The suspense continues

The Central Bank of Nigeria rescheduled its MPC meeting to Feb 19-20 to decide on interest rates.

The Central Bank of Nigeria (CBN) has rescheduled its 299th Monetary Policy Committee (MPC) meeting to February 19 and 20 from the previously planned dates of February 17 and 18. This change addresses speculations arising from the National Bureau of Statistics delays in releasing the rebased Consumer Price Index. With the new dates confirmed, economic analysts are keen to see whether the CBN will hold or hike the Monetary Policy Rate in response to current economic trends. The initial MPC meeting for 2025, originally set for January, was postponed.

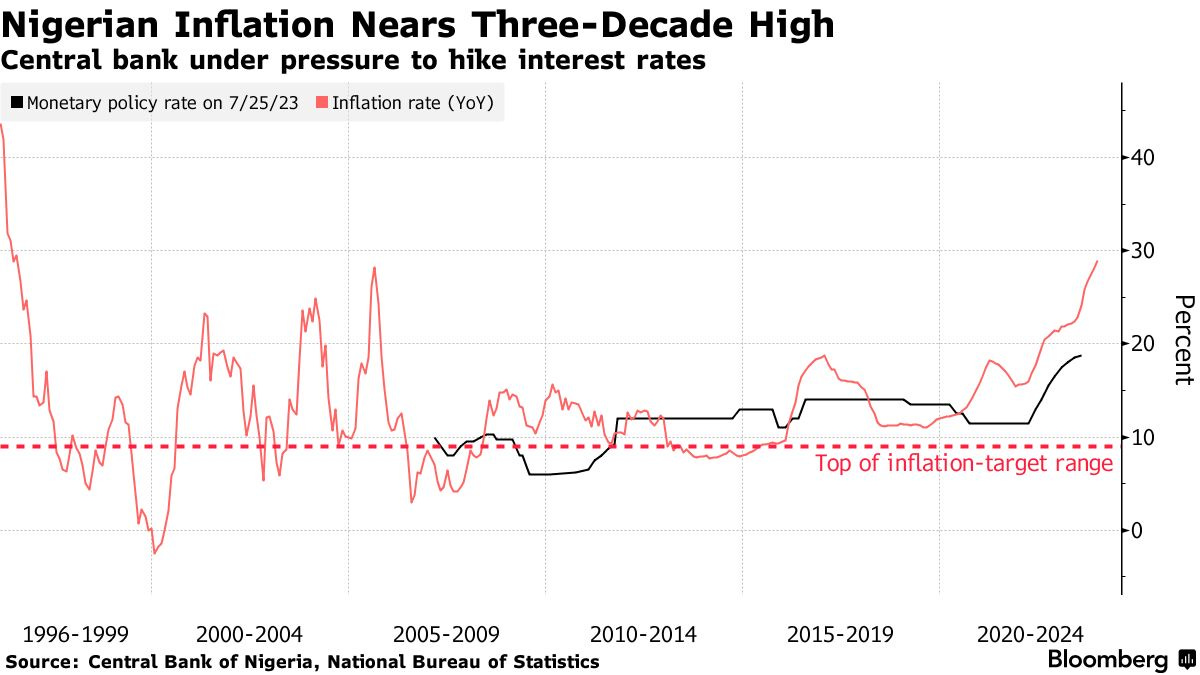

Monetary Policy Committee (MPC) meetings are pivotal for investors and businesses, as they directly influence interest rates, affecting borrowing costs, investment decisions, and overall economic activity. The initial meeting for 2025 was postponed from January to allow updated economic data to be incorporated into the decision-making process. This pattern mirrors last year’s schedule, where the first MPC meeting occurred in February. In the final MPC meeting of 2024, CBN Governor Cardoso hinted at a potential shift from the bank’s previously hawkish monetary policy stance, suggesting a more dovish approach as the country anticipates the impact of recent economic reforms in the first quarter of 2025. Nigeria’s Monetary Policy Rate (MPR) currently stands at a historic high of 27.50%, significantly increasing business borrowing costs and attracting short-term foreign portfolio investments seeking higher returns.

The federal government has announced plans to rebase the country’s GDP and inflation data to capture structural changes across various sectors better and reflect current consumption patterns. The last rebasing exercise, conducted in 2014, led to an 89% increase in Nigeria’s GDP, elevating it to $510 billion. However, due to subsequent currency devaluations and economic challenges, the GDP has since contracted and is now estimated at $363.85 billion. Analysts predict that the upcoming rebasing could push the GDP back above the $500 billion mark and potentially reduce the inflation rate below 30% from its current level of 34.8%.

While GDP rebasing is a standard statistical practice that provides a more accurate representation of an economy, it has drawn mild criticism in Nigeria’s context. Critics argue that rebasing, while technically sound, can sometimes create a misleading perception of economic progress without addressing underlying structural issues. For instance, the 2014 rebasing significantly boosted Nigeria’s GDP figures, making it the largest economy in Africa overnight. However, this did not translate into tangible improvements in living standards, job creation, or infrastructure development for most Nigerians. GDP rebasing can sometimes be a cosmetic adjustment, masking more profound economic vulnerabilities such as over-reliance on oil revenues, weak industrialisation, and persistent inequality. Without complementary reforms to drive productivity and diversification, the benefits of rebasing may remain superficial.

As the CBN prepares for the rescheduled MPC meeting, stakeholders are keenly observing whether the bank will adjust the MPR, especially in light of the anticipated economic data and ongoing reforms. The decision must strike a delicate balance between curbing inflation, supporting economic growth, and maintaining investor confidence. While the potential GDP rebasing may offer a more optimistic economic narrative, policymakers must ensure that such statistical adjustments are accompanied by concrete measures to address the structural challenges that continue to hinder Nigeria’s long-term economic stability and inclusive growth.