Willing chocolate demand

Côte d’Ivoire doubles cocoa purchases to stabilise the sector, with supportive weather and strong investor confidence boosting prospects.

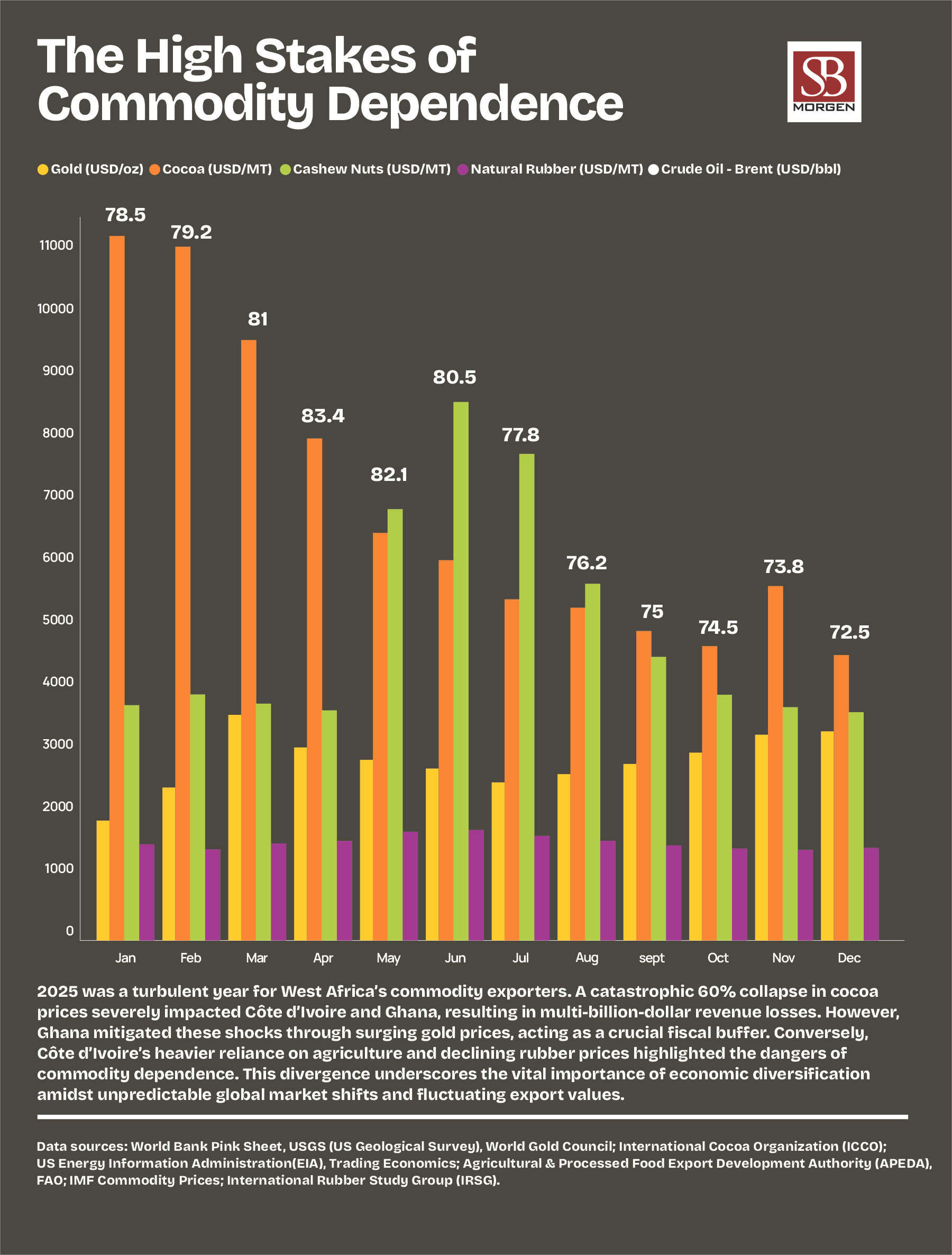

Côte d’Ivoire has doubled weekly cocoa purchases to 20,000 tonnes as authorities seek to stabilise the sector amid weak global demand, slow export buying, and quality concerns linked to storage delays. The intervention aims to absorb excess beans and reassure farmers facing liquidity pressures. Weather conditions, however, remain supportive. Farmers in key regions such as Abengourou, Divo and Soubré report adequate soil moisture despite below-average rainfall, with expectations of a stronger April–September mid-crop. Alongside sector support, the government raised 220 billion CFA francs ($396 million) through Treasury bond auctions, exceeding its 200 billion CFA target, signalling sustained investor confidence. Meanwhile, the 2026 farmgate price for raw cashew nuts was set at 400 CFA francs per kilogram, slightly lower than last year, reflecting softer global demand. Authorities say pricing remains protective and could be revised if market conditions improve.

