The miners have had too much stability

Ghana plans sweeping mining reforms, scrapping long-term stability agreements and significantly raising royalty rates to capture more value from high gold prices.

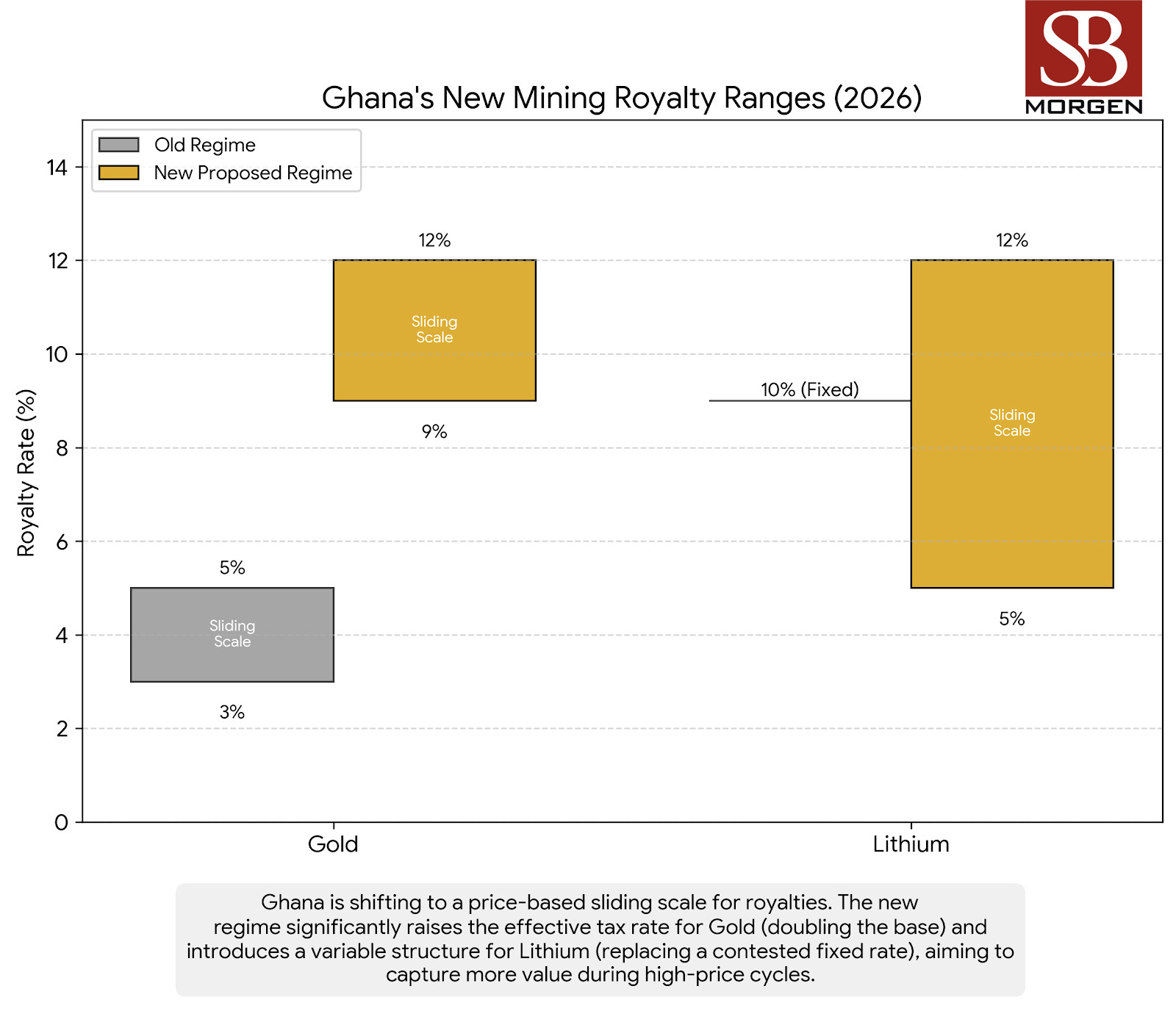

Ghana will scrap long-term mining investment stability agreements and sharply raise royalties under sweeping reforms aimed at capturing more value from record gold prices, the country’s minerals regulator has said. Isaac Tandoh, acting chief executive of the Minerals Commission, told Reuters the changes seek to balance investor confidence with the government’s push for higher mining revenues. A draft bill expected in parliament by March proposes royalties starting at 9% and rising to 12% if gold prices reach $4,500 per ounce or higher, roughly double current rates. Stability agreements, which lock in tax and royalty terms for up to 15 years, will no longer be renewed. Newmont’s agreement, which expired in December, will lapse permanently, while similar deals held by AngloGold Ashanti and Gold Fields will be phased out by 2027. Tandoh said development agreements would be scrapped entirely, citing abuse and failure by some firms to meet local obligations.

Ghana’s decision to dismantle its decades-old mining stability architecture signals a bold shift toward aggressive fiscal recalibration. With gold prices hovering near $4,900 per ounce, the government is scrapping agreements that shielded giants like Newmont and AngloGold Ashanti from tax fluctuations for up to 15 years. Accra is betting that its status as Africa’s top gold producer provides enough leverage to prioritise immediate revenue over long-term certainty.

The new regime introduces a sliding royalty scale of 9% to 12%, which is nearly double the current rates. This kicks in immediately, given current prices. It reflects a government determined to shore up fiscal buffers as it prepares to exit its IMF programme in May 2026. The termination of development agreements underscores a hardening stance against perceived corporate abuse. The Minerals Commission plans to phase out these protections by 2027.

This moves the mining landscape from a predictable, fixed-rate environment to one characterised by high-stakes volatility. While this “resource nationalism lite” aims to fund infrastructure and stabilise the cedi, it puts companies like Gold Fields on the defensive. They must now navigate a terrain where profitability is tied to the caprice of global commodity prices. Ultimately, the country is testing whether its mineral wealth remains an attractive magnet even as it significantly raises the cost of doing business.

The strategic gamble is understandable. Fiscal room remains constrained, and debt vulnerabilities persist. Stability agreements negotiated in a lower-price environment now appear misaligned with public expectations. Price-linked royalties are designed to capture windfalls when prices soar without the need for constant renegotiation.

Yet the trade-off is real. Mining investment is inherently long-term and capital-intensive. Removing fiscal stabilisers during global uncertainty shifts risk decisively toward investors. While existing infrastructure provides a buffer, the longer-term effect may be delayed expansion and reduced exploration spend. Over time, this could cap production growth just as the state seeks to maximise revenue.

There is also a sequencing risk. Success depends on administrative credibility. Investors will watch how consistently the new framework is applied. Any perception of retroactive adjustments would widen the risk premium attached to Ghanaian assets. In essence, Accra is repositioning itself from a stability-led jurisdiction to a leverage-driven one.

If gold prices remain elevated and implementation is rule-bound, the reforms could strengthen public finances. If prices correct or governance falters, the costs could surface quickly through weaker investment. This is not just a fiscal adjustment; it is a test of whether the country can extract more value from its endowment without undermining the foundations that made it a leader in the first place.