance the remaining $2.5 billion without depleting its external reserves, it must take steps to obtain debt relief from all its international creditors. In Zambia’s case, although it received approval from the IMF executive board to start its $1.3 billion programme, it has still been unable to receive disbursement(s) due to its inability to convince external creditors, including China, to take haircuts. Unlike Ghana and Zambia, the IMF doesn’t see Kemya as a debt restructuring candidate. Kenya has a $2 billion Eurobond maturing in June 2024, and the country’s central bank governor has indicated that the government was “quite relaxed” about it. Getting an IMF programme without debt treatment as a condition is relatively easier. This makes Kenya’s IMF talks pretty cool and different. While Zambia is stuck in a debt frenzy, Ghana seeks to use the IMF bailout window to renegotiate debts towards saving about $10.5 billion. Ken Ofori-Atta looks forward to a fruitful engagement with Ghana’s bilateral and private creditors in the days ahead although he is unsure of the type of haircut they will agree to take. Meanwhile, the success of China’s Belt and Road Initiative changed international finance and economic development in the Global South in a way that has not been seen since the Marshall Plan. It has expectedly drawn criticism from China’s geopolitical rivals in the West, who accuse it of engaging in debt-trap diplomacy that, when broken down, aims to rope African and lower-income countries into China’s sphere of influence with loans that these countries have little to no capacity to pay for within a foreseeable period. However, as with others, the data and reality have painted a different picture in Ghana’s case. Among the top five external debts Ghana owes, Chinese debt ranks lowest with $1.7 billion. On the other hand, it owes Western lenders a lot more: the Paris Club: $1.9 billion; multilateral lenders: $8 billion; and the highest is Eurobonds at $13 billion. The IMF’s recently approved $3 billion loan adds to the list, whose new entrants push the Chinese debt lower the rank. In essence, the idea of the Chinese debt trap is white noise that holds little in terms of substance. When both IMF and Chinese loans are compared, the one advantage the IMF has over China is that Ghana was forced to embark on austerity measures before the loans were approved. The Chinese never bothered to venture into that sphere. In its own right, the IMF requirements are a good thing for the kind of fiscally irresponsible governments that many countries in Sub-Saharan Africa regrettably have.