Money matters

Ghana’s government missed its ambitious treasury bills target by a whopping GH¢2.670 billion, securing 64.1% of the GH¢7.438 billion target…

Ghana’s government missed its ambitious treasury bills target by a whopping GH¢2.670 billion, securing 64.1% of the GH¢7.438 billion target for maturing debts and projects. The Bank of Ghana’s auction results revealed an undersubscription of 35.90%. Also, the BoG has adopted a new methodology for calculating its Foreign Exchange (FX) Market Reference Rate (MRR) to better align with international best practices and accurately reflect market developments. Additionally, Ghana’s central bank had its first main interest rate cut since January (GHCBIR=ECI), opening a new tab by 200 basis points to 27% as inflation continues to ease.

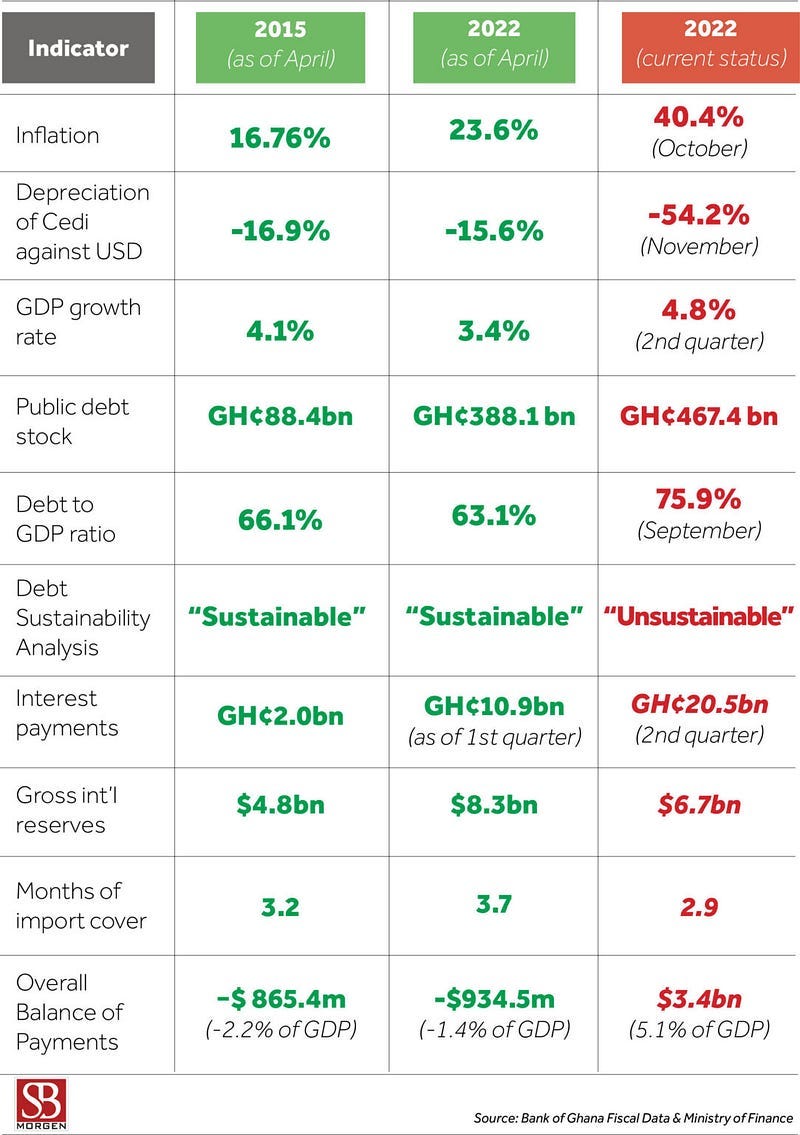

Counsel: A decade ago, the Ghanaian economy was touted as a model for Sub-Saharan Africa. However, recent geopolitical crises, such as the 2016 commodity price crash and the 2020 COVID-19 pandemic have led to volatile macroeconomic conditions, soaring inflation and a depreciating currency. Today, the major issue is a debt crisis that has caused the country to default on its Eurobond payments. A significant reason is that the country exploited its positive economic perception to borrow excessively to fuel development, yet it failed to generate sufficient revenue to service its debt. Ghana’s revenue-to-GDP ratio is around 14%, higher than Nigeria’s 9.4%, but still below the Sub-Saharan African average of 20.5%. Moreover, the Bank of Ghana’s decision to cut the Monetary Policy Rate (MPR) from 29% to 27% was seen as a reactive measure, not aligning with available economic data. Many saw this move as part of a broader effort to reduce the cost of borrowing, particularly as the country edges closer to elections. Consequently, the under-subscription of the Government of Ghana’s T-Bills was expected, with many investors shying away from these government instruments. The anticipation of further rate cuts likely fuelled this reaction, as investors foresee less attractive borrowing conditions in the near future. This year, Ghana’s private sector has had to compete at high costs with the government for access to capital from the T-bill market. The Bank of Ghana’s data reveals that commercial banks have favoured investing in government securities over extending loans to private enterprises. This trend limits credit access for businesses, further escalating borrowing costs. The recent rate cut is a welcome development for the private sector, as it is expected to lower the cost of borrowing. However, this reduction could lead to challenges, especially as it seeks to meet its bloated fourth-quarter financing needs. With a relatively lower rate, there’s a likelihood that the government may receive less than anticipated from future T-bill issuances. Compounding this is the Bank of Ghana’s recent introduction of a new Gold Coin, intended to offer an alternative investment avenue and stabilise the cedi. While this move could provide some relief, the persistent rise in government expenditure, exacerbated by a weakening exchange rate, may create further complications. As government spending grows, the pressure on the Bank of Ghana to hike rates again could increase. This would be aimed at making T-bills more attractive to investors, thereby enabling the government to borrow more to cover its financing needs. Nigeria, being a much more diversified economy, has several levers it can pull to remain solvent, whereas Ghana, with its overreliance on cocoa revenues, has limited options. As a result, investors are sceptical and are likely to avoid Ghanaian debt instruments unless more positive news emerges or the risk premium significantly increases. Consequently, the Bank of Ghana’s recent rate cut is unlikely to provide much relief.