Ghana’s FDI Conundrum

Ghana scraps its foreign investor capital requirement to boost investment, while simultaneously imposing new forex restrictions on corporations.

Ghana has announced the removal of its minimum capital requirement for foreign investors, aiming to boost foreign direct investment and enhance economic competitiveness. President John Mahama outlined the reform as part of broader efforts to revitalise the economy, attract global capital, and stimulate job creation. By eliminating this financial barrier, the government seeks to foster entrepreneurship and position Ghana as a more accessible investment destination within the region. Meanwhile, the Bank of Ghana has restricted large corporations from withdrawing foreign currency without equivalent prior deposits, to curb pressure on the cedi and stabilise the forex market. Critics argue the measure could harm legitimate business operations and encourage black market activity.

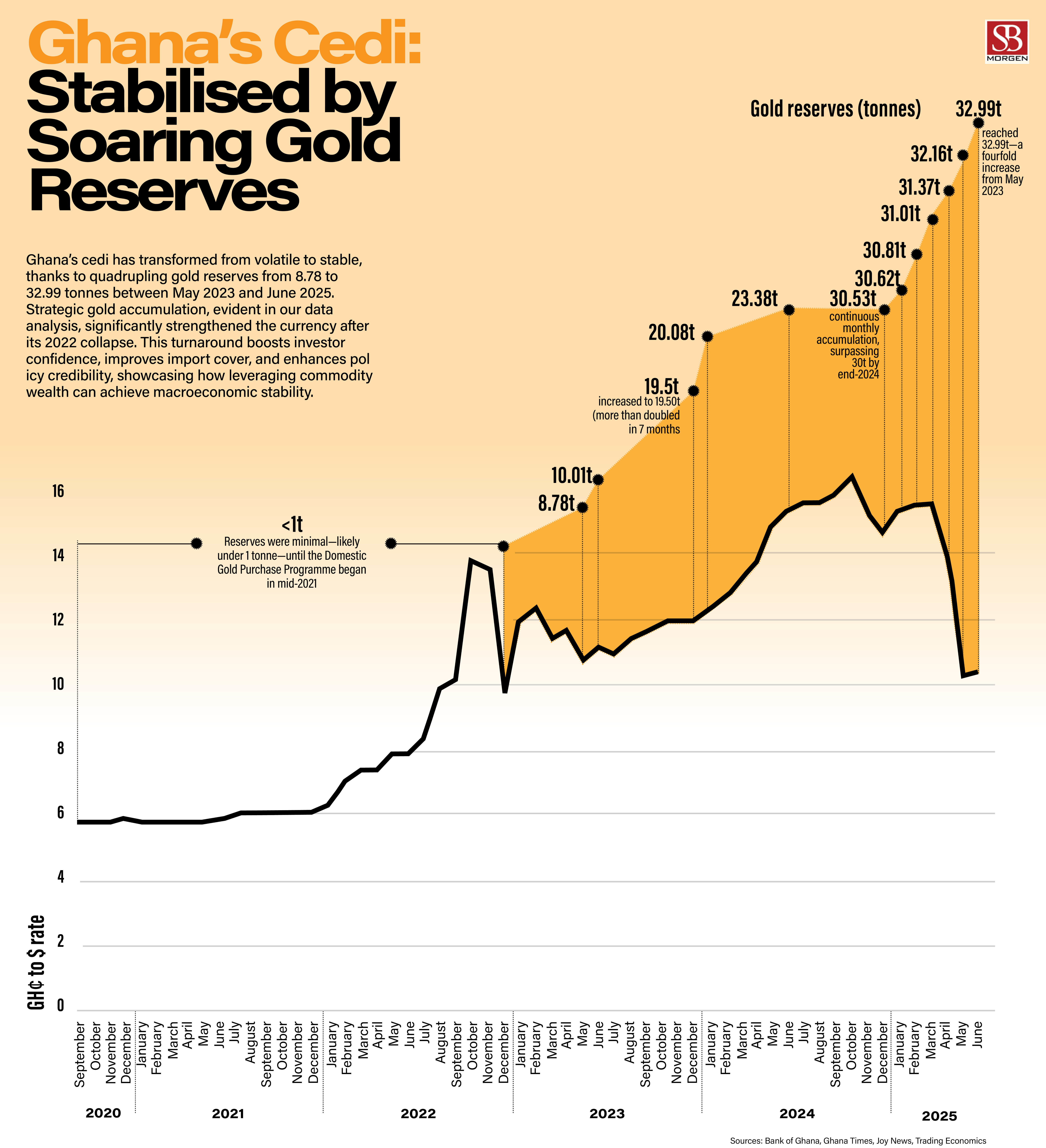

Foreign direct investment into Ghana has seen a dramatic fall over the last decade. Inflows have contracted sharply from a peak of nearly $5 billion in 2012–2013 to under $700 million by 2024. This reflects a significant decline in investor confidence, largely driven by persistent macroeconomic challenges. Inflation soared to 54% in December 2022, and the Ghanaian cedi became the world's worst-performing currency against the US dollar.

Beyond macroeconomic instability, foreign investors have also been frustrated by structural barriers and policy contradictions. The government has continued to court foreign investment, citing recent improvements in macroeconomic indicators, but new policies have raised further concerns. The central tension is between two contradictory approaches: liberalising investment policy while simultaneously tightening foreign exchange controls.

On the one hand, the government has announced an ambitious liberalisation of its investment regime. President John Mahama has proposed removing the minimum capital requirements under the Ghana Investment Promotion Centre (GIPC) Act. These stipulations previously required foreign partners in joint ventures to commit at least $200,000, wholly foreign-owned firms to invest $500,000, and foreign trading companies to provide a minimum of $1 million in capital. Removing these barriers would lower entry costs, particularly for small- and medium-scale investors, and could catalyse entrepreneurial activity, expand job creation, and improve Ghana’s competitiveness against regional peers with more rigid investment thresholds. This reform signals a shift toward a more inclusive investment regime.

On the other hand, the Bank of Ghana (BoG) has introduced a directive restricting large corporations from withdrawing foreign exchange unless they have equivalent local deposits. This policy, intended to stabilise the cedi, has drawn criticism from multinational firms, especially in the extractive industries. They argue that such restrictions add to operational uncertainty in an already fragile environment. Critics warn that these measures could also incentivise a shift toward the parallel market, further weakening formal financial mechanisms and exacerbating the very volatility the BoG aims to prevent. This continued uncertainty around forex access and repatriation remains a significant deterrent for capital-intensive sectors like energy and mining.

This policy inconsistency has created a mixed message for investors. The removal of minimum capital thresholds is a progressive reform, particularly for sectors such as services, technology, and light manufacturing, which are typically deterred by high entry costs. Yet, the BoG’s restrictions on corporate access to foreign exchange send a more cautious signal.

The underlying tension reveals the strategic balancing act facing Ghanaian policymakers: the need to reinvigorate FDI in a context of declining inflows and fiscal stress versus the need to protect the cedi amid persistent external vulnerabilities. Ultimately, Ghana’s FDI outlook will depend not just on headline reforms but on policy consistency. Liberalisation efforts will fall short if undermined by restrictive monetary measures that erode investor confidence.

For now, businesses seeking entry into Ghana must navigate a dual landscape—one that promises greater openness to investment but remains encumbered by macroeconomic fragility and policy volatility. Success will require not only strategic positioning but also the capacity to manage the risks inherent in Ghana’s evolving political economy.