Naira’s new normal

Nigeria’s naira is decoupling from oil prices due to Dangote Refinery’s impact, non-oil exports, and FX reforms, with analysts forecasting ₦1,556/$ stability.

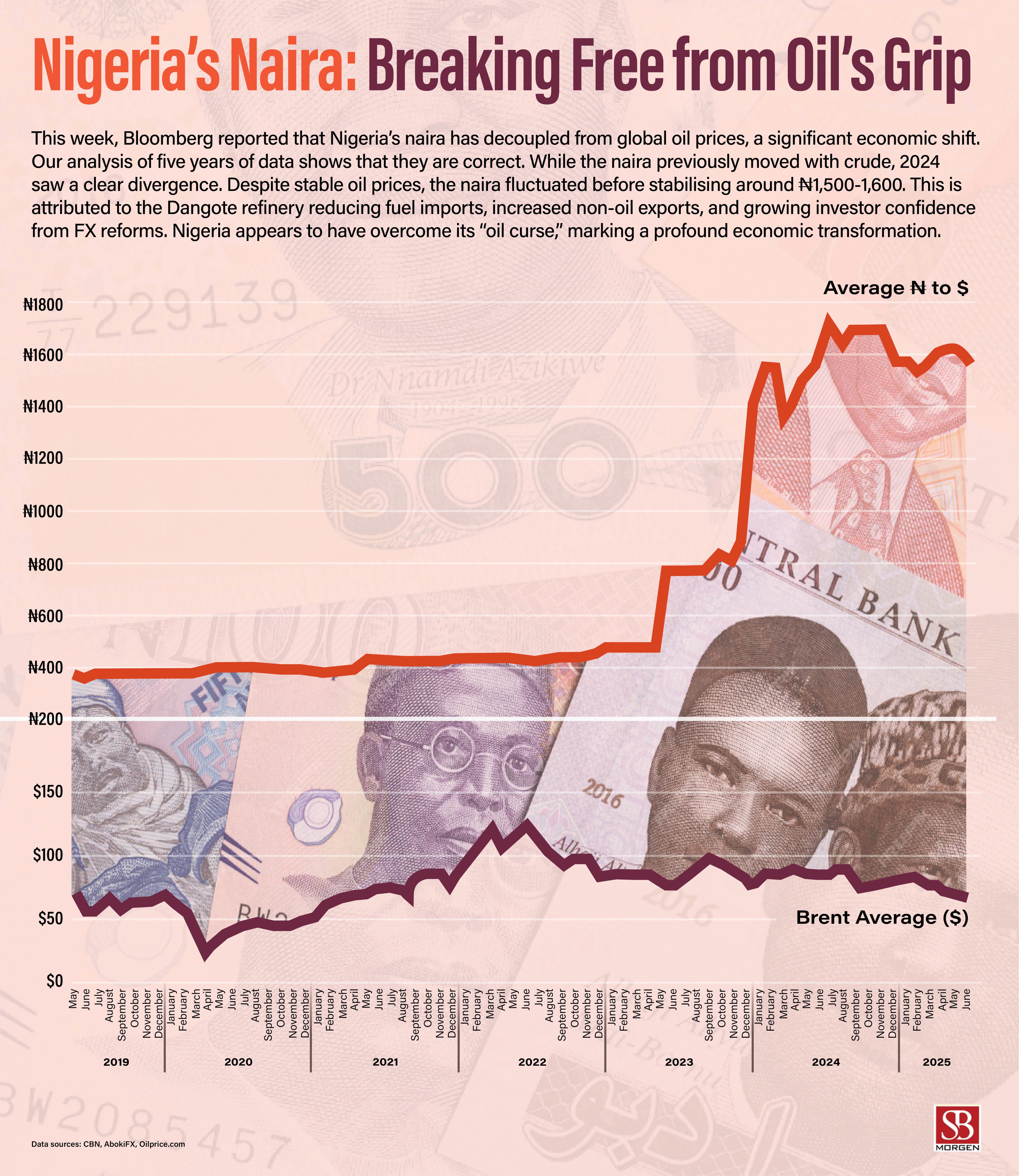

According to Bloomberg, Nigeria’s naira is showing a marked decoupling from global oil price movements, diverging from its historical correlation. Analysts from Deutsche Bank and Cardinal Stone attribute this shift to past undervaluation, rising non-oil exports, and reduced petroleum imports, thanks largely to the operational Dangote Refinery. This transition has made Nigeria a net exporter of refined products, lessening FX pressure. After a 41% drop earlier in 2024, the naira is projected to stabilise around ₦1,556 per dollar by year-end. A weaker US dollar, ongoing FX reforms, and increased investor interest in Nigerian assets have further strengthened currency and market resilience.

