Rebasing the illusion?

Nigeria’s GDP rebasing to 2019 shows a sharp rise to ₦372.82 trillion ($243.76 billion), with Q1 2025 growth at 3.13%, led by services (4.33%).

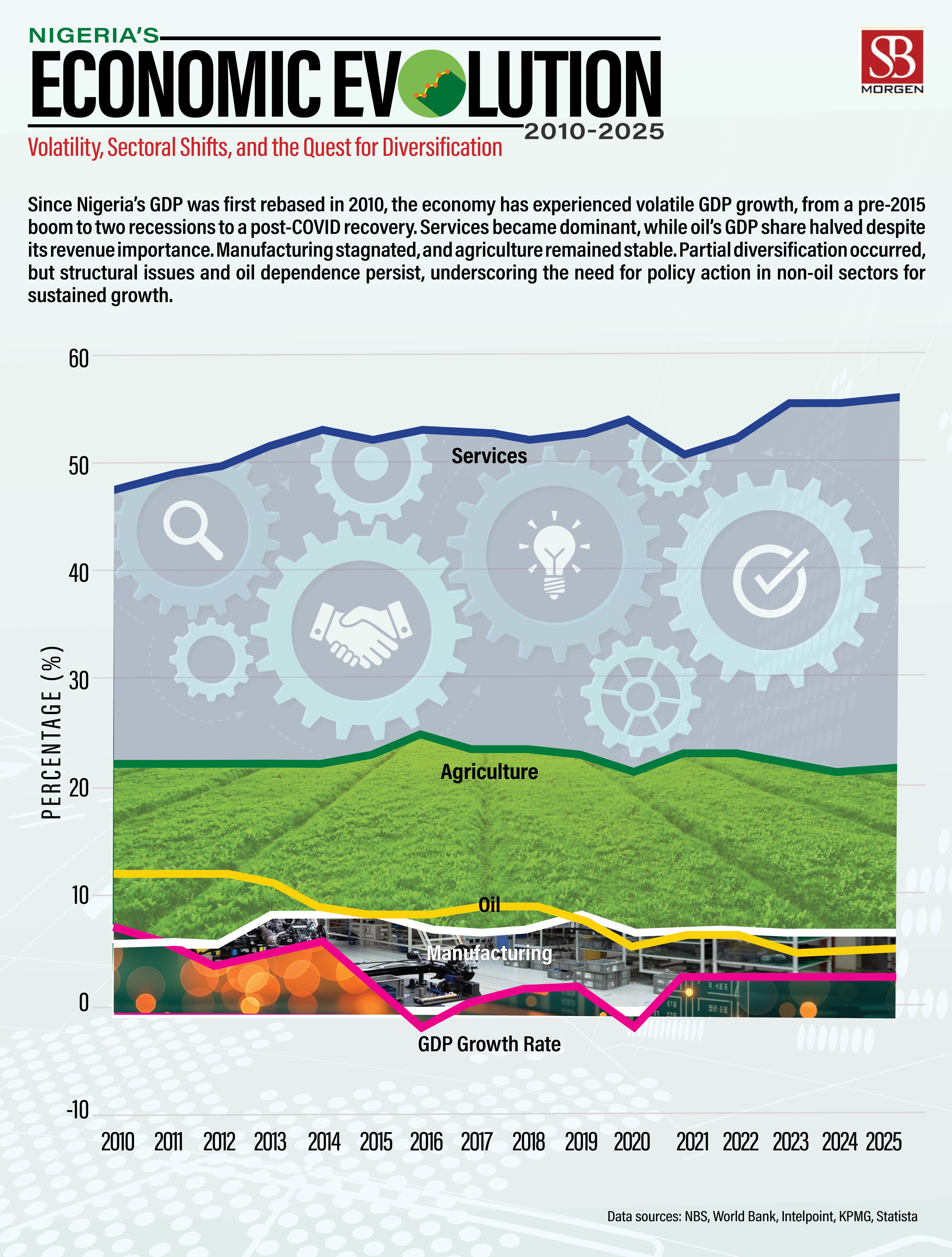

Nigeria’s GDP has been significantly revised following a rebasing exercise that changed the base year from 2010 to 2019. The rebased nominal GDP for 2024 is ₦372.82 trillion ($243.76 billion), up from ₦205.09 trillion ($134.09 billion) in 2019. In Q1 2025, the economy grew by 3.13% year-on-year in real terms, led by the Services sector, which expanded by 4.33% and contributed 57.50% to GDP. The industrial sector grew by 3.42%, while the agricultural sector recorded marginal growth of 0.07%. The non-oil sector dominated, contributing 96.03% to GDP. Q1 2025 nominal GDP stood at ₦94.05 trillion, reflecting sustained economic expansion.

The recent rebasing of Nigeria’s Gross Domestic Product (GDP), shifting the base year from 2010 to 2019, represents a significant recalibration of how the economy is measured. The updated nominal GDP figure for 2024 is ₦372.82 trillion ($243.76 billion), showing a marked statistical increase from the pre-rebasing estimate of ₦205.09 trillion ($134.09 billion) in 2019. While rebasing does not reflect new economic output, it offers a more accurate representation by incorporating emerging industries and structural shifts across sectors.

First-quarter 2025 data provides further insight into Nigeria’s evolving economic landscape. Real year-on-year growth of 3.13% suggests moderate, sustained momentum despite persistent macroeconomic pressures. Services continue to drive expansion, growing by 4.33% and contributing 57.50% to GDP, likely supported by resilient sub-sectors such as ICT, finance, and trade. Due to ongoing infrastructure and energy deficits, the industrial sector's 3.42% growth is notable. In contrast, agriculture recorded a marginal 0.07% increase, reflecting unresolved issues around productivity, climate vulnerability, and input supply chains. These underscore the need for targeted reforms in agribusiness and rural value chains, particularly concerning the country’s food security concerns.

The dominance of the non-oil sector, contributing 96.03% to GDP, points to progress in output diversification. However, this must not be mistaken for fiscal diversification. Government revenue remains heavily dependent on oil, even as the sector’s contribution to GDP has fallen to just 3.97%. Its influence on foreign exchange inflows and budgetary performance remains disproportionately large.

The rebased GDP offers a more accurate denominator for macro indicators such as the debt-to-GDP ratio, which may now appear improved. Nonetheless, this statistical uplift does not address Nigeria’s fundamental structural deficiencies: low revenue mobilisation, elevated inflation, a narrow export base, and high unemployment. Rebasing is a methodological refinement—not an economic remedy. The challenge lies in translating nominal gains into tangible outcomes. Improved infrastructure, higher living standards, and credible fiscal consolidation must follow. Absent this, the rebased figures risk becoming an accounting milestone with limited real-world impact.

This is Nigeria’s first GDP rebasing in 11 years, despite international best practice recommending a five-year interval, with a maximum of ten. While GDP has expanded in Naira terms, the drastic decline in exchange rates in 2023-2024 means the gains have not translated into improvements in US dollar terms or per capita GDP—both of which remain at historic lows, effectively returning Nigeria to 2007 levels in dollar terms for key sectors. Critically, industry’s share of the shrinking GDP has declined even as industrialisation remains essential to sustaining long-term growth. This signals a failure of industrial policy and a chronic shortfall in infrastructure investment. President Tinubu’s pledge to achieve a $1 trillion economy by the end of his term would require GDP to quadruple over six years—three of which will likely be consumed by second-term dynamics and succession politics. Even for the most optimistic observers, this target borders on the implausible.