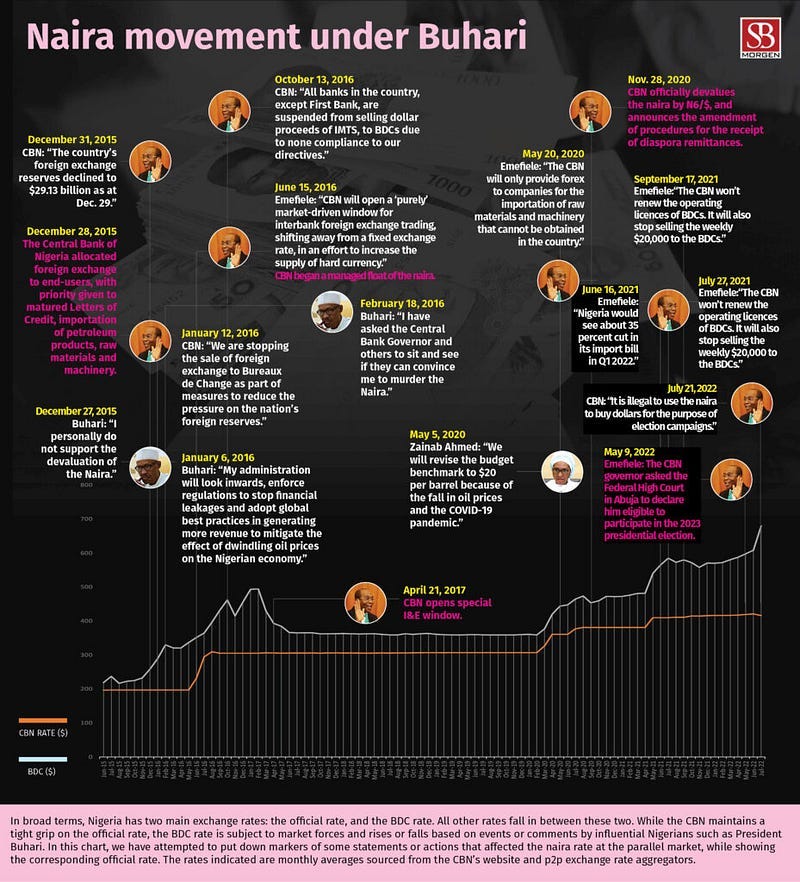

The CBN’s dilemma

The Economic Intelligence Unit (EIU) has predicted in its latest report that it believes the Nigerian government will go back to a system…

The Economic Intelligence Unit (EIU) has predicted in its latest report that it believes the Nigerian government will go back to a system with more control over the exchange rate to try and stop the Naira from losing its value much further. The EIU pointed out that the Central Bank of Nigeria (CBN) needs more experience handling a flexible exchange rate system, and the need to control rapidly increasing inflation will become more acute over time. Meanwhile, on 31 August, President Bola Tinubu announced that Nigeria has been able to save over ₦1 trillion by removing petrol subsidies.

Firstly, the reality is that almost no currency in existence is solely floating or fixed. Most central banks intervene in the exchange rate mechanism whenever they deem necessary. In Nigeria’s case, the CBN’s ability to intervene is constrained by the level of foreign exchange reserves. In recent years, $40 billion appears to be a benchmark that indicates how bullish the CBN’s intervention can be. Nigeria’s external reserves opened the year at about $37 billion but had dropped to about $34 billion as of July 2023. Many analysts suggest that the CBN is currently constrained in its ability to defend the Naira, hence the reason why the Naira has devalued in the official window in recent weeks. However, with the removal of petrol subsidies and the end of the high FX demand season of July–September, there is an increased likelihood that the downward slide in the foreign reserves will change how the Naira could strengthen against the US Dollar towards the end of the year. Secondly, moving towards a fixed exchange rate system could be economically disadvantageous for Nigeria, especially considering the significant amount the Central Bank has spent in the past to maintain such a system. The fixed exchange rate restricts the Naira’s flexibility to adjust to market fluctuations and economic changes, which may hinder the country’s ability to respond effectively to external shocks. The continuous intervention required to defend the fixed rate could deplete the Central Bank’s foreign currency reserves and take away resources that could be used for other critical developmental purposes, such as infrastructure improvements or social programmes. On Mr Tinubu’s claim that the government saved ₦1 trillion from the removal of subsidies, there is only one thing to say — it is a deceptive narrative. The true context is this: since 2017, the NNPC has withheld monies that should have gone into the pork barrel for sharing by the three tiers of government for subsidies and other sundry expenses. Unchecked by anyone, including the National Assembly, the company even took out of the government’s oil tax proceeds and dividends from the Nigeria Liquified Natural Gas Company to run two parallel subsidies or “under-recovery” schemes. When Nigeria’s oil proceeds dropped, the state-owned oil company found it hard to raise enough money to fulfil financial commitments on the fields it has licences in, absorb losses from underselling petrol and kerosene and still add some pork to the less-than-half-full barrel. In response to the shortfall and the unprofitability of the NNPC to its money-earning course, the government borrowed from the central bank, the domestic market, and foreign bilateral and multilateral lenders. Much of the borrowings contravened section 12 of the Fiscal Responsibility Act, which asks the government not to borrow for things that would not yield income. By the last full year of the Buhari administration, the government had borrowed so much, and the cost of borrowing was very expensive, so the government put a stop to the ability of the NNPC to withhold money in the name of subsidy. That full stop was a ₦3.36 trillion budget that should cover for under-recoveries for six months in 2023. In its last Medium Term Expenditure Framework and Fiscal Strategy paper, the government said that if it did not take that action, the 2023 budget would not contain capital expenditure for its Ministries, Departments and Agencies. The only money the finance ministry reasoned the government would have, if the subsidy were not removed, would be those tied to grants — ₦1.7+ trillion. That weighs less than the expected half-year subsidy withholding by the NNPC. The government cannot treat the absence of a subsidy as part of its savings because it collects less than enough from its income sources, even without the subsidy. Food for thought: the NNPC currently owes the oil marketers it has been swapping petrol with roughly $3 billion, and it is expected to finish clearing the debt by October. For context, NNPC says it earned profit after tax of ₦674 billion ($1.6 billion) based on a ₦410 rate from the approved budget exchange rate in 2021. We, therefore, wonder whether Tinubu’s much-touted savings brag is as substantial as it might have been given a bit more accountability and transparency.