The borrowing continues

President Bola Tinubu has requested $2.209 billion in external borrowing to cover Nigeria’s 2024 budget deficit, citing sections 21(1) and…

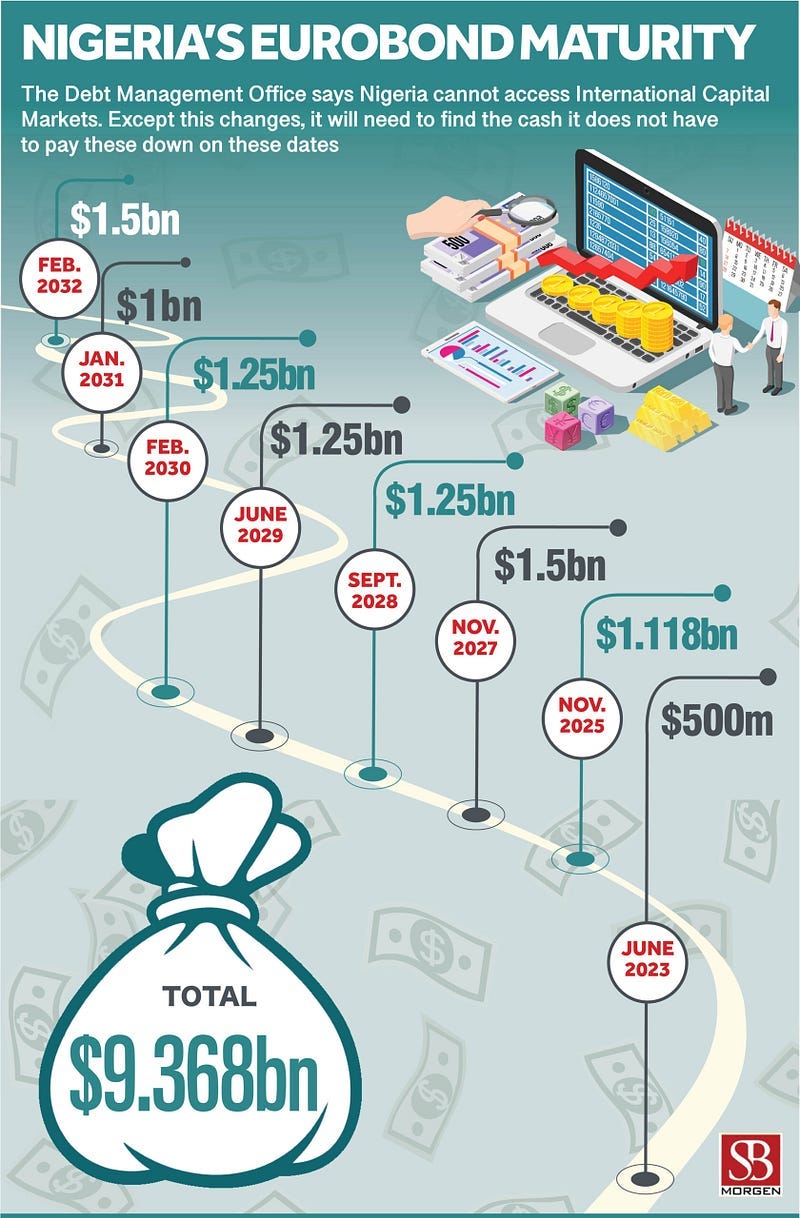

President Bola Tinubu has requested $2.209 billion in external borrowing to cover Nigeria’s 2024 budget deficit, citing sections 21(1) and 27(1) of the Debt Management Office Act. This request comes as the 2024 budget expires on 31 December. Additionally, Tinubu has transmitted the 2025–2027 Medium Term Expenditure Framework (MTEF) and Fiscal Strategy Paper (FSP) to the National Assembly. The MTEF includes a crude oil benchmark of $75 per barrel, a production target of 2.06 million barrels per day, an exchange rate of ₦1,400 per dollar, and a projected GDP growth rate of 6.4%.

The government’s proposed borrowing source remains ambiguous, particularly as it involves foreign currency. Critical questions remain unanswered: Will the funds be secured through another multilateral loan arrangement, or will the government opt for an alternative such as issuing a bond? Recently, the success of the local USD-denominated bond issuance has sparked discussions about targeting Nigerians in the diaspora for a similar initiative. Although initiative in approach, this diaspora bond raises challenges, including the logistics of issuance and whether it can generate sufficient interest among the target audience. Regardless of the chosen mechanism, what remains evident is the continuity in fiscal strategy from the previous administration. It appears the Tinubu-led government is following the same path as the Buhari administration, which relied heavily on massive deficit financing without a corresponding boost in economic productivity. Under Mr Buhari, Nigeria saw a surge in debt accumulation, much of it justified by the need to address infrastructure deficits and support social investment programmes. However, these investments often failed to translate into tangible, sustainable economic growth or improved revenue streams. The current administration seems to be perpetuating this cycle. While borrowing is not inherently bad — many governments worldwide rely on debt to fund development — it becomes problematic when the funds are not directed towards projects or initiatives that drive long-term growth. Nigeria’s persistent challenge has been its inability to significantly increase productivity, diversify revenue streams, and create an environment conducive to economic expansion. This lack of productivity improvement exacerbates the country’s debt burden, as the borrowed funds do not generate the returns needed to repay the loans or justify the interest obligations. The reliance on foreign currency-denominated loans or bonds introduces additional risks, particularly currency risk. A weakening naira could make debt servicing more expensive, further straining the country’s precarious fiscal position. This risk underscores the need for a more deliberate and transparent borrowing strategy, prioritising projects with measurable economic benefits. If the government continues to borrow without addressing structural issues such as low productivity, limited industrialisation, and inadequate export diversification, Nigeria risks falling into a debt trap. The economic playbook needs an urgent rewrite. Rather than simply replicating past strategies, there must be a shift towards policies prioritising fiscal discipline, economic diversification, and efficiency in public spending. Without these changes, the current approach will likely deepen Nigeria’s economic vulnerabilities, leaving the country on an unsustainable fiscal path.