The OPEC board game

The Organisation of Petroleum Exporting Countries (OPEC) and its allies agreed to cut global oil production by 1.393 million barrels daily…

The Organisation of Petroleum Exporting Countries (OPEC) and its allies agreed to cut global oil production by 1.393 million barrels daily, reducing Nigeria’s oil production quota by 20.7 percent. Now, Nigeria will decrease its production cap to 1.380 million barrels daily from January to December 2024. Nigeria’s inability to meet previous quotas has shrunk dollar proceeds from oil sales. Many of the country’s crude lies are stranded as buyers turn to cheaper alternatives. This drop would constrain its oil production and exports, affecting government revenue and overall economic stability, as oil is a significant income source.

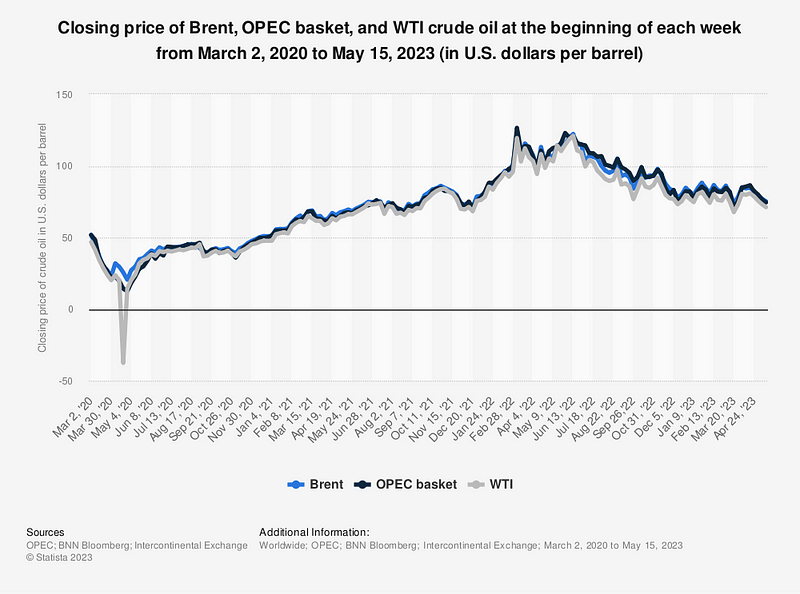

Since the Declaration of Cooperation agreement was signed at the end of 2017, Nigeria has never been assigned up to 1.9 million barrels of oil daily. Including condensates, Nigeria’s oil production for April was 1.25 million bpd, a drop of more than 17% from March. With production reaching 1.52 million bpd in March, optimists felt the country could attain the 1.69 million bpd the budget is propped on. Without condensates, Nigeria’s production in April averaged 998–999,000 bpd, signalling a return to pre-Tompolo days. April could be a one-off setback, though. The low production was caused by a two-week strike by Mobil staff, reportedly over severance pay from the American company’s push to sell its shallow and onshore oil assets to Seplat. Even though Nigeria and Angola opposed the cuts, both countries have failed to meet the previous quota obligations assigned to them. Globally, the USA appears to be winning its war with the oil cartel, as oil prices have remained relatively low. In April, when the Vienna-based organisation announced cuts this year, oil prices rose to $87, but that gain has since been shaved off. The commodity is now firmly in the $70 bracket, and the US-based Energy Information Administration predicts a ceiling of $79 for the year. The USA has deployed several tools from its arsenal to keep the price at this level. First, it has refused to stock up on its strategic petroleum reserves. Secondly, the country is pumping more than 12 million bpd, 3 million more than OPEC’s main cornerstone, Saudi Arabia. In addition to the glut US’s high production is causing, OPEC and its Russian-backed alliance say the excess printing of dollars by the American government is bringing down prices. Layered on top of that is the sanction of Russian oil output by the US and the G-7. The coalition did not seek to stop the flow of oil from Moscow but has successfully sought to cap the cost of Urals, the Russian oil grade. One aspect of the oil price narrative that the US cannot control are events in China. The world’s second-largest economy has been signalling weak growth, indicating that the oil demand could be lower than once thought. Recently, it was generally understood that the OPEC countries were happy with oil prices around $65 per barrel because at this price, the sellers made enough revenues to be comfortable, and the price was relatively affordable to major buyers. Over the last few years, it has become apparent that the OPEC countries now view $75 as a more sustainable benchmark for their needs since it keeps some dissenting members like the United Arab Emirates (UAE) within the fold and a key ally, Russia, happy. Here is simple math: Pumping fewer volumes at higher prices to make the same revenue might seem attractive because the main buyers, like China and India, have little choice but to buy at the offered price. The risk to OPEC is, at such prices, shale oil producers in the US are incentivised to drill oil and can flood the market with their products, leading to lower prices in the long run. As for Nigeria, there is little to be happy about because, unlike most OPEC countries which enjoy higher prices, we suffer because we must import refined products at higher prices, meaning more money will be spent on subsidies, or in the absence of subsidies, more suffering on the streets going forward. Since these are not issues Mr Tinubu or his economic advisers can deal with, his strategy would need some tweaking. The government should, at this point, consider decoupling investments in gas from oil. This should be followed up with increased domestic consumption because the economic cost of the recent OPEC quota cuts on Nigeria will be weighty. The cuts will reduce Nigeria’s oil exports by 200,000 barrels per day, amounting to a loss of $1.2 billion in monthly revenue. The fiscal cliff the Tinubu administration faces presents further constraints at a time when Nigeria is in dire need of elevated revenues. This shows the dilemma of a country depending primarily on the export of a single product, whose price it does not control, for its biggest government revenue source, especially for earning foreign exchange. Nigeria desperately needs to diversify its revenue from oil, and the new administration must prioritise this. The government has to increase its revenue and cut down on unnecessary public sector jobs and subsidies and diversify the economy by investing in agriculture, manufacturing, and tourism to make the country less vulnerable to oil price fluctuations. Of course, it can raise more tax revenue. But this, in an economy experiencing slow growth, does not also have great prospects. Given the sophistication and time required to develop competence in manufacturing, agriculture and tourism would have to be prioritised as low-hanging fruits that are easier to reach in the short term.