Powering on credit

Ghana faces an imminent power crisis with under three days of fuel reserves. The government needs billions to pay for ordered fuel, considering private sector aid.

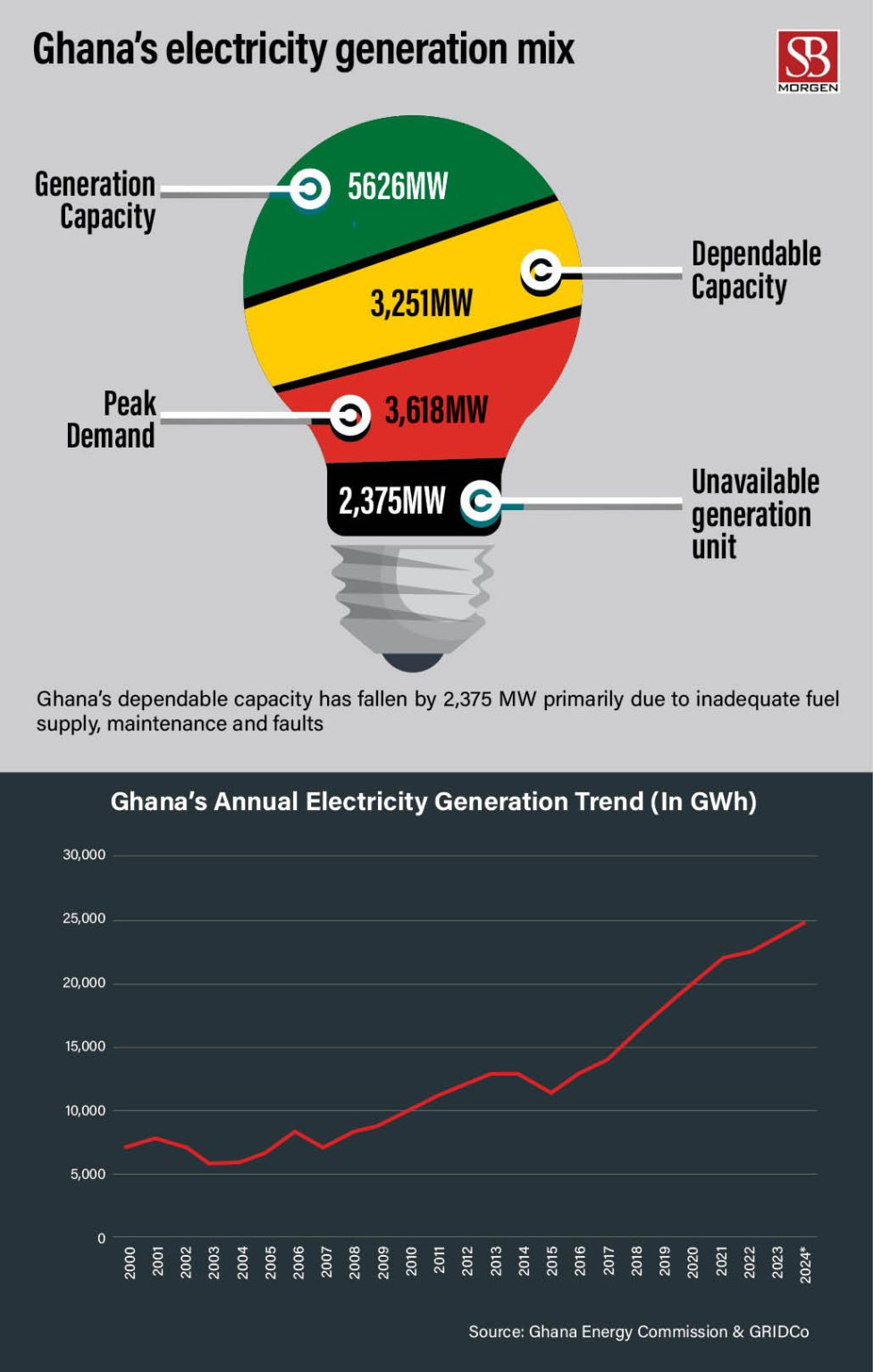

Ghana is on the brink of a nationwide power crisis, with less than three days’ worth of liquid fuel available to run its power plants, Energy Minister John Jinapor warned. The Ministry urgently needs billions of cedis to pay for already-ordered fuel, while financial constraints limit government action. Jinapor hinted at involving the private sector in managing the Electricity Company of Ghana (ECG) for a sustainable solution. Meanwhile, Ghana’s energy mix has shifted, with thermal now providing 70% of installed capacity. However, this transition has deepened financial strain, as the government owes Independent Power Producers (IPPs) over $2.5 billion.

Once heralded as a beacon of progress in Africa, Ghana now grapples with a severe economic crisis characterised by escalating public debt, rampant inflation, and currency depreciation. These profound challenges have triggered a cost-of-living crisis and widespread public unrest and severely constrained the government's capacity to deliver essential services, most notably within the energy sector. Following its external debt default in 2022, Ghana embarked on a complex restructuring process with international bondholders. This default, a direct consequence of unsustainable debt servicing costs and broader macroeconomic instability, has had far-reaching implications, particularly undermining the state's ability to invest in power infrastructure and secure vital fuel supplies.

Despite boasting an impressive electricity access rate of nearly 90%—one of the highest in West Africa—this achievement comes at a significant fiscal cost. Though relatively stable, the nation's power supply predominantly relies on thermal plants, which are heavily dependent on consistent and substantial funding for natural gas and liquid fuels, estimated at approximately $90 million monthly. However, Ghana's reliance on gas imports, particularly from Nigeria via the West African Gas Pipeline, has proven problematic due to intermittent supply disruptions. Meanwhile, burgeoning demographic pressures, including population growth and increasing rural-urban migration, continue to drive up electricity demand, making it increasingly difficult to meet. This mounting strain on the sector has been highlighted in reports such as SBM Intel's "Ghana's looming energy crisis" from April 2024, underscoring the severity of the financial challenges.

The energy sector remains a major contributor to Ghana's public debt, with government shortfalls in power sector payments estimated at around $2 billion annually. This fiscal stress, exacerbated during and after the 2022 economic crisis, has frequently led to erratic electricity provision. Central to this dilemma is the state-owned Electricity Company of Ghana (ECG), which operates with a commercial loss rate of approximately 32% and carries a staggering debt exceeding $5 billion. Repeated government defaults have stalled efforts to restructure the sector's debt, despite ongoing discussions and support from entities like the World Bank; alarmingly, reform efforts are being outpaced by new debt accumulation.

In response to these pervasive issues, President John Mahama has advocated for the partial privatisation of ECG, a strategy aimed at curbing inefficiencies, reducing financial losses, and alleviating the state's growing fiscal burden. Simultaneously, there is a concerted push to increase the share of renewable energy in Ghana's power mix, targeting an ambitious shift from the current 2% to 10% in the medium term. Achieving this will require significant capital investment and present a crucial opportunity for private sector engagement. Ghana's power sector is thus at a critical juncture, navigating the complex interplay of fiscal strain, policy inertia, and entrenched structural inefficiencies. While access levels remain commendable, the sustainability of supply is undeniably under threat, underscoring the urgent need for bold reforms, improved debt management, and renewed investment, particularly in cleaner, more resilient energy sources.