Paper growth

Nigeria’s GDP grew by 3.46% in Q3 2024, up from 3.19% in Q2 and 2.54% in Q3 2023. The growth was mainly driven by the services sector…

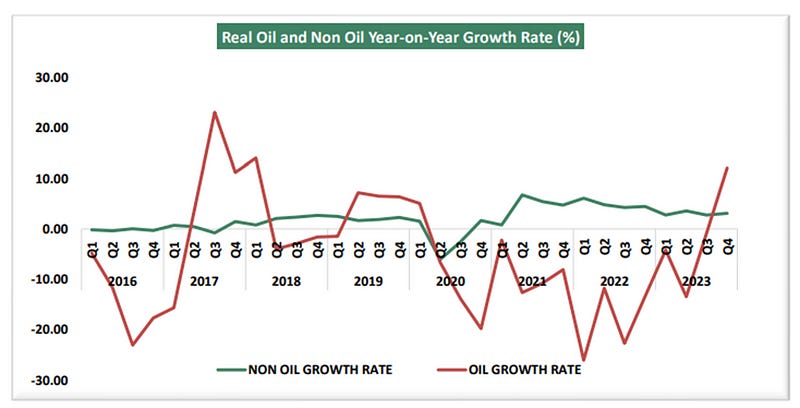

Nigeria’s GDP grew by 3.46% in Q3 2024, up from 3.19% in Q2 and 2.54% in Q3 2023. The growth was mainly driven by the services sector, which grew by 5.19% and contributed 53.58% to GDP. Oil production averaged 1.47 million barrels daily, with a real growth of 5.17%. The non-oil sector grew by 3.37%. Nigeria’s unemployment rate was 4.3% in Q2 2024. Meanwhile, the Central Bank of Nigeria raised its benchmark lending rate to 27.50%, marking its sixth hike this year, and reported foreign reserves at $40.88 billion as of 21 November 2024.

While headline GDP growth numbers exceeding projections are being celebrated — as seen in the presidency’s recent statements — the details tell a more troubling story. Key sectors like manufacturing, which should serve as engines of job creation and economic diversification, have contracted, reflecting a worrisome inability to catalyse industrial growth. Trade, another vital sector, remains stagnant, highlighting persistent structural issues and weak consumer purchasing power. Meanwhile, inflation continues its relentless climb, eroding disposable incomes and worsening living standards, even as the central bank persists with aggressive interest rate hikes. These measures, while aimed at curbing inflation, have inadvertently depressed the real sector, stifling investment and business expansion. The announcement of growing reserves has been portrayed as a success story. However, this improvement has yet to stabilise the naira, which continues its downward spiral, undermining confidence in the foreign exchange market. This disconnect between government pronouncements and real-world outcomes raises scepticism about the integrity and reliability of reported economic indicators. It is also crucial to contextualise Nigeria’s GDP growth in global and regional terms. While a GDP growth rate of 2–3% might seem reasonable for developed economies, it is insufficient for a developing country like Nigeria, which has a population growth rate of 2.42%. According to the United Nations, developing economies need a GDP growth rate of at least 6–7% annually to make meaningful progress in reducing poverty and improving living standards. Nigeria’s current growth trajectory falls woefully short of what is required to improve the citizens’ lives. The most concerning aspect of Nigeria’s recent GDP statistics is the stagnation in agriculture, the country’s largest employer and a cornerstone of food security. With over 70% of Nigerians relying on the agricultural sector directly or indirectly for their livelihoods, its stagnation represents a significant threat to economic stability and poverty reduction. Chronic challenges such as inadequate infrastructure, limited access to credit, climate change, and insecurity continue to plague the sector. Achieving the necessary 6–7% annual GDP growth will remain elusive unless these systemic issues are addressed.