On penalties

Foreign exchange transactions conducted outside Nigeria’s official FX window will soon incur excise tax penalties, the Presidential Fiscal…

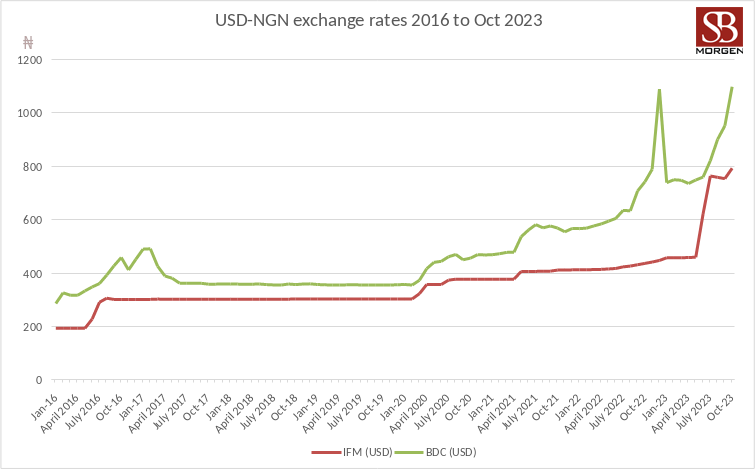

Foreign exchange transactions conducted outside Nigeria’s official FX window will soon incur excise tax penalties, the Presidential Fiscal Policy and Tax Reform Committee, established by President Bola Tinubu, proposed. Taiwo Oyedele, the committee’s chairman, indicated that the committee’s “quick win” recommendations, designed to address pressing economic issues including exchange rate management, the impact of fuel subsidy removal, inflation control and economic growth facilitation, include the imposition of excise tax on foreign exchange transactions conducted outside the official market. This tax on FX transactions is expected to be implemented within 30 days as part of the initial “Quick Wins” phase.

At the surface level, this is a good move. However, a deep dive shows us that this move will not solve Nigeria’s forex liquidity problem because saboteurs cannot be entirely blamed for the naira’s continued depreciation. Legitimate businesses have been waiting on the CBN to honour forward contracts for months! Businesses continue to demand dollars primarily because Nigeria’s economy does not sell much else outside oil. Individuals also feel the need to stockpile dollars or have dollar investments because of the naira’s volatility. The problem, therefore, is a lack of trust in the government’s ability to meet the forex needs of businesses and individuals. Another leg of the equation is that the CBN supplies forex to Bureau de Change operators, who then sell it to travellers. It is uncertain if these transactions are regarded as taking place outside the official channels. FX transactions carried out outside the official window are, by nature, difficult for the government to track. This is why it is called the black market. The government’s proposed measures can elicit either of the following reactions. First, those who trade will simply not move the FX into the country; rather, they will make person-to-person moves abroad and then make a naira-to-naira equivalent moves within Nigeria. It will, therefore, not improve liquidity or drive rates down. Second, people will simply include the tax as a markup on the actual transaction, and only those willing to pay this extra will have access. This will effectively drive the exchange rate up. This type of measure is a classic case of chasing shadows. The real issue is, of course, a lack of supply in the official market and the monetary authorities’ move to control how willing buyers and sellers trade. If these two issues are fixed, the incentives to go outside the official window should disappear. Foreign investors’ primary concern over the past decades has been the multiplicity of foreign exchange windows, official and unofficial. At its peak, Nigeria had more than five recognised exchange rates, including the official market rate (published by the CBN), the Importer and Exporter Window (IEW), the commercial bank rate, the rate for Personal Travel Allowances (PTA) and the parallel market rate. In 2016, when the Nigerian economy was just exiting its first recession in 30 years, the CBN spokesperson explained that special windows with variant rates were created to meet the forex demands of specific critical sectors of the economy. However, like most things in Nigeria, people in authority abused it, leading to cases of opportunistic wealth accumulation. Today, all that is being reversed can be described as a major policy somersault. SBM has always advocated for a unified exchange rate, and it appears that the new CBN administration is focused on achieving this. Hopefully, a unified exchange rate will give the Nigerian economy a stable platform for growth, although the road ahead promises to be turbulent.