From bailout to build-out

Ghana has signed a $344 million debt restructuring deal with the UK, restarting key infrastructure projects as an IMF review begins.

Ghana has signed a bilateral debt restructuring agreement with the United Kingdom, unlocking funding for stalled infrastructure projects while the International Monetary Fund (IMF) starts its fifth review of the country’s $3 billion bailout. Finance Minister Dr Cassiel Ato Forson and UK Trade Commissioner to Africa John Humphrey signed the deal in Accra. The restructuring covers more than $256 million and will allow the resumption of five priority projects, including the Bolgatanga Road, Obetsebi Lamptey Interchange Phase 2, Kejetia Market Phase 2, Tema Aflao Road, and the Komfo Anokye Teaching Hospital Maternity project. Dr Forson said the agreement would ease financing pressures and encourage other creditors to conclude similar deals, helping to fund the 2025 budget. The IMF team, led by Mission Chief Stéphane Roudet, will spend two weeks in Accra assessing progress on the $3 billion Extended Credit Facility. The review will examine arrears, weak bank balance sheets, and concerns over reserves despite policy rate cuts. If successful, Ghana will unlock a $360 million tranche in October, bringing total disbursements since May 2023 to $2.3 billion. The programme runs until May 2026 and seeks to restore debt sustainability, control inflation, and create conditions for private-sector growth.

Ghana’s recent bilateral debt restructuring agreement with the UK is a significant development, offering a tactical reprieve and a broader signal in the nation’s ongoing debt diplomacy. By unlocking approximately £256 million ($344 million) and restarting critical stalled infrastructure projects, Accra has not only eased immediate fiscal pressure but also sought to build momentum for a wider creditor consensus. The emphasis on visible, politically salient projects underscores the government’s dual imperative: stabilising macroeconomic conditions while demonstrating tangible benefits to a restive public grappling with austerity.

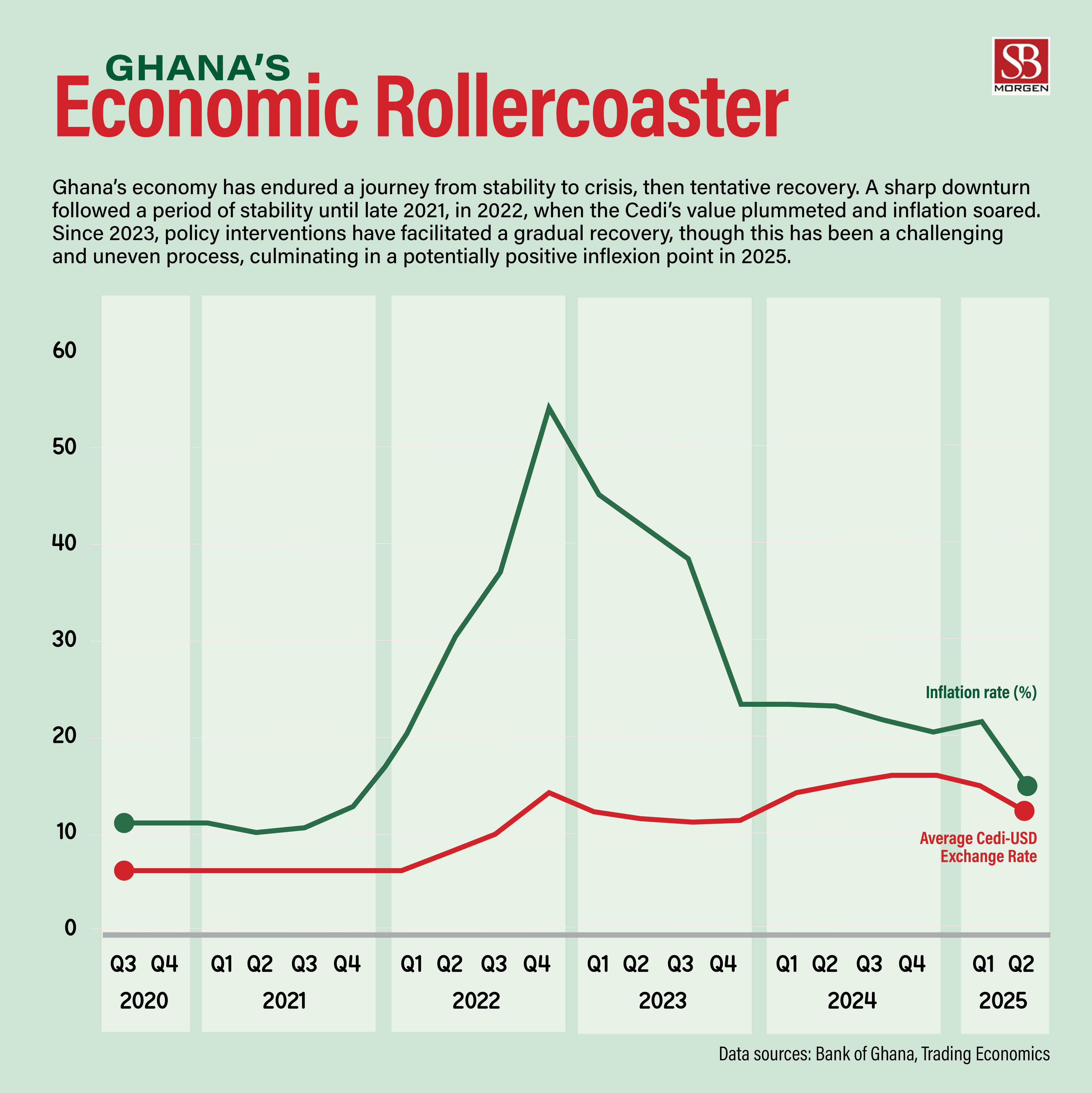

Simultaneously, Accra has been actively working to rebuild credibility through macroeconomic stabilisation. Several recent milestones have bolstered Ghana’s position: the cedi was the world’s best-performing currency in the second quarter of 2025; inflation has fallen back into single digits after peaking at 54%; and buoyant gold exports—projected above $15 billion this year—have strengthened external buffers. These achievements have improved Ghana’s sovereign risk profile, leading ratings agencies to move its outlook into stable territory. By signalling policy traction to official creditors and private investors, Ghana aims to address remaining pressing issues like debt arrears, fragile bank balance sheets, and concerns over dwindling reserves.

For the IMF, the UK deal provides a useful proof point that Ghana’s restructuring framework is holding. However, it also raises questions about whether similar bilateral deals can be concluded quickly enough with non-Paris Club creditors, particularly China, to lock in durable debt relief.

Beyond the technicalities, this episode highlights the new realities of African sovereign debt management. Countries like Ghana are operating within overlapping arenas: domestic political expectations, IMF conditionality, and a fragmented creditor landscape where bilateral partners and private bondholders must be persuaded one by one. The UK deal is therefore less a breakthrough than a foothold in a longer negotiation.

For Accra, success in this phase may unlock further external financing and reinforce investor confidence. Failure, however, risks entrenching a cycle of stopgap bailouts and unfinished reforms that have dogged Ghana since its first IMF programme in 1966.