Paradoxical

Six Nigerian banks' profit after tax rose 62.38% to $2.2 billion in 2024, despite economic challenges.

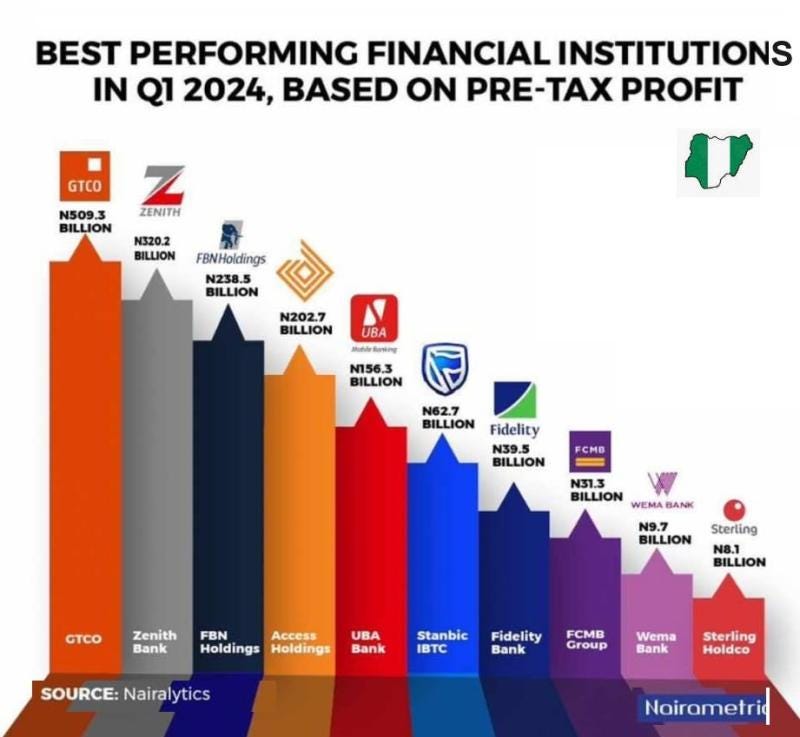

Six Nigerian banks reported a profit after tax of ₦3.41 trillion for 2024, a 62.38% increase from ₦2.1 trillion in 2023, despite challenges like customer dissatisfaction and economic difficulties. In related news, Nigeria's GDP grew by 3.84% in real terms in the fourth quarter of 2024, an improvement from 3.46% in Q4 2023. The expansion was attributed to the services sector, which saw a 5.37% growth, contributing 57.38% to the GDP. However, Nigerians took out ₦470 billion in personal loans in Q4 2024, with consumer credit outstanding rising 11.06% to ₦4.72 trillion by year-end, reflecting a growing reliance on personal loans amid prevailing economic conditions.

The stellar profit after-tax earnings of Fidelity, GTCo, Stanbic IBTC Holdings, United Bank for Africa, Wema and Zenith signal the continued dominance of financial institutions in an economy where households and businesses face mounting financial pressure. This surge in profitability, despite widespread economic difficulties and customer dissatisfaction, highlights the duality of Nigeria’s economic landscape: financial sector resilience coexisting with consumer hardship.

One key driver of this bank's profit growth is the impact of foreign exchange gains following the naira's depreciation. Many Nigerian banks hold substantial forex positions, allowing them to benefit from currency volatility. Additionally, higher interest rates, a feature of the Central Bank of Nigeria’s tightening monetary policy, have increased the cost of borrowing and boosted banks’ net interest income.

However, while banks thrive, ordinary Nigerians increasingly rely on personal loans, as evidenced by the ₦470 billion ($305 million) in new borrowing during the fourth quarter of 2024. The 11.06% rise in consumer credit outstanding to ₦4.72 trillion suggests that economic challenges—rising inflation, weak purchasing power, and job insecurity—are pushing individuals to borrow more to sustain their livelihoods. While providing short-term financial relief, this trend raises concerns about debt sustainability and potential defaults, especially if disposable incomes fail to keep pace with the rising cost of living.

Meanwhile, Nigeria’s GDP growth of 3.84% in the fourth quarter of 2024, driven mainly by the services sector, indicates some resilience in the broader economy. The services sector expanded by 5.37%, contributing 57.38% to GDP, with financial services, telecommunications, and trade playing key roles. However, an over-reliance on services-led growth appears to have reached its ceiling regarding job creation and inclusive economic expansion. For growth to translate into improved living standards, it must be accompanied by job creation, improved wages, and policies that alleviate household financial burdens.

Access to loans has historically been a limiting factor in Nigeria’s financial system, but the rise of fintech companies has made borrowing easier—though high interest rates remain a significant challenge. In developed economies, debt often stimulates consumer spending and economic growth. However, excessive dependence on credit can have adverse effects, particularly when financial stress leads to defaults and instability. This underscores the need for a more robust credit bureau system to enhance borrower assessment while exploring innovations such as universal credit scores.

In sum, Nigeria’s 2024 economic performance presents a paradox: record-breaking bank profits and GDP expansion, yet an alarming rise in consumer borrowing for basic needs. This imbalance highlights the urgency of policies that stabilise macroeconomic indicators while ensuring inclusive growth, reducing the financial strain on ordinary Nigerians.