The global cocoa market is swinging from last year’s supply shock to what now appears to be a supply surplus, and that shift is dragging down both spot and futures prices. Just months ago, the market was gripped by scarcity. Weather disruptions, disease pressure and tight bean flows from Côte d’Ivoire and Ghana pushed prices to record highs. Futures soared, grinders scrambled for supply, and producing countries enjoyed a rare moment of pricing power. That narrative has now flipped.

Improved output from Côte d’Ivoire and Ghana, which together account for about 60 percent of global cocoa production, has altered market sentiment. Bean arrivals have strengthened compared to last year’s disrupted season. Additional volumes from Nigeria, Cameroon and some Asian producers have added to global supply. What was once a tight market has loosened quickly.

Prices have responded accordingly. Cocoa futures have fallen by more than 2,000 dollars per tonne this year, sliding to around 3,800 dollars. The correction reflects not just improved supply but also buyer resistance. Trading houses and grinders are unwilling to transact at the elevated levels seen during the rally. Demand in Europe and North America has softened as manufacturers pass higher input costs to consumers, dampening grind volumes.

For Côte d’Ivoire and Ghana, this shift creates fiscal and sectoral stress. Both economies depend heavily on cocoa export revenues for foreign exchange, budget support and rural incomes. Lower prices complicate forward sales, revenue projections and the setting of farmgate prices ahead of the 2026 to 2027 season.

The stress is already visible in policy responses. Côte d’Ivoire, through its Coffee and Cocoa Council, has accelerated a government buyback programme. The CCC plans to purchase up to 20,000 tonnes per week, targeting 100,000 tonnes by March 2026, backed by 280 billion CFA francs. The state is effectively stepping in as buyer of last resort after cocoa futures fell below the fixed farmgate price of 5,000 dollars per tonne.

That pricing mismatch created a distortion. International traders were unwilling to buy at levels that did not reflect global market conditions. Purchases slowed, stocks accumulated at ports, and liquidity tightened across the supply chain. Thousands of tonnes remained unsold, raising the risk of bean deterioration and delayed payments to farmers.

By absorbing excess supply, the government aims to put a floor under domestic prices and stabilise farmer incomes. In the short term, this reduces the risk of rural income shock and broader social pressure in a country where cocoa supports millions of livelihoods.

However, the intervention treats symptoms rather than causes. The core issue is weak global demand. If grind data in Europe and North America remains soft, the government may end up holding large inventories without a clear exit strategy. Buying time is not the same as restoring equilibrium.

There is also a structural paradox at play. The current glut masks underlying supply risks. Reports of mealybug infestations and swollen shoot disease in parts of West Africa suggest potential medium-term production losses. If disease spreads and farm maintenance declines due to weaker price incentives, today’s surplus could evolve into tomorrow’s shortage.

Weather conditions add another layer of uncertainty. Farmers in regions such as Abengourou, Divo and Soubré report adequate soil moisture ahead of the mid-crop season. The mid-crop is smaller than the main harvest, but improved rainfall could enhance bean quality. That matters because the current oversupply includes concerns about deteriorating quality in unsold stocks. Even in a surplus market, shortages of premium-grade beans could emerge, creating volatility in quality differentials rather than in headline prices alone.

The strain is not limited to cocoa. In the cashew sector, where Côte d’Ivoire controls roughly 40 percent of global supply, authorities opted for a different approach by lowering the farmgate price instead of launching a buyback. That contrast underscores cocoa’s macroeconomic importance. Cocoa remains the strategic commodity, central to foreign exchange earnings and fiscal stability.

For Ghana, the policy dilemma is similar. Authorities have explored measures to manage excess beans and mobilise funding to pay licensed buying companies and farmers. The risk is twofold: physical surplus in the short term and financial stress across the value chain. If farmers face delayed payments or lower producer prices, agitation could grow, particularly after last year’s global rally raised income expectations.

The broader lesson is that cocoa has become structurally volatile. In less than a year, the market has swung from scarcity to surplus. Such rapid transitions expose weaknesses in administered pricing systems and in forward sales mechanisms that assume gradual adjustments rather than abrupt reversals.

For producing countries, the challenge is balance. They must protect farmer incomes without distorting market signals to the point where buyers disengage. They must stabilise revenues without accumulating unsustainable fiscal liabilities through repeated interventions.

The next two quarters will hinge on three variables: global demand recovery, the pace of government buybacks, and the evolution of weather and disease conditions. If grind volumes recover and weather risks re-emerge, the surplus could tighten quickly. If demand remains soft and stocks continue to build, prices may stay under pressure.

For Côte d’Ivoire and Ghana, cocoa is not just a commodity. It is a pillar of macro stability and rural welfare. Price volatility, therefore, carries consequences that extend far beyond futures exchanges in London and New York. The market may have shifted from scarcity to surplus, but the underlying fragility remains.