Low current

Nigeria’s currency-in-circulation has dropped to its lowest level since 2008 due to the Central Bank of Nigeria (CBN)’s currency redesign…

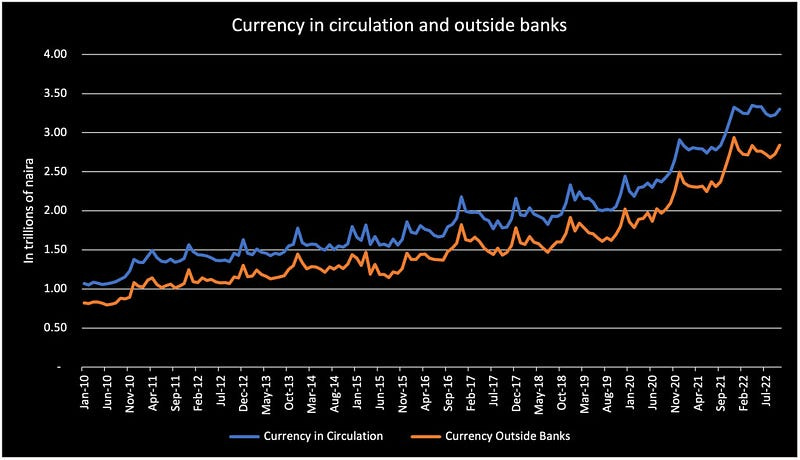

Nigeria’s currency-in-circulation has dropped to its lowest level since 2008 due to the Central Bank of Nigeria (CBN)’s currency redesign policy, according to BusinessDay. The CBN’s data reveals it declined by 29.2 percent to ₦982.1 billion in February 2023, the second straight month of declines. The February 2023 figures represent a 69.9 percent year-on-year increase from February 2022. Nigeria Inter-Bank Settlement System (NIBSS)’s data show that the total volume of NIBSS Instant Payment platform (NIP) transactions rose by 45.6 percent to 787.9 million in February from 541.7 million in January.

This data suggests that it is mission accomplished for the CBN, whose ill-implemented currency redesign policy has had the effect of sucking a ton of cash out of circulation. It is worth restating that before October 2022, a ₦2.7 trillion pool, which was swimming outside the banking system (out of total money circulation of ₦3.23 trillion), constituted an elephant which stood in the way of the CBN getting a handle on inflation management using its monetary tools. Also positive is the fact that online transactions are growing, suggesting that the economy is still functioning, although the blunt implementation of the policy has hammered the informal sector. While inter-bank transfers have increased, the general experience has been that they have proven unreliable for many Nigerians. In many cases, they have been unable to handle many of the informal micro-transactions that prevail in Nigeria’s huge informal economy. Various arbitrage systems have emerged to deal with the latent demand for cash that has not been stifled by constrained supply. The CBN constantly sang about its objective to reach 95% financial inclusion by 2024. In illustrating how the naira policy’s disadvantages exceed its advantages, one could argue that the CBN will fall short of meeting its 2024 financial inclusion targets because of its actions. Why? For one, the public’s distrust in the banking sector has grown as the industry’s inability to meet customers’ demands has deepened. This entire process has made it harder, not easier, for unbanked people to access banking services and slowed the adoption of electronic forms of payment. Transaction volumes increased due to the cash crunch, while transaction values fell over the review period by 5%, from ₦38.77 trillion in January to ₦37.79 trillion in February. Due in large part to the limitations of the current infrastructure, instant settlement during the height of the cash crunch failed miserably. Instant payments fell 12.47% between December 2022 and February 2023. This Is not accounting for the amount and value of delayed and deferred transactions. All in all, a critical appraisal of the policy, its implementation, the problems and its short and long-term effects need to be carried out to serve as a cautionary tale to such endeavours in the future. From a monetary policy standpoint, we believe that the CBN will limit cash circulation to the ₦1 trillion level, suggesting that current cash shortages will continue in the short term and the economy is in for some long-term demand destruction on the cash side.