Tear gas for beans not chocolate bars

Ivorian cocoa farmers protest unpaid stocks as prices crash. Police fire tear gas amid demands for an industry audit.

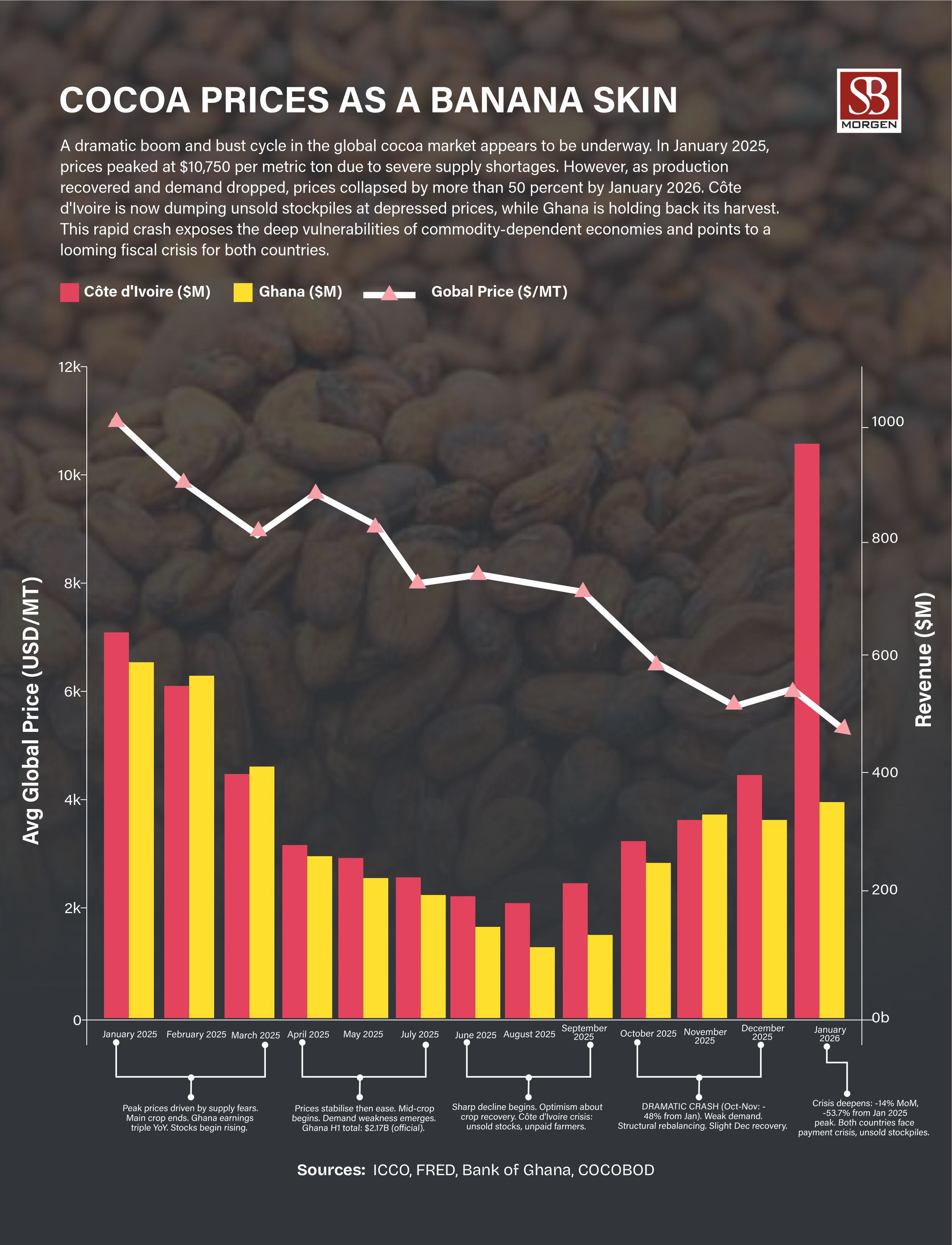

Côte d’Ivoire is facing growing unrest in its cocoa sector as farmers protest unpaid cocoa stocks and falling prices that have left many struggling financially. In M’Batto, police used tear gas to disperse demonstrators demanding payment for cocoa sold during the October-to-March harvest season, with farmers warning that delayed payments could affect the next harvest and their livelihoods. The crisis follows a sharp drop in global cocoa prices below government-fixed rates, leaving large volumes unsold. Meanwhile, civil society group PEC-CI is demanding an audit of the Coffee-Cocoa Council after cocoa prices reportedly fell by 57%, arguing that weak price stabilisation policies and poor transparency continue to expose farmers to severe economic hardship.

The unrest spreading across M’Batto, Daloa, and Duekoué is not an isolated labour dispute in Côte d’Ivoire’s cocoa belt. It is the clearest signal yet that the country’s cocoa‑dependent economy is entering a period of structural strain. Cocoa contributes roughly 40 percent of export earnings and supports nearly one million farming households. The collapse in farmgate prices from 2,800 to 1,200 CFA francs per kilogramme therefore represents far more than a commodity correction. It exposes the fragility of a pricing system that has historically underpinned both fiscal stability and social cohesion in the world’s largest cocoa producer.

