When growth crawls

The African Development Bank said Ghana’s economy expanded by 3.6 percent in 2022, from 5.4 percent in 2021. In its latest 2023…

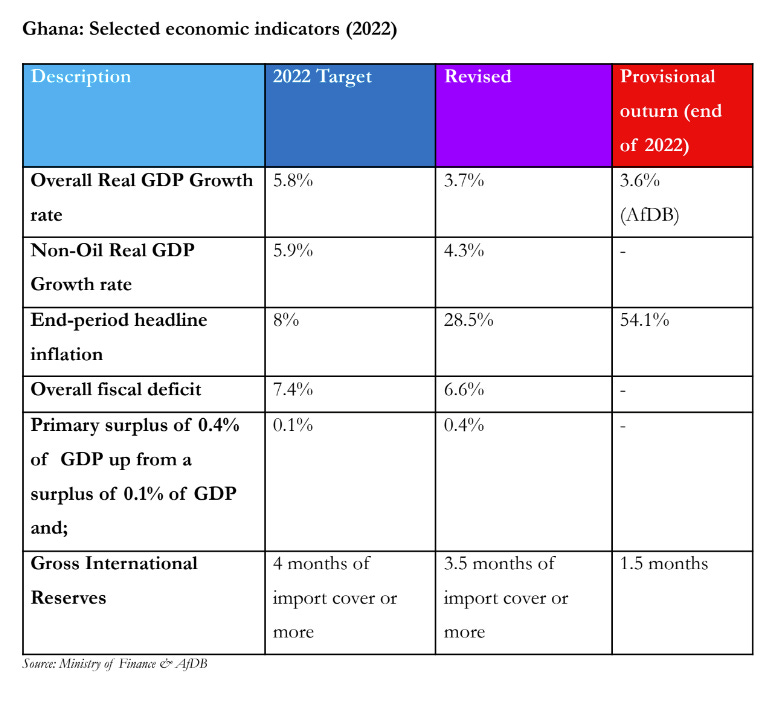

The African Development Bank said Ghana’s economy expanded by 3.6 percent in 2022, from 5.4 percent in 2021. In its latest 2023 Macroeconomic Performance and Outlook Report, it said deep macroeconomic imbalances, higher inflation, depreciating local currency, and high public debt estimated at 91 percent of GDP weighed down growth. 2022’s top African growth performers were Seychelles (8.3 percent), Rwanda (6.9 percent) and Kenya (5.5 percent). Growth in oil-exporting countries declined marginally, with average growth reaching an estimated 4.0 percent in 2022, from 4.2 percent in 2021, largely reflecting Libya’s sharp decline and Nigeria’s weaker growth.

Ghana’s macroeconomic environment came under significant pressure after the Finance Minister, Ken Ofori-Atta, presented the 2022 budget to parliament in November 2021. The adverse impact stemming mainly from global shocks and domestic developments made it difficult for the government to call the shots in its own economic space. The scarring from the COVID-19 pandemic, coupled with the impact of the Russia-Ukraine war on an already fragile global supply chain, spiking commodity prices, global inflation, interest rates and the tight financing conditions rendered the assumptions that underpinned the country’s 2022 macroeconomic planning obsolete and irrelevant. Global inflation skyrocketed to a 40-year high, and the Fed decided to tackle it by pursuing monetary policy tightening and almost all developed and developing countries, Ghana inclusive, were not spared. By the year’s first half, the Black Star’s inflation had more than doubled — from 13.9% in January to 29.8% in June. The cedi lost more than 20% of its value to the US dollar and became one of the world’s worst-performing currencies. Ghana’s fiscal deficit was 5.7% of GDP for the first half of 2022 compared to the government’s 3.9% target. Despite a 450 basis point hike in the monetary policy rate between March and May 2022, real GDP grew only 3.3% in Q1 2022. When paired with a debt-to-GDP ratio approaching 80%, global credit rating agencies duly downgraded Ghanaian debt and asset qualifications. The fall in international reserves was the last straw that broke the camel’s back. Currency reserves fell to US$7.7 billion (3.4 months of import cover at the end of June 2022, compared to US$9.7 billion (4.3 months of import cover at the end of December 2021), putting the cedi in a forlorn position. July represented a turning point for the government as it finally ate humble pie and sought an IMF bailout package after months of playing hide and seek. By the time the Finance Minister announced a revision of all macroeconomic targets for the 2022 fiscal year, including cutting GDP growth by almost half, Ghana’s economy had lost its anchor. The country has suffered at least seven downgrades and revisions and lost complete access to the Eurobond market. Foreign investors began dumping Accra’s long-term sovereign bonds, revenue targets were missed, and default was next for both external and domestic creditors. The IMF cut Ghana’s growth rate for 2022 to 3.6% from the earlier 5.2%. It, therefore, does not come as a surprise when AfDB disclosed that the country’s economy expanded by 3.6%. Sectorally, a demise in the industry was somewhat offset by expansion in agriculture and services. Most observers still maintain a positive outlook on the economy; those hopes hinge on securing a $3 billion IMF package. The government has also implemented various measures to address the imbalances and boost economic growth in 2023, including fiscal consolidation, monetary policy tightening and structural reforms. Many of those efforts are not popular. The AfDB’s projection, while higher than the IMF, World Bank or government projections, is still a long way down from recent trends. For an economy that grew by 7% on average between 2017 and 2019, the AfDB’s report serves as a reminder of the current economic turbulence and a great lesson to other Sub-Saharan African economies whose economic growths are directly tied to unstable booms in certain commodities.