Slippery slope

Ghana's plan to transfer 80% of MIIF to Consolidated Fund raises concerns over long-term financial stability.

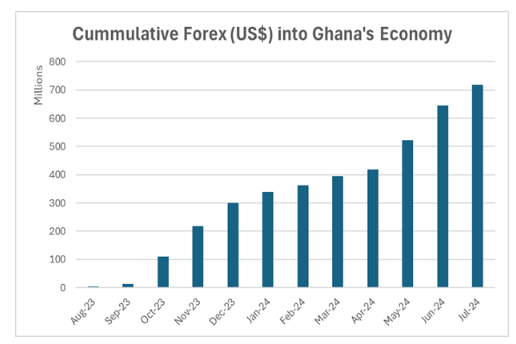

Ghana’s plan to transfer 80% of the Minerals Income Investment Fund (MIIF) into the Consolidated Fund for infrastructure has raised concerns among analysts, who warn it could weaken long-term financial stability. MIIF, a top-performing state entity, grew from $180 million in 2021 to nearly $1 billion in 2024. Meanwhile, the Ghanaian cedi depreciated 1.57% against the US dollar last week, with year-to-date losses at 2.66%. The slump follows tax cut announcements in the 2025 budget, raising concerns over fiscal targets. Investors reacted negatively, with Ghana’s dollar bonds falling 1.5 cents, signalling potential fiscal instability.

When a government decides to scrap well-functioning tax handles generating $700 million annually to fulfil a campaign promise, it often leads to alternative measures, such as reallocating 80% of mineral royalties—previously managed by the Minerals Income Investment Fund (MIIF)—to the Consolidated Account. These funds are expected to be directed toward infrastructure projects and social programmes like free tuition for first-year students in public tertiary institutions and free sanitary pads for young girls. Ghana's mineral royalties amount to approximately $400 million annually, with a significant portion originally designated for MIIF investments. MIIF typically allocates over 70% of its income to high-yield assets, ensuring long-term financial growth. However, projections indicate that Ghana could forgo nearly $10 billion in sovereign wealth fund accumulation over the next 15 years if this new policy is implemented.

The move thus raises concerns about the effectiveness of the previous government’s policies, which, despite their flaws, established mechanisms like the MIIF to create sustainable revenue streams and build long-term financial resilience. The MIIF’s focus on high-yield investments was designed to generate wealth for future generations, aligning with global best practices for resource-rich nations. While the previous administration faced criticism for inefficiencies and slow implementation, its framework for managing mineral royalties provided a foundation for economic stability. A complete reversal of these policies risks undermining this progress, potentially destabilising Ghana’s fiscal outlook.

The dangers of a 180-degree turn by the new government are evident. While redirecting funds to immediate social and infrastructure needs may address short-term demands, it could come at the expense of long-term economic security. The projected $10 billion loss in sovereign wealth accumulation over 15 years highlights the trade-offs. Moreover, such abrupt policy shifts can erode investor confidence, particularly in a volatile economic environment.

Meanwhile, the Ghanaian cedi remains under pressure against the U.S. dollar. The situation has been worsened by the central government's decision to lower treasury bill rates from 28% to 17%, making the domestic market less attractive to investors. As a result, many are shifting their investments to alternative assets like the dollar, further weakening the cedi. Large capital transfers by multinational corporations have also exacerbated the currency's depreciation.

In this context, the new government must tread carefully. While addressing immediate social needs is crucial, it should avoid dismantling systems contributing to long-term economic stability. A balanced approach—one that preserves the strengths of previous policies while introducing targeted reforms—would be more effective. Abrupt reversals risk economic instability and a loss of credibility among investors and international partners. Policymakers must prioritise continuity, transparency, and stakeholder engagement to ensure that Ghana’s economic trajectory remains sustainable.