At the heart of the crisis lies the pricing framework operated by the Coffee‑Cocoa Council (CCC). Under the forward‑selling mechanism introduced after the 2011 reforms, between 70 and 80 percent of expected harvest volumes are pre‑sold to international traders. This allows authorities to fix a guaranteed farmgate price based on projected market conditions, shielding farmers from intra‑season volatility. However, the model has become vulnerable to market miscalculations. The 2025/26 season exposed this vulnerability with unusual severity. In October 2025, the CCC fixed the main‑crop farmgate price at a record 2,800 CFA francs, assuming the extraordinary cocoa rally of 2024 would persist. Instead, global cocoa futures collapsed as chocolate manufacturers reduced volumes amid weaker demand and high prices. The result was a severe mismatch: by December, Ivorian cocoa was trading at nearly 75 percent above world prices, effectively freezing exporter purchases and leaving 100,000–200,000 tonnes unsold.

The subsequent reduction of the farmgate price to 1,200 CFA francs in March 2026 was an unavoidable market correction, but its social consequences were devastating. Farmers who had already delivered produce under the earlier pricing structure faced losses exceeding 50 percent. Delayed payments for deliveries between October and March exposed a deeper liquidity crisis. The unrest now emerging reflects not only falling incomes but also growing distrust in the institutions responsible for stabilising the sector. This is where the issue becomes politically and fiscally sensitive. The CCC maintains a stabilisation reserve fund with the Central Bank of West African States and parallel reserves in Ivorian commercial banks – mechanisms designed to absorb such shocks. Yet the apparent inability or unwillingness to deploy these reserves transparently has intensified civil society calls for an independent audit. The reluctance to commission such an audit has itself become a source of suspicion, especially given memories of the near‑identical 2017 crisis, when up to 80 percent of forward buyers defaulted on contracts.

We argue that the CCC should be audited and its findings published, covering stock levels, sales, payment flows, buyers’ obligations, and any losses. This should not be a narrow financial exercise but a compliance audit that checks whether rules, procedures, and payment systems are actually working. The problem is not just underpayment; delayed payments and weak oversight turn a pricing dispute into a legitimacy crisis for the entire cocoa value chain.

The broader macroeconomic implications are increasingly difficult to ignore. Côte d’Ivoire has maintained one of West Africa’s strongest macroeconomic profiles – growth around 6 percent, moderating inflation, and a narrowing fiscal deficit. But the cocoa sector now represents a concentrated downside risk. The government has already committed about 280 billion CFA francs to purchasing unsold stocks while simultaneously subsidising the gap between guaranteed farmgate prices and lower export prices. This forces the state into an expensive balancing act between preserving farmer incomes, maintaining social stability, and protecting fiscal consolidation targets.

More importantly, the crisis signals that the era of easy cocoa windfalls may be ending. Côte d’Ivoire and Ghana historically benefited from their combined dominance of global supply (55–60 percent of world output), giving them significant pricing leverage. However, structural shifts are weakening that position. New competition from producers such as Ecuador, Nigeria, and Cameroon is gradually eroding the traditional West African duopoly. Increasingly stringent regulations, such as the EU Deforestation Regulation, add new compliance costs.

This is as much a transparency and bargaining‑power problem as a market problem. Pricing should be more transparent so farmers can see the same information on global prices, exchange rates, export contracts, and regulatory assumptions simultaneously. Farmers need stronger bargaining power through cooperatives, better access to finance, and direct representation in pricing discussions. Accountability works only when information is shared openly, farmers have a voice, and there are real regulatory penalties for manipulation.

The currency dimension further complicates the outlook. Because Côte d’Ivoire and Ghana operate within relatively stronger currency frameworks than some regional competitors, their cocoa exports risk becoming structurally more expensive. If Nigeria significantly expands cocoa production while maintaining a weaker exchange rate, it could gradually develop a competitive export advantage. Though such a shift is unlikely in the immediate term due to infrastructure and productivity constraints, the directional risk is becoming more apparent.

Ultimately, the crisis is not simply about cocoa prices; it is about the sustainability of the institutional model governing the sector. The forward‑selling framework worked during periods of chronic global undersupply, but it has now produced two major pro‑cyclical crises within a decade. A more resilient structure would likely require shorter forward‑sale windows, greater transparency around stabilisation reserves, independently supervised reserve management, and a pricing mechanism more dynamically linked to international futures markets rather than politically determined annual benchmarks.

None of these reforms is technically impossible, but the real challenge is institutional and political. If the sector is to rebuild trust, greater transparency is unavoidable, even if it reduces the CCC’s discretionary power. Without reform, the cocoa sector risks becoming not a pillar of stability but a recurring source of payment delays, weak accountability, and farmer unrest.

For investors and policymakers alike, the message is increasingly clear: Côte d’Ivoire’s macroeconomic resilience can no longer be assessed in isolation from the structural weaknesses emerging in its cocoa economy. The credibility of the government’s response over the coming quarters may determine whether the country preserves its reputation as one of Africa’s strongest frontier growth stories or enters a more prolonged cycle of commodity‑driven instability.