The chips are down

The International Monetary Fund (IMF) downgraded Nigeria’s 2024 economic growth forecast to 2.9%, citing insecurity in oil-producing areas…

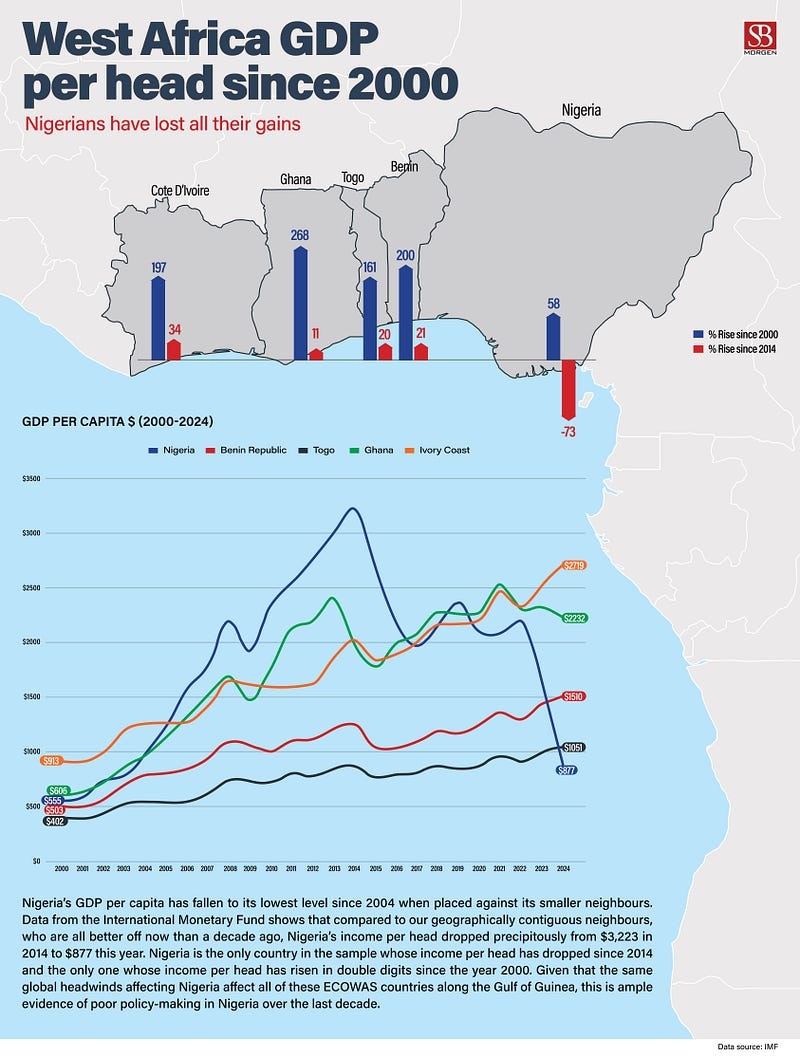

The International Monetary Fund (IMF) downgraded Nigeria’s 2024 economic growth forecast to 2.9%, citing insecurity in oil-producing areas, flooding, and lower-than-expected activity in the year’s first half. This marks a reduction from earlier projections of 3.3% in April and 3.1% in July. Nigeria’s GDP per capita dropped to $877, lagging behind neighbouring countries like Benin, Togo, Ghana, and Ivory Coast. Floods, attributed to poor infrastructure, killed 185 people and displaced 208,000 across 28 states. Additionally, unrest in the Niger Delta region has affected oil production, the country’s primary source of revenue.

Nigeria’s GDP per capita halved in one year, falling to its lowest since 2004. Earlier in the year, there were expectations that the country would begin to see gains from fiscal reforms, leading the lender to forecast an improved economy. But reality has hit, and the IMF’s projection indicates a decline from 3.1 percent in July and 3.3 percent in April. Nigeria, which ranked Africa’s largest economy in 2022, has slipped to fourth place. This decline is largely due to a precipitous devaluation of the currency against the USD, the currency used to denominate the GDP per capita measure — the exchange rate fell from around ₦700 to over ₦1,700 per dollar. Compared to its immediate neighbours, Nigeria has fared poorly, with this decline beginning in 2014 (when per capita GDP was at its highest in the country’s history at $3,201) after 16 years of steady growth during the Peoples Democratic Party years, when it rose from $494 in 1999. This is a good proxy to measure the impact of APC’s administration, and the verdict is clear: it has been a time of thorough destruction of wealth for the country. After two naira devaluations in eight months, the currency has become more than 70% weaker against the dollar, fuelling inflation at record highs. While Nigeria is expected to see a decline in growth, its African peers, such as Ghana, Angola, Côte d’Ivoire, Cameroon, and South Africa, are projected to improve. These countries are intensifying efforts to drive consumption and economic growth. As Nigeria continues to experience slow growth, more people are becoming impoverished. Recently, the World Bank said that an additional 25 million people have been pushed into poverty in just six months. Another report from the IMF indicated that Nigeria’s GDP per capita has dropped by 46 percent to $877 as of October 2024. This illustrates that the average Nigerian is now poorer than 20 years ago. Nigeria’s biggest economic challenge is weak productivity. This means the majority of its working-age citizens are not sufficiently engaged to produce outputs that can be bought and sold to create value. Each individual’s productivity contributes to the country’s GDP, and with GDP per capita at $877, it suggests that the productivity of the average Nigerian is among the lowest in the world. This is surprising because Nigerians are well known for their entrepreneurial spirit and strong work ethic. This implies that many Nigerians lack opportunity and direction, which the government should provide. The conflicts and insecurity in various parts of the country have led to internal displacement, causing much of Nigeria’s predominantly farming population to become disengaged.