Oily shenanigans

Nigeria's crude output hits two-month high (1.486 mbpd April), oil theft drops. Petrol price hike warning countered by Dangote Refinery.

Nigeria’s crude oil production rose to a two-month high of 1.486 million barrels per day (bpd) in April, up from 1.401 million bpd in March, but still below OPEC’s 1.5 million bpd quota. Including condensates, total output reached 1.683 million bpd, though condensates are excluded from OPEC quotas. The country also recorded a 58.3% drop in oil theft in Q1 2025, attributed to improved security and regulatory efforts. Meanwhile, oil marketers warned that petrol prices may surge to ₦1,500/litre if fuel imports are banned, a claim dismissed by the Dangote Refinery, which accused marketers of seeking to justify substandard fuel imports.

The power struggles inherent in Nigeria's oil and gas sector reflect the country's broader political landscape, particularly the contest for control over this crucial industry. A positive development has been the decline in oil theft, largely attributed to the strategic engagement of host community actors in pipeline security contracts. While these arrangements offer welcome economic opportunities at the local level, a critical question arises: what deliberate, long-term development initiatives are being implemented to ensure these communities experience sustainable and lasting benefits that extend beyond their security roles?

Shifting focus to the downstream sector, the recurring proposals to ban the importation of refined petroleum products seem to contradict the fundamental principles underpinning downstream deregulation. Such a move would effectively hand a near-monopoly in the domestic market to the Dangote Refinery, given its unmatched production capacity within Nigeria. This naturally raises concerns about potential market dominance and its subsequent implications for pricing and fair competition. Instead of an outright import ban, a more balanced and sustainable approach might involve the rigorous enforcement of consistent quality standards for all petroleum products sold nationwide. Complementarily, mandating clear labelling of pump types at fuel stations could empower consumers to make informed choices based on both quality and price considerations.

In contrast to the Buhari administration's emphasis on devising new borrowing strategies, the Tinubu administration has notably prioritised boosting Nigeria's crude oil production. Their immediate strategy involves enhancing output from existing wells through consistent maintenance and stimulation efforts. Looking ahead, the longer-term focus has shifted towards facilitating the divestment of International Oil Companies (IOCs) from marginal fields while actively seeking fresh capital to accelerate exploration activities. Although the immediate impact of these production-focused efforts may be limited, crucial questions emerge: what specific timelines and measurable milestones have been established to achieve the stated goal of reaching two million barrels per day within the next year, and what key performance indicators are being used to diligently track progress towards this ambitious target?

