Stained black star

Ghana’s balance of payments further deteriorated to a deficit of $3.64 billion in December from a $3.4 billion deficit the previous…

Ghana’s balance of payments further deteriorated to a deficit of $3.64 billion in December from a $3.4 billion deficit the previous quarter, central bank data showed on Saturday. Recent balance of payments woes have been largely driven by a sharp reversal in capital flows, with Ghana’s capital account deficit worsening to $2.18 billion in December from $1.64 billion in September. At the same time last year, Ghana had a capital account surplus of more than $3.3 billion.

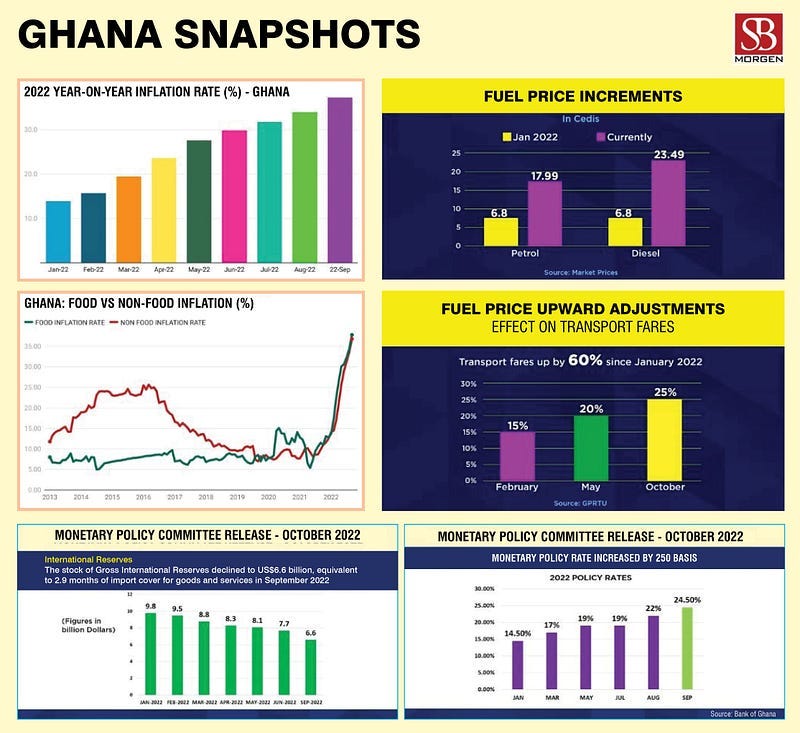

At the end of the 2022 fiscal year, Ghana’s current account deficit, together with its net capital and financial account outflow, resulted in an overall balance of payments deficit of US$3.6 billion, compared to a surplus of US$510.1 million in 2021; the stock of gross international reserves stood at US$6.2 billion (equivalent to 2.7 months of import cover) from a stock position of US$9.7 billion (equivalent to 4.4 months of import cover) at the end of December 2021. The net international reserve position stood at US$2.4 billion, from US$6.1 billion over a comparative period. The state of the global economy in 2022 impacted the external sector’s performance. The improvement in the merchandise trade account significantly reduced the current account deficit from 3.2% of GDP in 2021 to 2.3% of GDP the following year. However, these gains were offset by sizable net capital and financial account outflows, mostly because of external factors that led to portfolio reversals and a decline in foreign direct investments, which led to a general balance of payments deficit and a reduction in reserves. Africa’s Black Star continues to depend heavily on inflows from the commodity. Still, in 2022, Ghana’s key export commodities prices, such as gold, cocoa and crude oil, remained volatile on the global markets. For instance, cocoa futures traded largely in the negative during most parts of 2022. Prices peaked at US$2,681.11 per tonne in February on the back of lower production volumes and, after that, eased to a low of US$2,333.33 per tonne in July 2022, owing to weak grind data. Gold prices rose to historical highs of US$1,949.4 per ounce in March as a result of increased global uncertainties but then dropped as a result of rising interest rates and a stronger US currency to finish the year at US$1,796.2 per ounce, an 8.7% increase over the previous year. The cost of all imports into the country rose 7.0% in 2022 to US$14.65 billion due to increasing expenditures for oil and gas imports. Oil and gas imports, consisting primarily of refined petroleum, increased annually by 71.3%, from US$2.7 billion in 2021 to US$4.7 billion in 2018, predominantly due to increased pricing. Nevertheless, the steep depreciation in the currency rate caused non-oil imports to contract by 8.4% to US$10.0 billion, mostly due to imports of capital and consumer items. Last year saw significant pressure on Ghana’s local currency due to portfolio reversals, a decline in foreign direct investment inflows, and rising demand pressures. The Ghana cedi lost more than 30.0% of its value versus the US dollar in the year under review (4.1% in 2021), despite some losses being reversed at the dying embers of the year. Just like last year, the cumulative depreciation of the Ghana cedi for January 2023 was 19.5%. The IMF bailout may be needed sooner than later. While the government waits to obtain the green light for an IMF programme, it has already taken several steps, including the gold-for-oil policy, to bring Accra’s balance of payment back to surplus status. According to the country’s Vice President, the policy is meant to tackle dwindling foreign currency reserves and the demand for dollars by oil importers, weakening the currency and increasing living costs. It was inevitable that capital flows would reverse as investors found ways to get their monies out or stop their money from going into Ghana. The Ghanaian government’s initial unilateral pronouncements on debt restructuring did much to damage trust, and the long-term effects are only beginning to emerge. This is a classic example of making a bad situation worse. Policymakers must weigh their actions and consider the systemic impact of such actions.