On disclosure

Nigeria’s Federal Government has launched an amnesty initiative that allows individuals to deposit foreign currencies into banks without…

Nigeria’s Federal Government has launched an amnesty initiative that allows individuals to deposit foreign currencies into banks without penalties or taxes — provided the funds are not proceeds of crime. The finance ministry’s spokesman, Mohammed Manga, called it the ‘Disclosure Scheme,’ saying the scheme, which would run for nine months, is designed to enhance transparency in the financial sector and boost Nigeria’s economic resilience, growth, and development. Finance minister Wale Edun said, “The disclosure scheme is a bold initiative aimed at integrating foreign currency outside the formal financial system into the formal economy.”

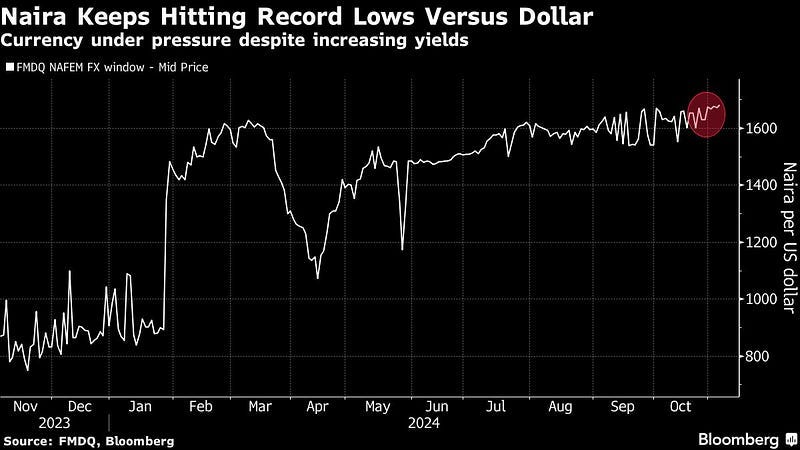

Nigeria’s persistent foreign exchange (FX) scarcity has spurred a series of initiatives by the federal government to stabilise the naira and boost liquidity in the FX market. This new initiative mirrors efforts from the previous Buhari administration, which launched the Voluntary Assets and Income Declaration Scheme (VAIDS) as a tax amnesty programme. Like its predecessor, the Tinubu administration has rolled out a series of initiatives to widen the tax net and reduce dependency on subsidies. The government has made considerable strides in the latter, but in addition to these tax reforms, the issue of foreign currency deposit regulations has come to the forefront as the government seeks ways to stem the excessive demand for foreign currencies, particularly the US dollar, circulating in the economy. Since the beginning of the year, the Central Bank of Nigeria (CBN) has intensified efforts to address the country’s illiquidity challenges. In its latest move, the CBN began supplying dollars to eligible Bureau de Change (BDC) operators while reducing the number of BDCs in operation. Despite these actions, the FX market remains volatile, and the challenges persist. The government’s latest amnesty initiative is expected to increase the supply of dollars, reduce FX rate fluctuations, and stabilise the naira, hoping this will help curb inflation. However, there are several concerns surrounding the sustainability of the initiative. Will people trust the process? Or is it simply a ploy to capture money launderers? The level of acceptance may take time and will depend largely on the transparency with which the government handles the scheme. Given the historical context, it is likely that the public will adopt a “wait and see” approach, wary of the plan’s efficacy. The government’s strategy is to digitise foreign currency transactions, arguing that doing so will make it easier to regulate the market and reduce the supply of dollars in circulation. However, critics caution that as long as there is demand, the supply will continue to find a way to meet it, and the black market will remain resilient. While the digitisation of currency transactions may make it more difficult to track physical dollar movements, it is unclear whether this will have a lasting impact on the FX market or simply push the informal market further underground. What is clear is that the federal government is desperate to secure dollars and address the foreign exchange liquidity crisis, but the success of these initiatives remains uncertain. The long-term viability of these plans will depend on the government’s ability to manage public trust, execute reforms transparently, and address the underlying economic issues contributing to Nigeria’s FX problems. Only time will tell if these strategies will stabilise the naira and bring a more balanced and sustainable foreign exchange market.