On a leash

Nigeria's naira rose 0.6% to ₦1,530/USD, boosted by $23 billion forex reserves and improved oil output, despite equities plummeting.

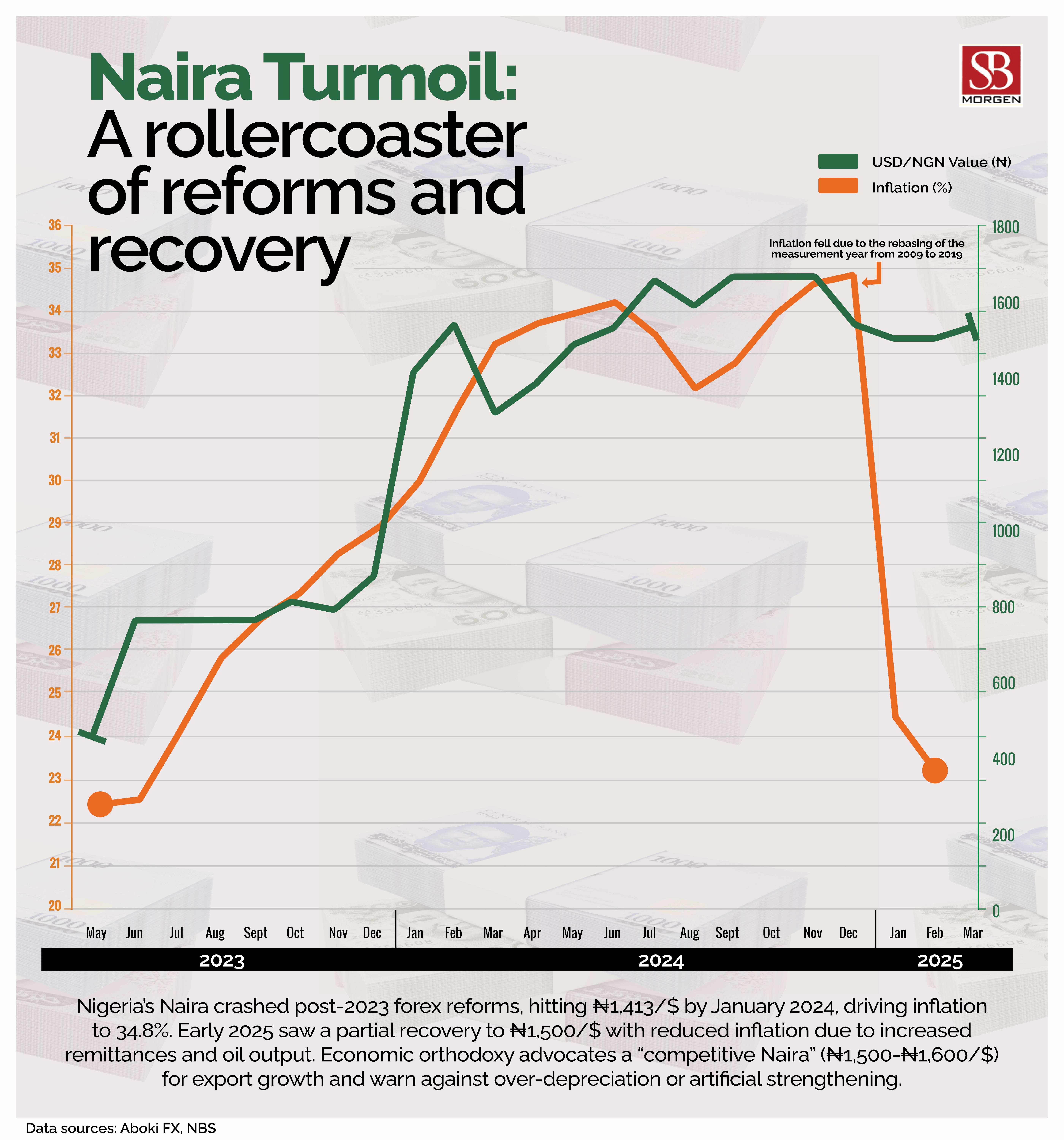

Nigeria’s naira strengthened by 0.6% to ₦1,530/USD, buoyed by the Central Bank of Nigeria’s (CBN) forex reserves reaching $23 billion—the highest in over three years. Gross reserves also rose to $38.33 billion, driven by improved oil output and export conditions. The CBN injected $197.71 million into the FX market to support liquidity amid rising U.S. import tariffs. However, Nigerian equities plunged, with investors losing ₦659 billion as the NGX ASI dropped 1.23%. Market sentiment weakened due to U.S. President Trump’s tariff plans. The Nigerian government has avoided retaliation against Trump’s tariffs but will approach the World Trade Organisation (WTO) for a solution for all parties.

The Central Bank of Nigeria (CBN) has established a trading band for the Naira, aiming to keep it within the ₦1,500–₦1,600 range against the US dollar. When the Naira strengthens beyond this band, the CBN intervenes by purchasing USD to bolster reserves and alleviate pressure. Conversely, when the Naira weakens, the CBN releases USD into the market to increase supply and support the currency. However, the broader macroeconomic landscape reveals underlying vulnerabilities. While notable, the recent appreciation of the Naira seems not to be solely attributable to domestic policy measures. Although the CBN’s reforms and interventions have contributed to relative stability, the global decline in the dollar—prompted by US President Donald Trump's recent tariff rhetoric and protectionist stance—has been a significant factor. Since February, the dollar has weakened against most global currencies, and Nigeria, like many emerging markets, has gained from this trend.

Nevertheless, this benefit may prove to be transient. Oil prices have been trending downwards, and futures indicate a sustained decline. Nigeria, whose economy relies heavily on crude oil exports, is already underperforming in production targets—missing budgeted volumes by nearly 600,000 barrels per day. This gap is expected to widen, further eroding fiscal buffers. However, it is important to note that while oil is a significant export, it accounts for only about 6% of Nigeria's GDP, meaning the direct impact of Trump's tariffs on the broader Nigerian economy is somewhat mitigated. Moreover, despite revisions to the inflation measurement framework, inflation remains above budgeted projections, compounding the pressure on real incomes and consumption. Trump's policy pause—holding back further tariff escalations for 90 days—offers temporary relief to global markets. Yet, if his protectionist agenda resumes in full force, global demand may contract, exacerbating the downward pressure on commodity prices. For Nigeria, this would amplify vulnerabilities. The combination of softening oil prices, underproduction, persistent inflation, and constrained fiscal space points to a fragile macroeconomic environment. Should external shocks persist or intensify, Nigeria risks slipping into recession—or, at the very least, facing a fiscal crisis. While the CBN's Monetary Policy Committee retains some levers to support growth, the economy's structural weaknesses limit the room for manoeuvre. As the global geopolitical landscape grows more unpredictable, Nigeria's ability to withstand further shocks will depend on accelerating structural reforms, improving revenue generation, and rebuilding investor confidence.