Honeymoon’s end

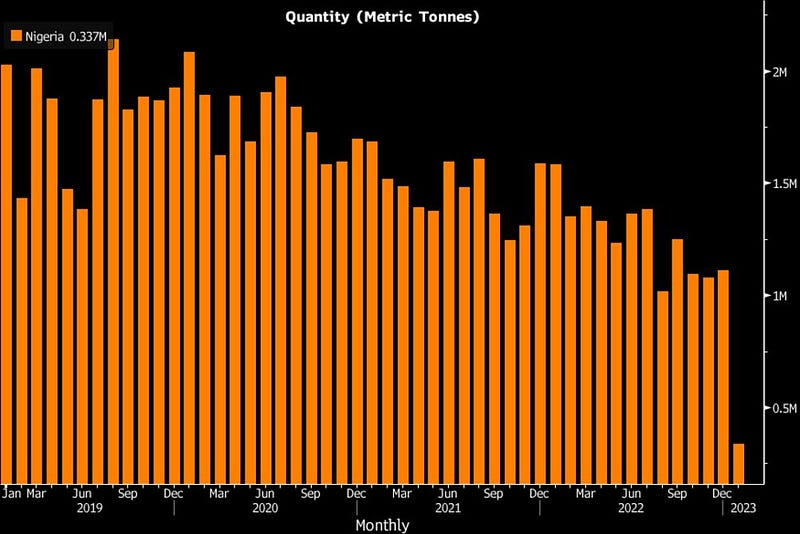

Nigeria’s liquefied natural gas export fell by 15 percent last year, according to the International Energy Agency (IEA). They noted that…

Nigeria’s liquefied natural gas export fell by 15 percent last year, according to the International Energy Agency (IEA). They noted that the biggest export declines occurred in Nigeria, Algeria, and Angola. Algeria and Angola’s supply dropped by 13 percent and nine percent, respectively. The IEA said that Africa is the only exporting region where production decreased in 2022 by six percent. Globally, LNG supply growth was relatively modest in 2022 at 5.5 percent, despite an unprecedented rise in LNG demand in Europe following the gradual decline in Russian pipeline gas deliveries throughout the year.

In a year when the market was booming and Europe was hungry for new gas suppliers, Africa was the only continent that supplied less gas in 2022 than in 2021. This reality painted by the IEA stands in stark contrast to African leaders demanding at COP 27 in Egypt that they be unhindered from developing and using their gas resources to power industrialisation, economic diversification and growth. Nigeria’s gas export share loss of 15% is 1% more than its average annual export to Europe. The country’s steady gas export industry could not have picked the worst time to battle headwinds. Around July last year, Nigeria Liquified Natural Gas Limited (NLNG) said between 32 and 40 percent of its refining capacity was offline. In October, it declared force majeure due to flooding in key production sites. NLNG depends on gas supply agreements with oil-producing companies that have seen their pipelines compromised by oil theft, including in Bonny, where the gas refiner is located. The cherry has slowly been chipped at for some time now. In 2021, NLNG exported 23.3 billion tons of LNG, compared to 28.7 billion in 2020, according to S&P. The company’s total capacity is 31 BCM. Besides low-hanging fruits in the retinue of issues that explain Nigeria’s export decline, the most pressing remains instability and volatility in resource-producing areas. The Niger Delta has been home to violent militant agitation going back at least three decades since the amnesty deal between the government and the agitators in 2009 was partially solved. Since then, the federal government has utilised such strategies as deploying the military and paying militants to guard the same pipelines they destroy in their demonstrations. Last year’s multi-billion naira pipeline surveillance contract awarded to former warlord Government Ekpemopulo (aka Tompolo) further buttresses the notion that the state’s capacity to manage its resources is no longer adequate, and the government does not trust it in the face of mounting oil theft allegations implicating senior security and defence officials. Beyond the primary locations in the Niger Delta, another reason for this decline is hinged on the siege the country faces: it is struggling to optimise production, and the gas produced cannot take an alternative land route to ready European markets because the Trans-Saharan gas pipeline, which connects Nigeria through Niger to Algeria’s terminals in the Mediterranean, passes through a retinue of security challenged routes filled with armed groups. With the other major gas producers on the continent, Algeria and Egypt, being closer to Europe and showing more seriousness with their gas intentions, they would be at the front of the gas investment queue and the heart of gas geopolitics. Algeria, for example, decreased supply to Spain due to a spat over Western Sahara while compensating by increasing supply to Italy. Egypt produces less than Algeria at the moment, but its consumption and production dwarf Nigeria’s. In 2022, the country’s petroleum ministry said it boosted gas supply to Europe by 14%. Although Egypt does not have Nigeria’s LNG capacity, it produced 71 BCM of gas in 2021 and domestically consumed 87% of that. To make more money from Europe’s needs, the country had to ration electricity supply. While these two countries, now Africa’s first and second largest gas producers, respectively, have less proven reserves than their West African competitors, they are firing their economies and making haste before sunset. Nigeria has seen flat to negative growth, and key investment decisions have been halted by souring economic fundamentals. Worse, the domestic market is not large enough to incentivise continued investment. Algeria’s domestic consumption of 45.8 BCM in 2022 is roughly equal to Nigeria’s total gas production of 49–52 BCM in 2020 and 2021. The general issues afflicting the oil industry have caught up with the LNG sector. It was assumed that the gas sector was insulated from these issues for years. Systemic issues, however, are difficult to insulate against, and Nigeria’s gas troubles are only another expression of this fact. The country is in a race against time to boost gas production and domestic consumption before its valued treasure trove becomes a global also-ran.