Nigeria's naira has experienced a tumultuous journey over the past decade, defined by relentless pressure, policy experimentation, and a painful transition towards market-driven exchange rates. This period began with an official peg of ₦197 to the US dollar in 2015, where the Central Bank of Nigeria (CBN) clung to rigid controls even as crashing global oil prices exposed the currency's severe overvaluation. This initial attempt at artificial stability came at a significant cost, leading to dwindling foreign reserves and growing distortions between the official and parallel market rates, with the latter trading 15-20% weaker. The CBN's rigid control effectively masked underlying vulnerabilities as Nigeria's crucial oil revenues began to decline.

The onset of the COVID-19 pandemic in 2020 starkly exposed these fault lines. With oil prices plummeting to $20 per barrel by April 2020, the naira entered a phase of controlled depreciation, reaching ₦460 to the dollar by early 2023. During this period, the CBN implemented various stopgap measures, from the "Naira4Dollar" scheme in 2021 to new foreign exchange (FX) restrictions. However, these interventions largely failed to address the underlying structural issues. Diaspora remittances and vital portfolio inflows dwindled, while the existence of multiple exchange rates (official, NAFEX, and parallel) created significant arbitrage opportunities, with premiums exceeding ₦100 to the dollar by 2022.

A significant turning point arrived in June 2023 when the CBN attempted to unify the disparate exchange rates. This policy shift triggered a dramatic 23% single-day crash, pushing the naira to between ₦600 and ₦850 to the dollar, as pent-up demand overwhelmed available supply. Despite this "floatation," the CBN continued intermittent interventions while simultaneously hiking interest rates aggressively; the Monetary Policy Rate (MPR) reached 20% by December 2023. This period saw the currency enter a freefall, hitting ₦1,500 to the dollar in early 2024 amidst rampant speculation and a staggering backlog of over $7 billion in foreign exchange demand.

Over the past two years, the naira has lost more than half its value under the Tinubu administration's economic reforms. Currently, the currency is showing tentative signs of stabilisation, trading at approximately ₦1,550 to the dollar (with ranges between ₦1,480 and ₦1,700 to the dollar as of July 2025). This fragile stability has been achieved through brutal monetary tightening, with the MPR reaching 27.5% by mid-2025, and concerted efforts to clear the FX backlogs.

However, this high-cost stabilisation has come with significant collateral damage. The corporate sector, particularly manufacturers, faces borrowing costs exceeding 32%, severely stifling growth. Everyday Nigerians are grappling with inflation exceeding 30%, which continues to erode their purchasing power. Furthermore, investors are demanding hard currency guarantees, reflecting a lingering distrust in the market's stability. While recent naira rallies, also aided by weaker global dollar demand and renewed investor optimism, suggest some progress, they mask deeper structural issues. The operational launch of the Dangote Refinery has positively altered Nigeria’s position as a net importer of refined petroleum products, and a rise in non-oil exports has contributed to the naira's recent performance.

Despite these positive factors, challenges remain. Portfolio investments are inherently volatile and may exit the market as swiftly as they arrived. The modest reinstatement of international naira card transactions by banks, such as GTBank’s $1,000 quarterly limit, pales in comparison to pre-2015 norms. Middle-class Nigerians, battered by inflation and wage stagnation, still face de facto exclusion from formal FX access, forcing many to rely on unofficial channels.

The overarching lesson from the past decade is clear: half-measures, whether partial liberalisation or ad hoc restrictions, only serve to prolong economic crises. To achieve lasting economic recovery, both monetary and fiscal reforms must be consistently maintained and effectively implemented. True price discovery, coupled with policies designed to mitigate the pain of this transition, such as targeted social buffers, represents Nigeria's only viable path to lasting FX stability. Without these fundamental changes, the naira's recurring cycles of volatility and artificial scarcity will inevitably persist, leaving ordinary citizens to bear the brunt of the cost. Nigeria now faces a critical choice between a controlled decline and genuine, comprehensive reform.