Pile on

Nigeria’s total public debt portfolio now stands at about ₦48.93 trillion. The Debt Management Office (DMO) had earlier confirmed the…

Nigeria’s total public debt portfolio now stands at about ₦48.93 trillion. The Debt Management Office (DMO) had earlier confirmed the Nation’s Economic Intelligence report, which states that the government had raised ₦2.129 trillion in the first two months of 2023. A breakdown indicated that Nigeria’s domestic debts have risen to about ₦30.643 trillion, primarily due to new borrowings of about ₦1.599 trillion in the fourth quarter of 2022 and ₦2.129 trillion between January and February 2023. Nigeria’s external debt increased to ₦18.282 trillion, mainly due to the depreciation of the naira against the dollar.

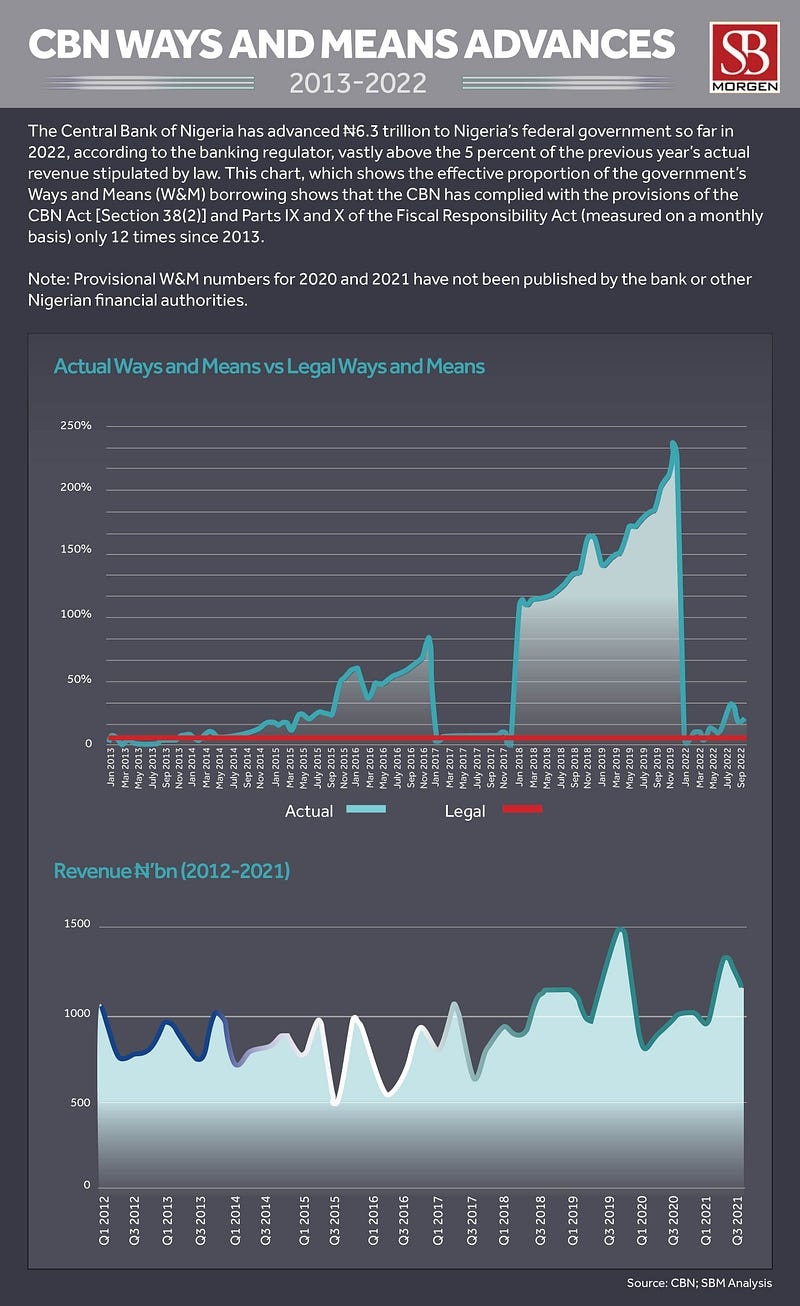

The public debt stock of Africa’s largest economy has been growing as debt sustainability indicators become concerning. The country’s debt-to-GDP ratio, estimated at 35.2 percent, is now over the 30% indicative benchmark by the government. The country’s debt service to revenue ratio, estimated at 80.7 percent, is way above World Bank’s suggested 22.5 percent for low-income countries. Another problem bubbling under the surface is the Ways and Means Advances made to the FG on behalf of the CBN. The National Assembly rebuffed President Muhammadu Buhari’s request to convert ₦24 trillion worth of temporary loans to the government from the central bank into 40-year bonds, a move that will shoot the public debt stock to about ₦73 trillion and negatively affect debt sustainability indicators. When Obasanjo handed over to a civilian administration in 1979, Nigeria’s public foreign debt stood at $3.74 billion. By 1983, the Shagari administration had driven the debt to roughly $20 billion. When Obasanjo returned as civilian president in 1999, he negotiated a partial write-off of Nigeria’s foreign debt to $19 billion, leaving Nigeria with a relatively clean slate to begin. But Nigeria’s total public debt portfolio now stands at ₦48.93 trillion after a borrowing spree by the Buhari administration, which has led to more debt in the last three years than in all the previous 30. Buhari alone is responsible for almost as much debt as all other post-1999 presidencies. Since the political carnival around the elections has sucked the air out of most conversations, stakeholders have to tackle one of Nigeria’s challenges — an inability to raise revenue and an unwillingness to make the hard decisions around spending cuts which has left the country hurtling towards a debt crisis. While President-elect Bola Tinubu is known to have a track record of boosting revenue collections in Lagos, much of these have come from personal income tax receipts from the formal sector. Pay As You Earn (PAYE) is a state-level tax whose corresponding federal equivalent, the company income tax, will be Tinubu’s new remit. Most of the firms that can provide quick wins for a Tinubu administration in this bracket already pay those taxes, and one does not know if he will be able to raise more taxes from this avenue. Value Added Tax collections might reach saturation point considering prevailing economic conditions; in the fourth quarter of 2022, the government collected ₦697.38 billion under this limb. In addition, Tinubu is also known for his ability to raise debt; he pioneered efforts by Nigeria’s subnational units to pursue their deficit financing strategies. It, however, remains to be seen how he will navigate debt at a national level considering the country’s current fiscal situation. Currency devaluation remains a risk item. Debt is not a bad thing. However, this administration has been profligate, with funds mostly channelled to non-revenue generating sources — recurring expenditure. Sorting through the morass is key for the new kids picking up the mantle. Considering the above, they have their work cut out.