Optimistic

The Senate approved Nigeria’s 2025 medium-term expenditure framework and fiscal strategy paper (MTEF/FSP), outlining ₦47.9 trillion in…

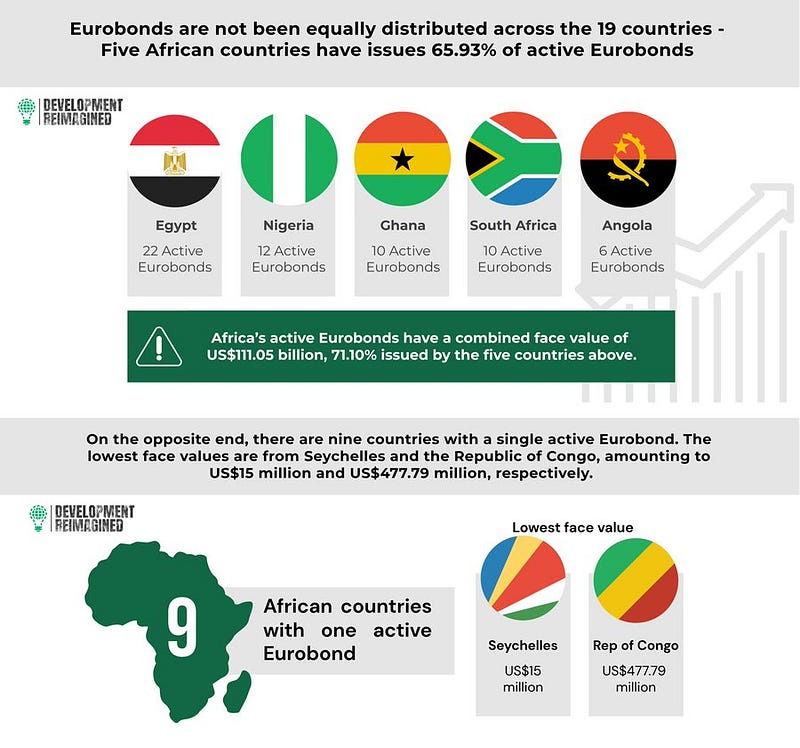

The Senate approved Nigeria’s 2025 medium-term expenditure framework and fiscal strategy paper (MTEF/FSP), outlining ₦47.9 trillion in spending and a ₦9.22 trillion borrowing plan, with an exchange rate of ₦1,400/$1 and oil benchmarks of $75, $76.2, and $75.3 per barrel and daily oil production output of 2.06 million, 2.10 million and 2.35 million barrels for 2025 to 2027 respectively. Meanwhile, Nigeria returned to the international bond market after two years, issuing oversubscribed Eurobonds totalling $2.2 billion to finance the 2024 fiscal deficit. The issuance included $700 million in 6.5-year bonds at 9.625% and $1.5 billion in 10-year bonds at 10.375%, attracting over $9 billion in subscriptions.

A decade ago, many Nigerians believed that their country’s natural wealth, if shielded from corruption, could guarantee widespread prosperity. This conviction was rooted in the country’s vast resources — oil, gas, minerals, and a large, youthful population. However, the harsh realities of the present economic landscape have shattered this illusion, revealing a more profound crisis of mismanagement, inefficiency and unproductivity. Nigeria’s economy presents a stark paradox: a resource-rich country grappling with widespread poverty, inadequate infrastructure and a significant fiscal deficit. As is now usual with the MTEF, the assumptions it presents are divorced from reality. For a document meant to provide the long-term horizon for the country’s fiscal planning, it is hard to see how it provides a realistic framework for budgeting beyond meeting the legal requirements that it must be sent as a precursor to the budget. For context, the proposed ₦47.9 trillion expenditure for 2025, when converted using the Federal Government’s exchange rate of ₦1,400/$, amounts to $34.2 billion. This figure is alarmingly tiny for a country of Nigeria’s size and potential. To put it in perspective, Kenya — a nation with half the GDP and a quarter of Nigeria’s population — has proposed a budget of nearly the same size. This stark comparison highlights Nigeria’s fiscal inefficiencies and underscores the need for urgent reforms to diversify revenue sources, improve productivity and prioritise investments in critical sectors. Nigeria’s economic challenges are not merely a function of global factors but also the result of decades of policy missteps and over-reliance on oil revenue. Despite being one of Africa’s largest economies, the country has struggled to translate its resources into equitable development, widespread employment or sustainable infrastructure. While sometimes necessary, the dependence on borrowing to plug fiscal gaps underscores the urgent need for long-term solutions such as tax reform, industrialisation and digital transformation. On a more optimistic note, the recent success of Nigeria’s Eurobond issuance signals a potential turning point. Although the coupon rates are significantly higher than those of its West African neighbours — Benin Republic secured $750 million for 12 years at a 7.96% rate, while Côte d’Ivoire raised $2.6 billion with 9- and 13-year maturities at 6.3% and 6.85% respectively — the outcome reflects growing investor confidence in Nigeria’s economic reforms. The bond’s pricing — 9.625% for 6.5 years and 10.375% for 10 years — indicates that while borrowing costs remain high, the global financial community sees promise in Nigeria’s reform trajectory. Endorsements from the IMF and World Bank have undoubtedly played a role in bolstering this confidence. If these reforms are sustained and deepened, Nigeria could see a reduction in borrowing costs in the future, enabling the government to allocate more resources to critical sectors. However, relying solely on external debt is neither sustainable nor sufficient. The government must address systemic inefficiencies that drain public resources. For instance, reforming the tax system to ensure equitable contributions from all sectors and individuals is long overdue. Nigeria’s current tax-to-GDP ratio remains among the lowest globally, limiting the government’s capacity to invest in public goods and services. Expanding the tax base, combating tax evasion and simplifying tax compliance are essential to fiscal sustainability. In addition, boosting productivity across key sectors such as agriculture, manufacturing, and technology is crucial. Nigeria’s vast youth population remains a largely untapped resource. By investing in education, vocational training, and technology, the government can create an environment where innovation and entrepreneurship thrive. This, in turn, can reduce unemployment, improve living standards and increase the tax base. While the successful Eurobond issuance is a positive signal, it should not overshadow the urgency of addressing Nigeria’s structural economic weaknesses. Borrowed funds must be judiciously deployed to projects that deliver measurable impacts, such as energy infrastructure, transport systems and social services. The focus should be on creating a multiplier effect that stimulates economic growth and sustains revenue to service debts. In summary, Nigeria stands at a critical juncture. The reforms initiated are steps in the right direction, but their success depends on consistent implementation, transparent governance and a clear focus on improving the lives of ordinary Nigerians. As the country navigates its fiscal challenges, it must balance short-term measures like borrowing with long-term strategies to build a productive, inclusive, resilient economy.