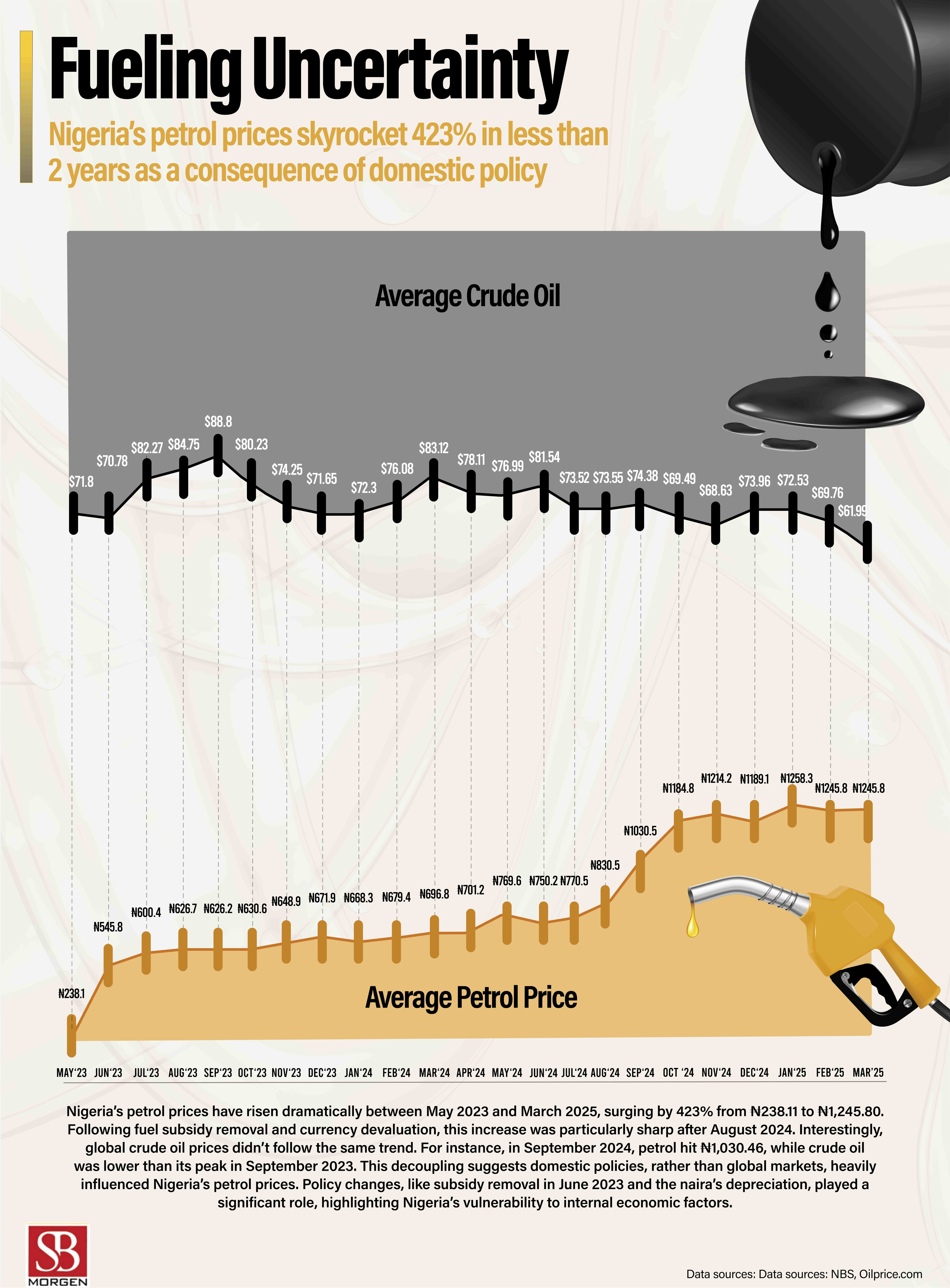

Considering the dramatic escalation in Nigeria's petrol prices, which surged by an astonishing 423% between May 2023 and March 2025 (from ₦238.11 to ₦1,245.80), particularly following the sharp increases after the removal of fuel subsidies and the devaluation of the naira post-August 2024, several critical questions demand attention. Notably, global crude oil prices did not follow a similar upward trend during this period. This decoupling, evident when petrol prices hit ₦1,030.46 in September 2024 while crude oil prices remained below their September 2023 peak, strongly suggests the significant influence of domestic policies on Nigeria's petrol costs. Given this evident vulnerability to internal economic factors such as the June 2023 subsidy removal and the depreciation of the naira, what further proactive measures are being considered and implemented to mitigate the adverse impact of such policy shifts on consumers and ensure greater price stability in the future?

Furthermore, the recent data introduces a concerning possibility regarding the downstream market: could the Dangote Refinery be strategically engaging in price undercutting against importers? This raises a significant question about the evolving long-term market dynamics. What are the anticipated price scenarios for consumers if the Dangote Refinery successfully drives out its competitors and establishes a dominant, near-monopolistic position in Nigeria's petrol market? Critically, what robust regulatory safeguards will be proactively put in place to effectively prevent potential monopolistic pricing practices and ensure the maintenance of fair and competitive conditions within the downstream sector?